from BOFIT, February 16, 2024:

Preliminary data shows unusually strong Russian GDP growth in 2023

Rosstat released preliminary data for 2023 last week, showing that Russia's GDP will grow by 3.6% in 2023. Growth was significantly higher than expected by international or Russian forecasters. For example, the latest forecast released by the Central Bank of Russia (CBR) in November last year predicts that GDP will grow by about 2.5% in 2023. An updated forecast released by the International Monetary Fund (IMF) in late January said growth could reach 3.0 percent in 2023.

This year, Rosstat was also unusually quick to publish a breakdown of demand-side and supply-side contributions to GDP. However, information on imports and exports is still quite limited, making interpreting GDP data more challenging. While there are no clear signs of widespread and systematic statistical manipulation, uncertainty in the data and its inconsistencies increase. We can be fairly certain that the Russian economy grew last year, but any specific growth figures should be taken with a high degree of caution.

Domestic demand drives growth and supports military industry

Domestic demand growth is the driving force for GDP growth. Preliminary data showed public consumption grew by 3.6% last year, the largest increase in current GDP reporting history dating back to 1996. Household consumption rebounded strongly from the 2022 downturn. According to reports, fixed investment increased by 10.5% last year and inventory growth turned positive significantly. The foreign trade component is reported only in current prices, which makes it difficult to capture the impact of price changes. However, Russia's isolation from the global economy is evident in its declining export share, which last year accounted for just 23% of GDP, the lowest level in the current series of GDP statistics dating back to 1996.

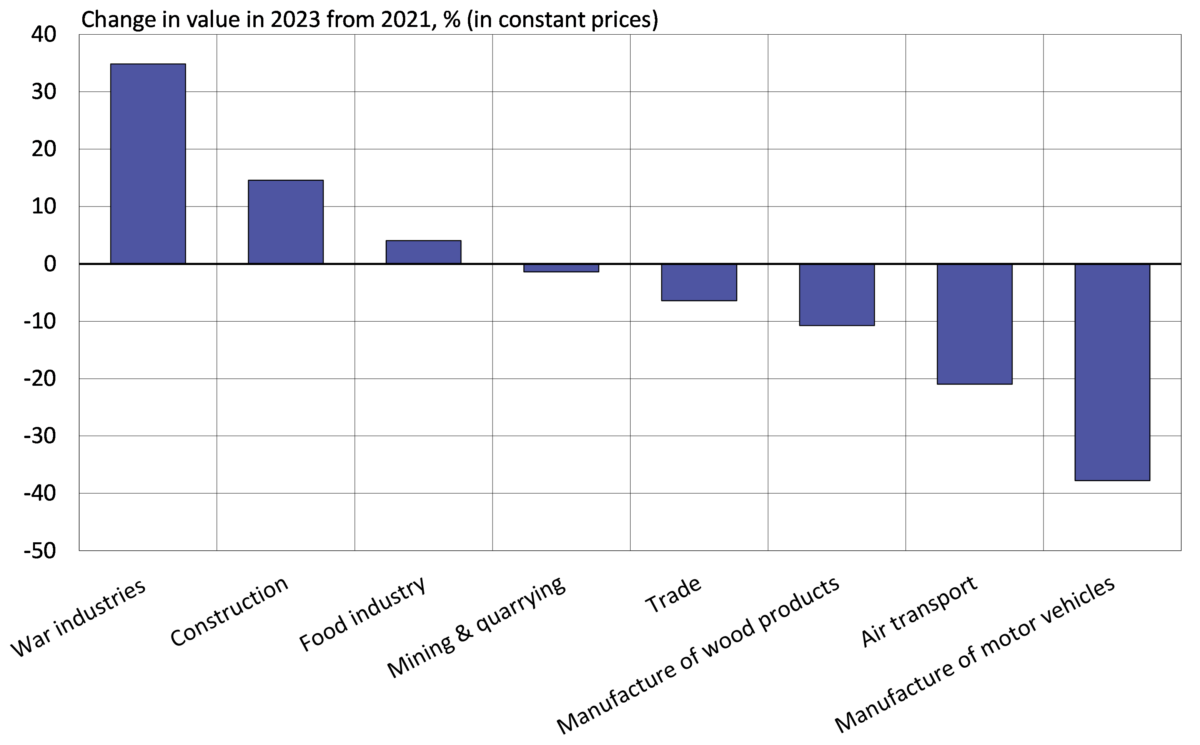

On the supply side, growing domestic demand has fueled growth in industries related to war, construction and retail. In the past two years, the industries serving the war and the construction industry have grown rapidly, and the output value in 2023 will be much higher than that in 2021. The growth of manufacturing, in particular, relied heavily on war-related industries. The output of the manufacturing sector that contributed to the war effort last year was about 35% higher than in 2021, while the total output of other manufacturing sectors fell by 0.4%. Even as the economy recovers, output last year in many industries, including car manufacturing and air transport, remained well below pre-war levels.

Russia's GDP growth is driven by war-related manufacturing and construction

Note: War industry is a proxy indicator consisting of war-related manufacturing sectors (manufacturing of metal products, electronics, and other transportation equipment).

Source: Rosstat, BOFIT.

Output growth continues to slow

Monthly data show output growth has slowed in recent months. Industrial output, retail sales and other services have remained stable for months. As of late last year, only construction seemed to be experiencing sustained growth.

…

Recent forecasts suggest Russia's gross domestic product growth will slow this year. The CBR released new forecasts today, predicting GDP growth of 1-2%. The International Monetary Fund predicts GDP growth of 2.6%, and the OECD predicts GDP growth of 1.8%. The average forecast published by Consensus Economics in January projected growth of 1.7% this year.

From US OMFIF Chari (formerly US Treasury Department) Mark Sobel, February 12, “Russia’s economic “resilience” is not what it seems”

Don’t overestimate the size of the Russian economy

Russia's war preparations and associated fiscal expansion are clear drivers of the current strong economic activity. According to the draft government plan, Russia's actual military spending will increase by nearly one-third this year, accounting for more than one-third of expenditures and about 7% of gross domestic product.

But we should not exaggerate the size and dynamism of the economy. As part of the global economy, Russia's purchasing power has fallen from nearly 4% before the 2008 financial crisis to less than 3% (currently well below 2% at market exchange rates).

Oil proceeds are an important source of income. Russian officials said Brent crude oil prices should be $85 a barrel in 2024. However, Brent crude prices have remained below that level so far this year. Furthermore, Urals oil trades at a significant discount to Brent, and there is huge opacity in the discount price Russia receives because it is highly dependent on deals with China and India.

Efforts by the United States and the G7 to tighten oil price caps and limit sanctions evasion, such as by Greek tankers, will also impact revenue. Unfortunately, they did far less damage to the Russian economy than expected.

While Russia should be able to easily finance its deficit, some costly macro factors are at play. Inflation is rising and the central bank is keeping interest rates high in light of the price outlook. This will erode real income and discourage investment. The ruble depreciates on average as currency depreciation brings more rubles to the budget. Without capital controls, the currency is likely to depreciate further. Russia may also tap its national wealth fund.

More generally, the Russian economy can increasingly be described as a system of financing energy production, financing ever-increasing military spending, and little else in a society that already lags far behind other countries on the technological front Innovation. But, of course, we should take the reliability of economic data, especially Russian economic data in the current circumstances, with a pinch of salt.

geopolitical vulnerability

Russian Growing reliance on ChinaIndia, Iran and other countries are weak points outside the development of energy markets. India is strengthening ties with the United States. China is willing to maintain There are strong export links with the United States and Europe.Despite cheap energy, China and its companies will Wary about Russia dealfearing they might violate U.S. sanctions, particularly those that could block access to the U.S. financial system.

At the same time, Russia is experiencing a rapid loss of human capital. The death of soldiers (estimated at more than 300,000 soldiers killed or seriously injured) and the huge brain drain (estimated at up to 1 million, mostly young and well-educated) are causing huge losses in human capital, according to reports in the labor market nervous. These factors will harm Russian productivity in the future.

Western sanctions on technology, even if greatly circumvented by transshipments and other leaks, can hurt economies. Reports abound of a lack of spare parts – Russian aircraft, for example, struggle to remain fully operational. Russia would also face difficulties in developing many energy sectors without Western services.

The opportunity costs of war preparations are also reflected in numerous reports of burst pipes and loss of winter heating across Russia as basic infrastructure needs cannot be met.

this is mine August blog post Trying to determine how non-military spending will grow in 2023.

{kind=link}

{kind=link}