Yesterday (November 29, 2023), the Australian Bureau of Statistics (ABS) released the latest data— Monthly consumer price index indicator – In October 2023, the inflation rate fell sharply. The release resolves some uncertainty surrounding September quarter data released last month, which showed a slight rise. I analyze this data release in this article – Australia’s inflation rate rises slightly due to unreasonable further interest rate hikes (October 25, 2023) and concluded that the small increase was not a sign of excess spending and would soon be resolved. Today’s data is the closest to what is actually happening now, showing annual inflation falling from 5.6% in September 2023 to 4.9% in October. The trajectory is firmly downward. As shown below, the only component of the rise in CPI was either due to short-lived external factors beyond the RBA’s control or was caused by the RBA rate hike itself. The governor of Australia’s central bank tried to justify raising interest rates in Hong Kong this week by saying Australian households were coping well. Her analysis is one-sided and ignores the huge distributional differences caused by rising interest rates. Justify the unreasonable!

Australian inflation continues to fall sharply

The data comes as the new RBA governor is making the rounds in Hong Kong, telling an audience at a so-called “high-level meeting” that Australia’s inflation is too high, despite raising interest rates 11 times since May 2022 , but Australian families are still “in a good position”.

I wonder if she actually asked some families if they were doing well.

She also claimed the impact of RBA interest rate decisions was uneven and:

There are distributional consequences, and we are dealing with the political economy challenge of distributional issues associated with rising interest rates.

Who is handling it?

Not the Reserve Bank of Australia?

Their stated goal is to make these “challenges” worse by driving up unemployment, thus throwing some 140,000 workers out of work.

If the RBA has its way, these job losses will mainly affect low-income households, which are also those hardest hit by rising interest rates.

I wrote about this in this article – The RBA wants to destroy the livelihoods of 140,000 Australian workers – a shocking indictment of a failed state (June 22, 2023).

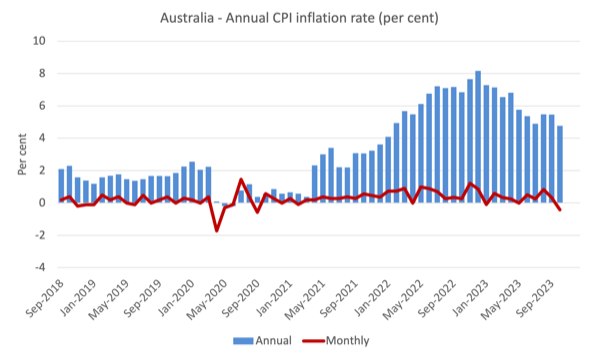

ABS Media Release (November 29, 2023) – As of October 2023, the monthly CPI indicator increased by 4.9% compared with the same period last year. – Point out:

The 4.9% increase was down from 5.6% in September and down from a peak of 8.4% in December 2022…

The largest contributors to annual growth in October were housing (+6.1%), food and non-alcoholic beverages (+5.3%) and transport (+5.9%)…

The annual increase in rents was down from September’s 7.6% increase, primarily due to increases in federal rental assistance effective September 20, 2023 and lower rents for eligible tenants…

Electricity prices rose 10.1% in the 12 months to October, reflecting increases in wholesale prices following the annual price review in July 2023…

Motor fuel prices rose 8.6% in October from 12 months ago as global oil prices rose. That was down from September’s annual growth rate of 19.7%.

So some observations:

1. All major contributors are in decline.

2. Rising rents are partly due to the Reserve Bank of Australia’s own interest rate hikes, as landlords in a tight housing market simply pass on higher borrowing costs – so so-called anti-inflation rate hikes are actually driving inflation .

3. None of the other major drivers are sensitive to rising interest rates and decline for reasons unrelated to short-term policy changes.

4. The rise in electricity prices is due to poor supervision of private power companies, which is a failure of the government. I wrote about this in a recent blog post – Failure in government regulation leads to profit-boosting by power grid companies (November 22, 2023).

5. Note that fiscal policy expansion—federal rental assistance programs have helped reduce inflation and provide some relief to households—but not enough.

The federal government could have done more to ease the pressure on families caused by temporary increases in the cost of living over the past two years.

The latest ABS data (linked in the introduction) shows:

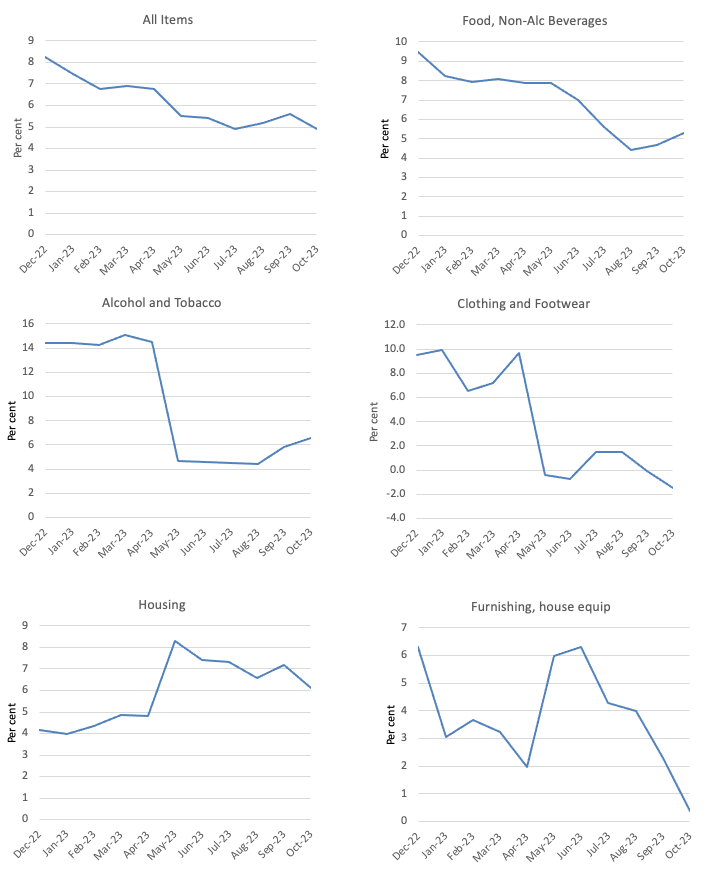

- The CPI measure for all groups fell by 0.41% and 4.8% respectively over the past 12 months (down from 5.5%).

- On an annual basis, food and non-alcoholic beverages fell by 0.2 percentage points.

- Clothing and footwear fell 1.5 percentage points.

- Houses rose 0.8 points.

- Furniture and home equipment fell 1.5 percent.

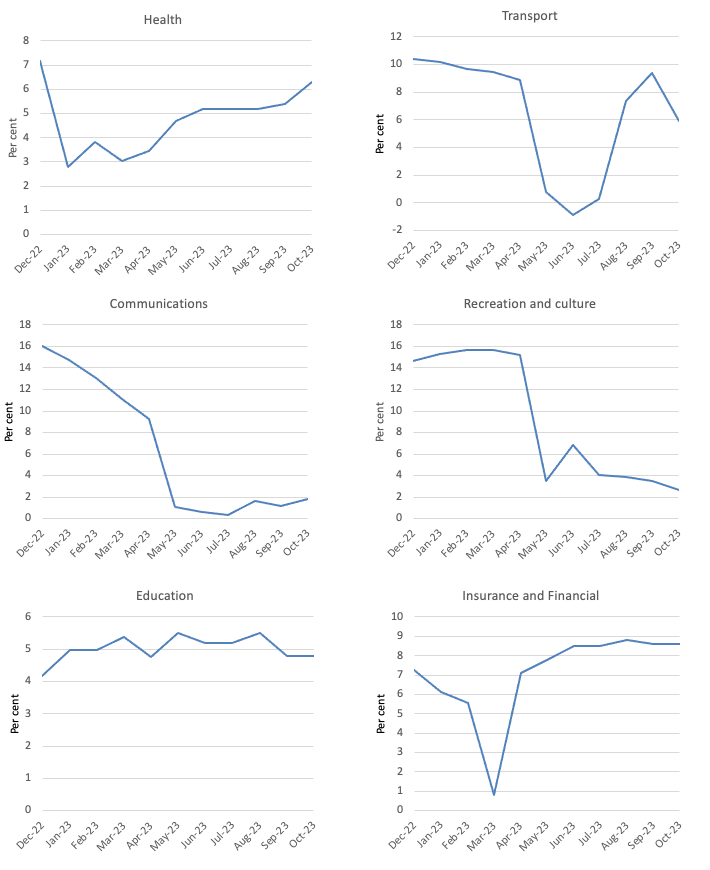

- Health dropped by 1.7 points.

- The transportation industry fell by 0.9 percentage points.

- Communications fell 0.2 points.

- Leisure culture dropped by 7.9 points.

- Education fell by 1.9 percentage points.

- Insurance and financial services rose 0.9 points.

As a result, most major commodity categories fell sharply.

Note that the growth of FIRE services is partly due to banks’ profit-seeking efforts.

The overall conclusion is that the global factors driving inflationary pressures are weakening rapidly as the world adjusts to the coronavirus pandemic, Ukraine and OPEC profiteering.

The next chart shows that the annual inflation rate is heading in one direction – falling rapidly.

The blue column shows the annual rate, and the red line shows the month-to-month change in CPI for all items.

The chart below shows the changes in the main components of CPI for all projects between December 2022 and October 2023.

Overall, as noted above, price growth has fallen sharply across most components and the exceptions do not provide any justification for further rate hikes by the RBA.

Overall, inflation is falling as supply factors ease.

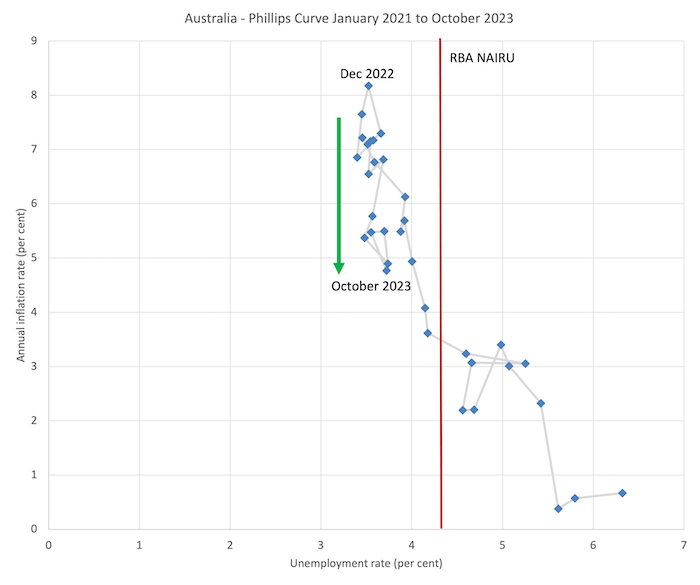

RBA’s fictional NAIRU

In June 2023, the governor of the Reserve Bank of Australia (then deputy governor) claimed that the so-called non-accelerating inflation unemployment rate (NAIRU) was 4.5% and that unless the unemployment rate rose to that level, inflation would continue to accelerate.

This is just a direct application of mainstream textbook garbage, which says: If the unemployment rate is below the NAIRU, inflation will accelerate; if the unemployment rate is above the NAIRU, inflation will fall.

Logically, NAIRU defines a state in which inflation is stable.

I reject this logic, but let’s use it to test its internal consistency.

On this basis, even if we accept that there is a definable NAIRU that can be measured in some way, the RBA governor’s narrative is clearly wrong.

I discuss this in more detail in this post (and others) – Mainstream logic should conclude that Australia’s unemployment rate is higher than the NAIRU, not lower than the NAIRU as the Reserve Bank of Australia claims. (July 24, 2023).

The Reserve Bank of Australia has now revised its NAIRU forecast to 4.25%.

The key is that, according to NAIRU logic, if the unemployment rate is below NAIRU, then inflation should accelerate; if the unemployment rate is above NAIRU, inflation should decelerate.

The facts are shown in the chart below, which is a graph of the Philip Curve from January 2021 (before inflation accelerated) to October 2023.

The Phillips Curve depicts the relationship between the unemployment rate (horizontal axis) and an inflation measure on the vertical axis.

Judging from the situation in Australia over the past two years, the situation is very obvious.

Unemployment was very stable last year, but inflation has been falling since September (green arrow).

This means that logically, NAIRU cannot be higher than the current unemployment rate, but must be lower than the current unemployment rate.

This means the RBA’s insistence on adding 140,000 extra workers to the unemployment scrap heap is unfounded even within the theoretical framework they believe in.

The vertical red line is the RBA’s NAIRU, which overlaps with an inflation rate of just over 3%.

But at this rate of inflation, with a wide range of unemployment rates – from 4.1% to 5.3% (approximately), if I were to run an econometric model to formally estimate NAIRU, I would get a wide confidence interval, at This is a range within which I cannot statistically discriminate—in other words, NAIRU’s estimates are useless for policy.

NAIRU estimates are simply a tool used by ideologues who want to increase unemployment and give businesses more bargaining power.

The latest inflation peak occurred in December 2022, and has been declining steadily since then, with minor fluctuations in April 2023.

But look at how far the unemployment rate has fallen?

Very narrow.

Therefore, if inflation is systematically declining at the current unemployment rate (3.7%), then the NAIRU is unlikely to reach 4.25%.

Logically, it has to be below 3.7%.

in conclusion

The problem with the RBA’s narrative is that it only touches on a subset of the spending categories faced by households.

The RBA cited data to justify its assertion that households have sufficient financial buffers (from savings) to cope with additional mortgage payments, but do not include costs related to education and health insurance, which have a significant impact on large A staple item for most homes.

And estimates are based on averages, but there is no “average”!

It is clear that low-income households are facing significant financial pressure – the proportion of households earning less than current costs is estimated to be around 15%.

On the other side are wealth holders, mainly seniors who own their homes, have interest-rate sensitive income or bank shares.

The group is currently meeting.

These allocation changes are important, but have been ignored in the RBA’s rhetoric to justify its irrational decisions.

In addition, yesterday’s data confirmed the Reserve Bank of Australia’s statement that domestic wage growth is threatening price stability.

Although the latest data from the Reserve Bank of Australia shows some promising growth in nominal wages, inflation is falling rapidly.

I cover this data release in this post – Australia – Nominal wage growth strong but still below inflation – no reason to deliberately increase unemployment (November 23, 2023).

That’s enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}

{kind=link}