The incoming Reserve Bank of Australia governor was confronted by “activists” yesterday (29 August 2023) as he prepared to address an audience at the Australian National University in Canberra. It’s a good thing for her that they filed an unemployment benefit application with her and put her name on it already. That was in response to her dire speech in June, in which she said the RBA intends to push the unemployment rate from 3.5% to 4.5%, meaning about 140,000 workers would be forced out of work. The problem is that even if we believe the logic underpinning this desire, the actual empirical evidence does not support this conclusion. Today, 30 August 2023, we have received more evidence, with the latest figures released by the Australian Bureau of Statistics (ABS): Monthly Consumer Price Index Indicator – In July 2023, inflation falls sharply. In addition to considering these figures, today I review the latest JOLTS figures released yesterday by the US Bureau of Labor Statistics. These two considerations go hand in hand, suggesting that central bankers in Australia and the US have lost their minds. After all, we commemorate a great musician who died recently to soothe our souls.

Australian inflation continues to fall sharply

The incoming governor has gained notoriety and may have locked in her appointment through the government when she delivers a speech in Newcastle on June 20, 2023, which lays out the scenario for the central bank to raise interest rates until unemployment rises to 4.5% from current levels. plan. 3.5%.

Based on the size of the workforce at the time, this would require approximately 140,000 currently paid workers to be forced into the unemployment queue.

It’s shameless proof that these central bankers have come a long way from reality – clouded by flawed “textbook” fiction.

I wrote about this in this blog post – The RBA wants to destroy the livelihoods of 140,000 Australian workers – a shocking indictment of a failed state (June 22, 2023).

Even if we start with a “textbook” fiction, the intentional plan to destroy thousands of jobs to set the economy at a so-called “Non-Accelerating Inflationary Unemployment Rate” (NAIRU) doesn’t hold water. stack up.

Even if we admit that there is a definable NAIRU, and that it can be measured in some way, there is no point in revenue governor’s plan.

I wrote about this problem in this blog post (and others) – Mainstream logic should conclude that Australia’s unemployment rate is above NAIRU, not below NAIRU as the RBA claims (July 24, 2023).

The point is, according to NAIRU logic, if the unemployment rate is below NAIRU, then inflation should accelerate; if the unemployment rate is above NAIRU, then inflation should decelerate.

Logically, NAIRU defines a state where inflation is stable.

Unemployment has been remarkably stable over the last year (although it only started to rise last month), but inflation has been falling since last September.

Ladies and gentlemen, this means that, logically, NAIRU cannot be higher than the current unemployment rate, it must be lower than the current unemployment rate.

This means that the RBA’s insistence on including 140,000 extra workers on the unemployment dump is unfounded even in the theoretical structure they believe in.

This is simply a mindless bastard.

It was great last night to see her being called upon by young activists at the ANU.

Armed with megaphones and signs, activists demanded that the incoming governor be the first to join the unemployment queue.

Protesters held up a large unemployment claim form with the name of the incoming governor on it.

They shouted through the loudspeakers:

We’ve started, we’ve started filling out your job application forms…if 140,000 people need to lose their jobs at your hands, we think you should go first.

The university’s elite apparently yelled “you should be ashamed of yourselves” at the protesters.

Here’s what elites without job risk would say.

You can watch a short video of the protests via the ABC News website — Protesters interrupt incoming RBA chief’s speech.

I’ve often wondered what policy would come out if policymakers had to face the consequences first—wage cuts, job losses, and so on.

But today we saw firsthand why the protesters’ point of view made sense.

ABS released the latest news—— Monthly Consumer Price Index Indicator – July 2023 shows:

1. The CPI rose by 4.9% in the past 12 months, lower than 5.4%, and the inflation rate continued to decline.

2. Although inflation for owner-occupier purchases of new dwellings has fallen sharply, housing remains a major contributor – 8.3% in May 2023 (over 12 months), 6.6% in June, now 5.9 in 2023 %. July.

3. But the rent component of housing rose from 6.3% in May, 7.3% in June and 7.6% in July. Part of the rent can be traced to rate hikes by the RBA itself, which has pushed up the cost of investment loans, which landlords have passed on to tenants.

Raising interest rates causes inflation, not the other way around.

4. As the government allows highly concentrated industry bosses to make profits, electricity prices are also increasing day by day.

As it stands, however, it still provides good information for assessing the direction of inflationary pressures.

ABS Media Release (30 August 2023) – As of July 2023, the monthly CPI indicator will rise by 4.9% year-on-year – point out:

The annual growth rate for the month was 4.9%, down from 5.4% in June. Annual price growth continues to moderate from its peak of 8.4% in December 2022.

The next graph shows that the annual inflation rate is heading in one direction – falling rapidly.

The blue bars show the annual rate, and the red line shows the month-to-month changes in CPI for all items.

The chart below shows the movement of the major components of the CPI for all projects between December 2022 and July 2023.

Overall, price increases for most components have fallen sharply.

But overall, inflation is falling as supply factors ease.

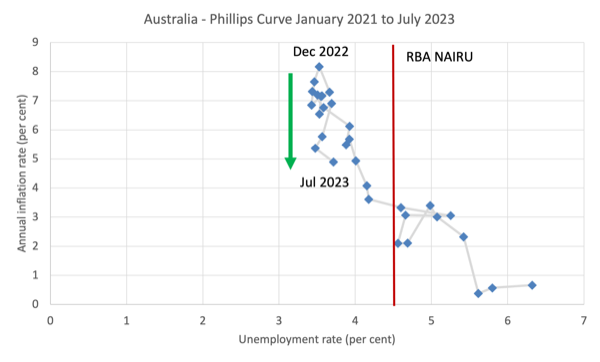

To help you understand what’s going on, the next graph is the Phillips curve from January 2021 (before inflation accelerated) to July 2023.

The horizontal axis is the official unemployment rate, and the vertical axis is the annual CPI inflation rate.

The solid vertical line (4.5% unemployment) is the current RBA NAIRU estimate.

It coincides with an inflation rate of just over 3%, but at that rate the unemployment rate shows a wide range – from 4.1% to 5.3% (approximately), if I were to use an econometric model To estimate the unemployment rate NAIRU formally, I get a wide confidence interval within which I cannot discriminate statistically—in other words, the NAIRU estimate is useless for policy.

They are just tools for ideologues who want higher unemployment and more bargaining power for businesses.

The most recent peak in inflation was in December 2022, and it has been declining steadily since then, with a small fluctuation in April 2023.

The green arrow depicts this decline.

But look at the extent of the decline in the unemployment rate?

very narrow.

Therefore, if inflation is systematically falling at the current rate of unemployment (3.7%), then it is impossible for NAIRU to reach 4.5%.

Logically, it must be lower than 3.7%.

Who said the American labor market is booming?

I noticed the Jackson Hole Fed President’s speech the other day, he seemed to enjoy flexing his muscles and threatening further rate hikes.

Some argue that the U.S. labor market is booming and could see a burst of accelerated wage growth.

Officials keep claiming that low unemployment portends overemployment — all from the twisted NAIRU logic that central bankers are obsessed with.

I haven’t fully researched the latest — Job Openings and Labor Turnover Survey (JOLTS) – Data released by the US yesterday.

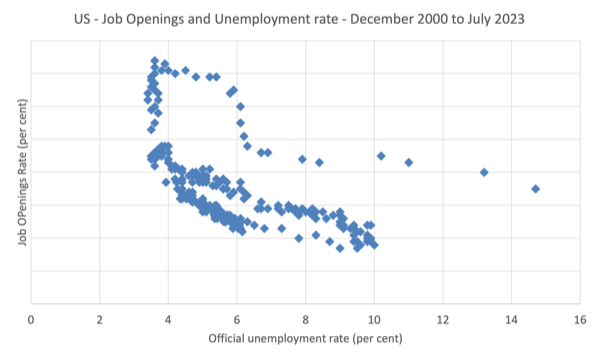

But two things caught my attention and I summarized them with a graph.

First, job vacancies in the non-farm sector have fallen dramatically.

Covid-19 has dealt a massive shock to the U.S. labor market, replacing an otherwise relatively stable relationship between job vacancies and unemployment.

With labor demand improving again and the unemployment rate falling rapidly, we reach our peak job vacancies in March 2022.

The demand side fell off a cliff.

Another shocking thing about this chart is that the official unemployment rate was little changed in the face of a collapse in the demand side of the US labor market.

That sheer vertical drop is pretty remarkable.

But it suggests that relying on the dynamics of the unemployment rate as a general estimate of the strength of the labor market is worrisome.

Another interesting thing I saw in yesterday’s JOLTS data was the change in quit rates.

I have pointed out before that the resignation rate is a good indicator of how strong the labor market is.

Employees tend to quit more frequently when job opportunities are plentiful, and keep their jobs when things look bleaker.

Quit rates peaked at 3% in November 2021 and have been declining since then.

With such worker behavior continuing to be apparent, it’s hard to argue that the US labor market is overheating.

Music – Sisto Rodriguez

Here’s what I heard at work this morning.

In 1970, I got this album — cold facts – from an import store in Melbourne.

I used to go to that store often.

Here is the first studio album by a little-known American performer – Sisto Rodriguez.

The first track is- sugar man – I fell in love with it immediately.

South Africa’s apartheid government banned it – drug references – and I think that’s a good sign.

It was difficult to find any information on the singer-guitarist, and his concentration was beginning to blur.

And then the movie— looking for sugar man – Released in 2012, it brought a new audience to this performer, and I’m excited to learn more about him – even though it’s been about 42 years since his first album.

He died on August 8, 2023 at the age of 81.

A mystery and a great talent.

Despite his poverty, he still defended the rights of the underprivileged and held regular public office to advance those causes.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}