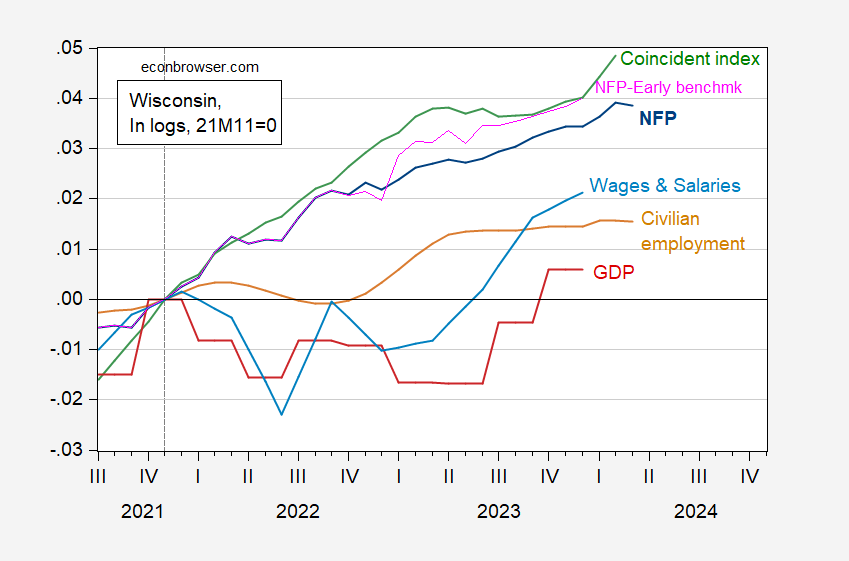

Newest employmentcoincident index:

figure 1: Wisconsin nonfarm payroll employment (dark blue), Philadelphia Fed early benchmark measure of nonfarm payrolls (pink), civilian employment (tan), linear interpolation of real wages and salaries, by state chain consumer price index ( Sky blue), GDP (red), and consistent index deflation (green), all in the log 2021M11=0.Sources: Bureau of Labor Statistics, U.S. Bureau of Economic Analysis, Federal Reserve Bank of Philadelphia [1], [2]and the author's calculations.

While Thursday's employment data showed a slight decline in nonfarm payrolls from the previous quarter, the three-month change was 12,600 (annualized growth of 1.7%).

Note that Wisconsin's synchronization index continued to accelerate in February. The trajectory of the coincidence index (and other indicators) differs from the trajectory of Wisconsin's real GDP. Note that GDP at the state level is not calculated directly through expenditure methods like at the national level.Instead, this estimate is based on factor payments combined with national-level information on industrial value added (see Bank of East Asia (2017)).

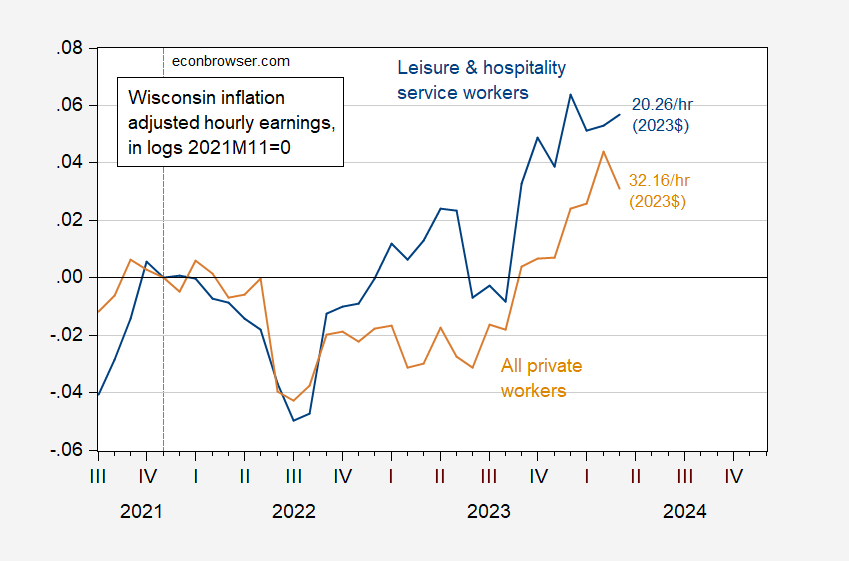

Real wages have risen since November 2021, the previous peak of US GDP.Since the average salary does not take into account wage deviations, in the absence of a median salary (see COWS/Highway Strategy To discuss median wage growth in 2022), I added real wages for workers in the leisure and hospitality industries.

figure 2: Average hourly earnings in $$ for leisure and hospitality industry workers (blue) and all private workers (tan) in Wisconsin in 2023, 2021M11 log = 0. Salaries in the Northeast-Central subregion are deflated by CPI, and the authors use the X-13 Census for seasonal adjustment. Source: BLS and author's calculations.

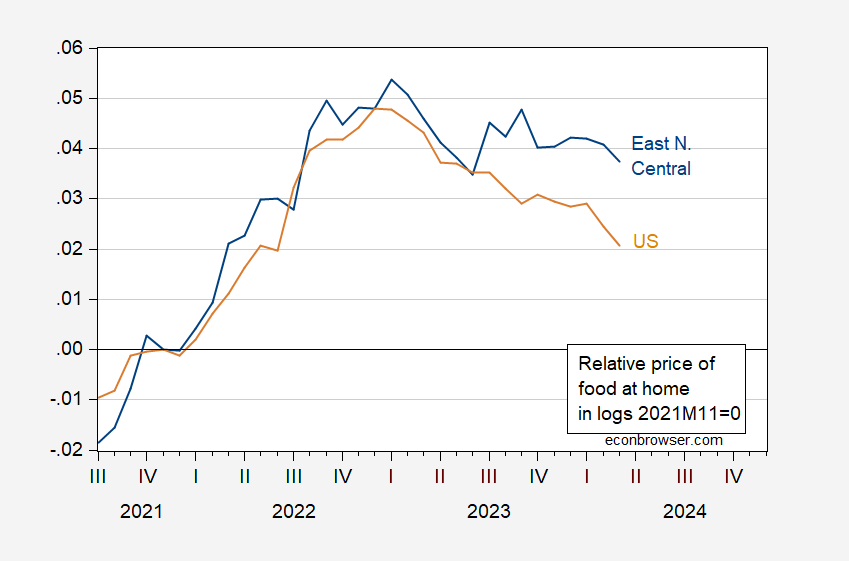

The U.S. Bureau of Labor Statistics does not report inflation by state. For states in the BLS Midwest subregion, which includes Illinois, Indiana, Michigan, Ohio, and Wisconsin, cumulative price level changes are comparable to overall price level changes in the United States.

As shown in Figure 3, household food prices have increased relatively sharply in the central and western subregions.

image 3: Relative prices of domestic food relative to overall CPI for the Northeast-Central subregion (blue) and nationally (tan) (both logarithms), November 2021 = 0. The author uses Census X-13 to seasonally adjust the Northeast-Central price index. Source: BLS and author's calculations.

as mentioned before postalHousehold food prices (i.e. groceries) have increased proportionally in the East-Central subregion than in the country as a whole.

{kind=link}

{kind=link}