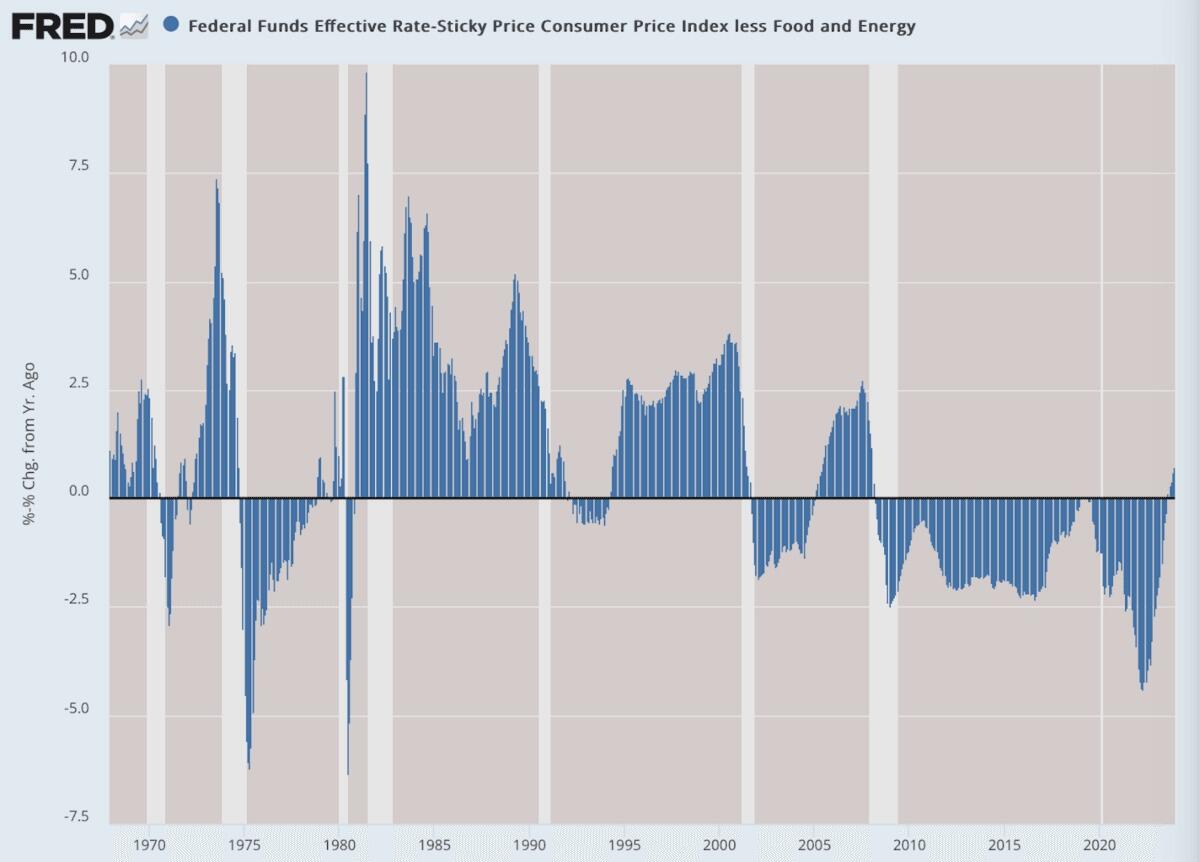

Imagine my surprise when I saw such a statement in an article titled “Interest rates are now barely positive, according to all official inflation and interest rate data” “Will the Fed elect Biden?” And attached pictures:

source: Zero hedging. Note: (Data: Federal Reserve Economic Data (FRED), Federal Reserve Bank of St. Louis; Chart: Jeffrey A. Tucker)

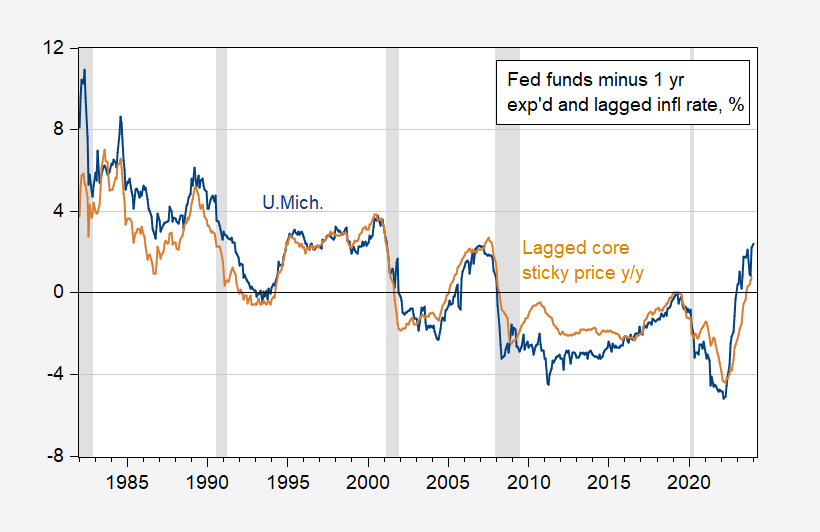

Well, the diagram looks like this because it uses Hysteresis Ex post core sticky price CPI inflation (year-on-year). If you use the University of Michigan's 1-year CPI inflation forecast to see what this graph looks like:

figure 1: The federal funds rate is adjusted one year in advance according to expected CPI inflation in Michigan, USA (blue), and adjusted year-on-year according to lagged core sticky price CPI inflation (tan), both are %. NBER-defined recession peak-to-trough dates appear gray. Source: Federal Reserve, State of Michigan, Federal Reserve Bank of Atlanta, through FRED, NBER, and author's calculations.

Over longer periods of time, the ex ante real federal funds rate is much higher than the oddly defined real rate provided by ZeroHedge. In fact, the ex ante federal funds rate was higher than its pre-recession peak in 2007 and well above real rates under Donald Trump. Regardless, theory suggests that economic decisions are based primarily on ex ante real interest rates rather than current rates adjusted for lagged inflation. Unless one uses adaptive expectations. All I can conclude is that ZeroHedge or Jeffrey A. Tucker have fully adopted adaptive expectations with unit coefficients. Quote: “Not that there's anything wrong with that.” After all, this is consistent with the Freeman acceleration hypothesis. Just a little surprising.I'm not sure why people choose core sticky price measure.

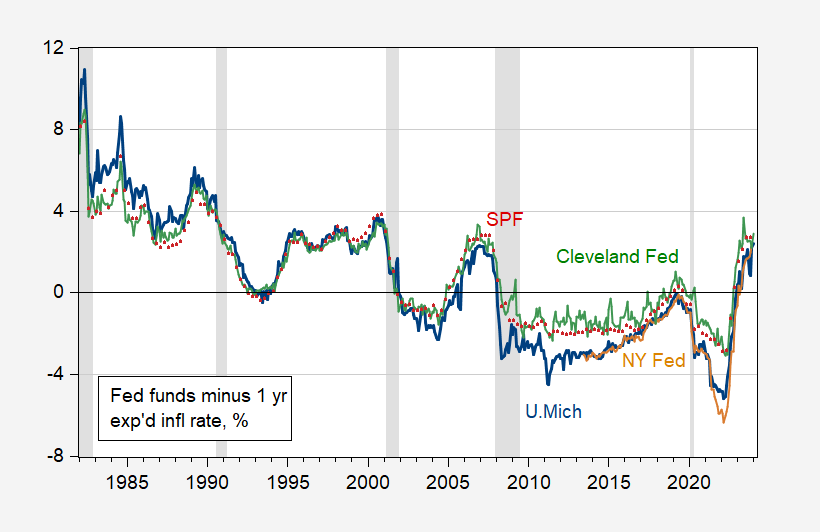

This is a more conventional picture from before Real federal funds rate:

figure 2: University of Michigan's one-year-ahead adjusted federal funds rate expectations CPI inflation annual rate (blue), New York Fed (orange), Cleveland Fed (green) and Survey of Professional Forecasters (red), all in percentages . NBER-defined recession peak-to-trough dates appear gray. Sources: Fed, University of Michigan, FRED, New York Fed, Cleveland Fed, Philadelphia Fed SPF, NBER, and author's calculations.

Therefore, other indicators of inflation expectations confirm what is actually happening from before The federal funds rate has entered positive territory.

{kind=link}

{kind=link}