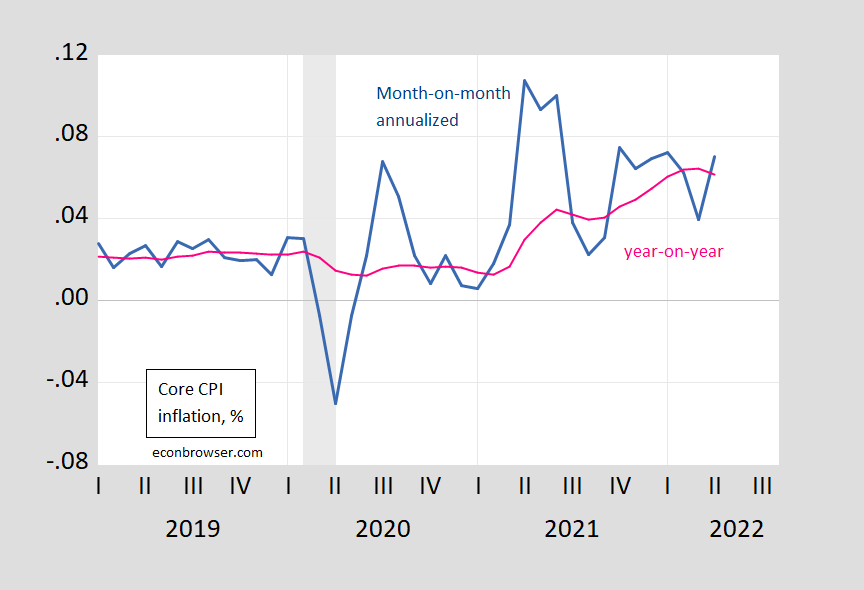

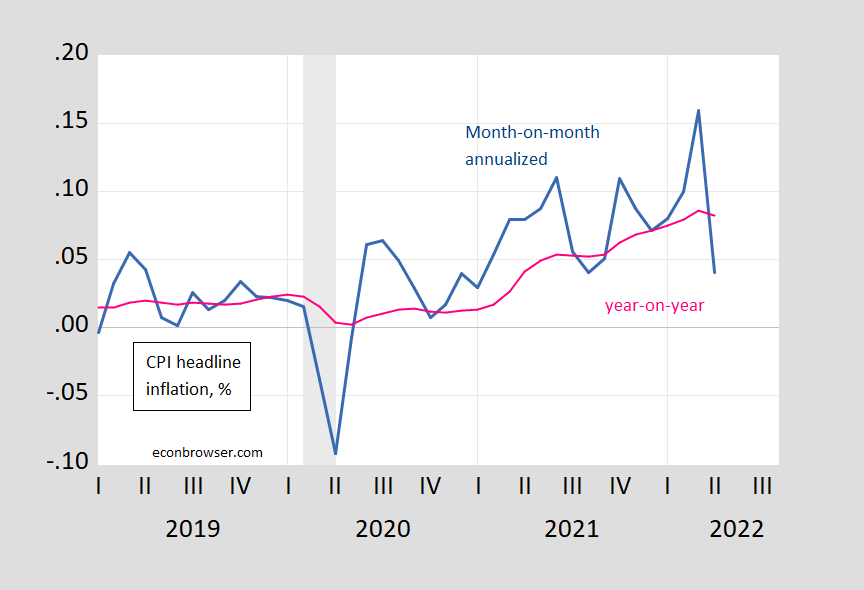

Headline CPI m/m inflation fell sharply, but both headline and core data unexpectedly rose.

figure 1: CPI month-on-month inflation, annualized (blue), 12-month or year-over-year inflation (pink), in decimal form (ie 0.05 for 5%). The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BLS, NBER, and author’s calculations.

“Base effects” will help going forward, but service inflation (and housing costs) will likely continue to put upward pressure on the overall and core.

figure 2: CPI month-on-month core inflation, annualized (blue), 12-month or year-over-year inflation (pink), in decimal form (ie 0.05 for 5%). The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BLS, NBER, and author’s calculations.

If year-on-year inflation continues to fall, we may be in a period of deflation (as mentioned earlier in the marketwhich is different from deflation, which is a general decline in prices lgrade).

Finally, we can update core inflation developments in the US and the Eurozone. In April, the monthly/monthly annualized core inflation in the US was 0.7 percentage points higher than that of the euro area, up 2.4 percentage points year-on-year. As shown in Figure 3, the fact that the m/m difference is less than year-on-year is consistent with the narrowing of the inflation gap.

image 3: Year-over-year annualized core inflation differentials for the US = Eurozone (blue), calculated using log differentials. The authors seasonally adjusted core HICP for the euro area using geometric census X-12. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BLS, Eurostat via FRED, NBER and author’s calculations.

{kind=link}

{kind=link}