perhaps. Maybe not. Some reason to wonder.

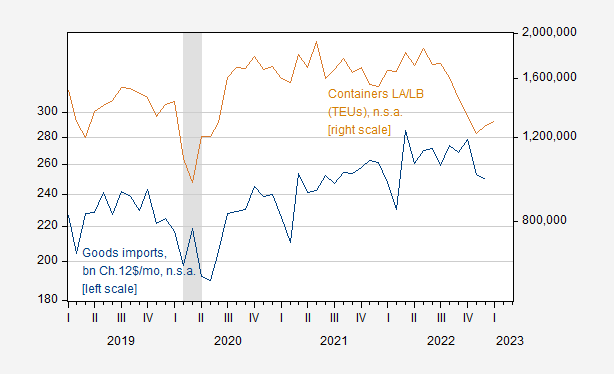

as calculated risk Note that LA port traffic drops. A drop in port throughput usually portends a drop in imports. Figure 1 shows the evolution of these two series before and during the pandemic.

figure 1: $1 billion/month of cargo imports in 2012, nsa (blue, left log scale), and containers (TEU) at the ports of Los Angeles and Long Beach, nsa (tan, right log scale). Actual imports are deflated by the import price deflator obtained from the seasonally adjusted series. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: Census, Port of Los Angeles, Port of Long Beach, NBER, and authors’ calculations.

Regression of one series on the other produced an adj-R2 of 0.32 and a slope coefficient (log-log) of 0.32. A 1 percent increase in container traffic at the ports of Los Angeles and Long Beach was associated with a 0.3 percent increase in actual cargo imports.

As far as we know, imports are indeed falling, and for the December data, if port flows are any indicator, January (nsa) imports will remain subdued relative to past peaks.

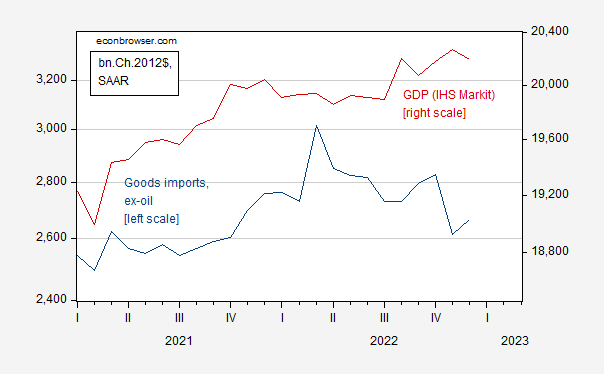

figure 2: Imports of goods except oil (blue, left log scale) and monthly GDP (red, right log scale), both in billions Ch.2012$ SAAR. Sources: BEA/Census and IHS Markit/SP Global.

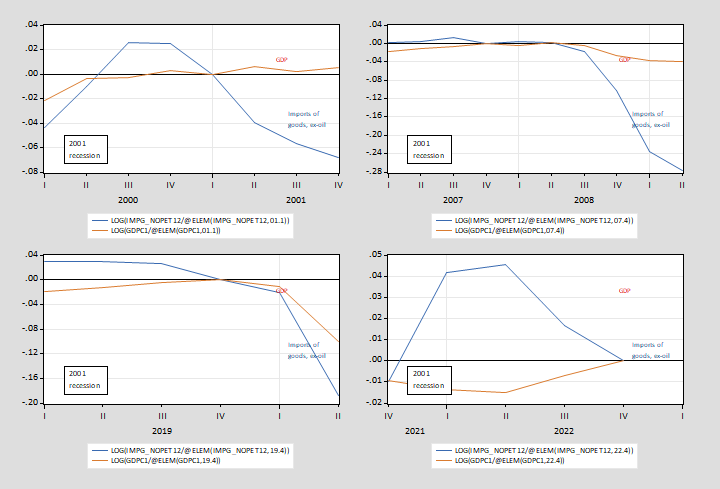

In fact, in the past 3 recessions, imports fell more than GDP (in fact, GDP didn’t fall in the 2001 recession). During the 2007-09 recession, I noticed that a collapse in imports suggested a deep recession was likely (see upper right panel in Figure 3 below).

image 3: Both GDP (tan) and imports of goods other than oil (blue) are presented in logarithmic form, normalized to 0 at the peak of the NBER (dashed red line). The normalization assumption for 2022 peaks in the fourth quarter of 2022. Sources: BEA, NBER and authors’ calculations.

Interestingly, the situation is different now than in the past. Over the past two quarters (peaking in Q4 2022), non-oil imports have been falling as GDP has risen.

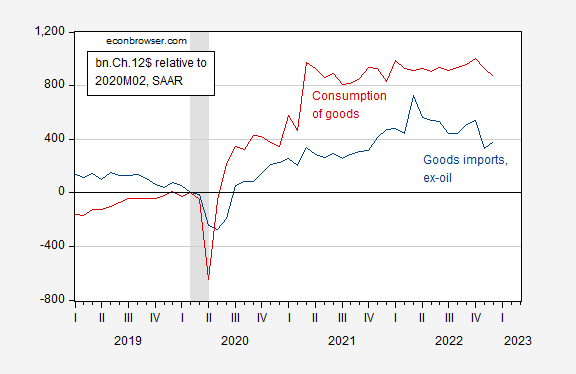

One reason imports are not seen as predicting a recession this time around is the anomalous behavior of commodity consumption during the pandemic. Figure 3 shows consumption of goods and consumption of imports relative to the 2020M02 level (peak as defined by NBER).

Figure 4: Imports of goods except oil (blue) and consumption of goods (red) differ from 2020M02 in billions of Ch.2012$ SAAR. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: BEA, NBER and authors’ calculations.

Goods imports are high because goods consumption is high. The latter deceleration is consistent with subdued (relative) levels of goods imports.

Therefore, a reduction in merchandise imports could be a signal of an economic slowdown. In fact, this is at least part of the story (as can be seen from the lower aggregate – goods and services – consumption, which peaks in 2022M10). But the other part of the story is the normalization of consumption patterns, and the reallocation of spending from goods to services.

That being said, the consensus remains for a recession, in 1Q (IHS Markit/SP Global) or 2H 2023 (for other countries), while GS raises the probability to 35%.

{kind=link}

{kind=link}