Back to the beginning of the year, sir. steven kopitz Assert that the Philadelphia Fed’s early preliminary benchmarks support a recession in the first half of 2022, namely:

Menzie, you are right that the Eastern Survey is more likely. You wrote: So: (1) I give more weight to the institutional series, (2) the gap between the two series is more likely to be due to increased measurement error and bias in the family series, rather than, for example, mainly being counted The number of employed people increased. https://econbrowser.com/archives/2022/12/the-household-builtment-job-creation-conundrum

It turned out to be dead wrong. Predictably.

You’re wrong because you haven’t considered statistics more holistically. This is where your students learn. If your dial is telling you different things, cross check your indicators. If employment is growing rapidly, then GDP should also be growing. If jobs are rising rapidly, so should mobility and gasoline consumption, because so many people in this country drive to work. Finally, if productivity plummets when jobs are added, you really need to stop and put together some narrative to explain why this happened. It indicates an anomaly in the data that needs to be examined carefully.

If you did, Menzie, you might end up like the Philly Fed…

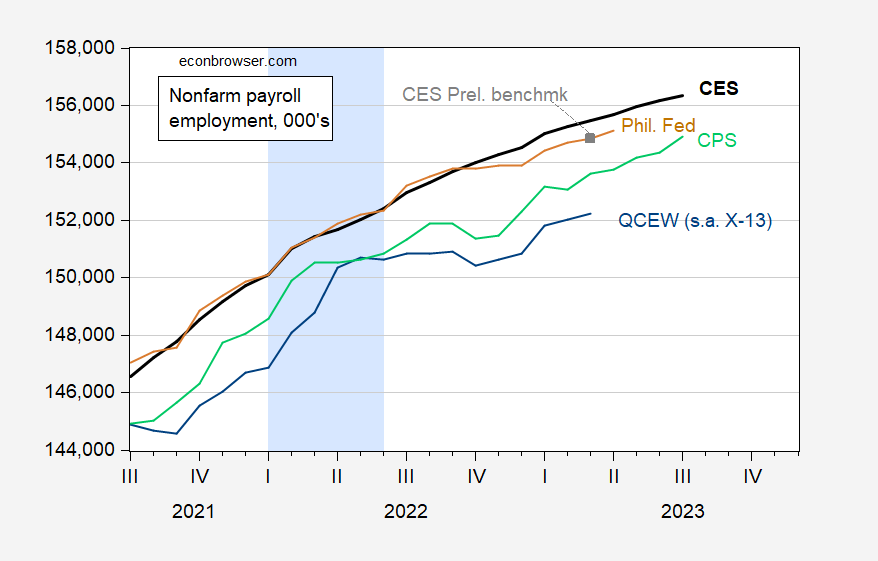

Based on the newly released QCEW data (used by the Philadelphia Fed to generate early benchmarks), what do we now think happened to the labor market in the first half of 2022?

figure 1: Nonfarm Payrolls, FRED Series PAYEMS (bold black), Preliminary Baseline (gray squares), Philly Fed Aggregate Early Baseline by State (tan), Employment of Civilian Over 16 Adjusted for NFP Concept (light green), Quarterly Employment Census and total wages covering employment, adjusted from the author’s X-13 census log (blue), all in thousands, seasonally adjusted. Light blue shading indicates (by Mr. Steven Kopits) a hypothetical recession in the first half of 2022. Sources: PAYEMS by BLS via FRED, Civilian Employment Adapted to NFP Concepts by BLS, QCEW by BLS, Bureau of Labor Statisticsthe sum of the early benchmark data philadelphia fed.

Note that the preliminary benchmark revision did not materially change the trajectory of non-farm payrolls.

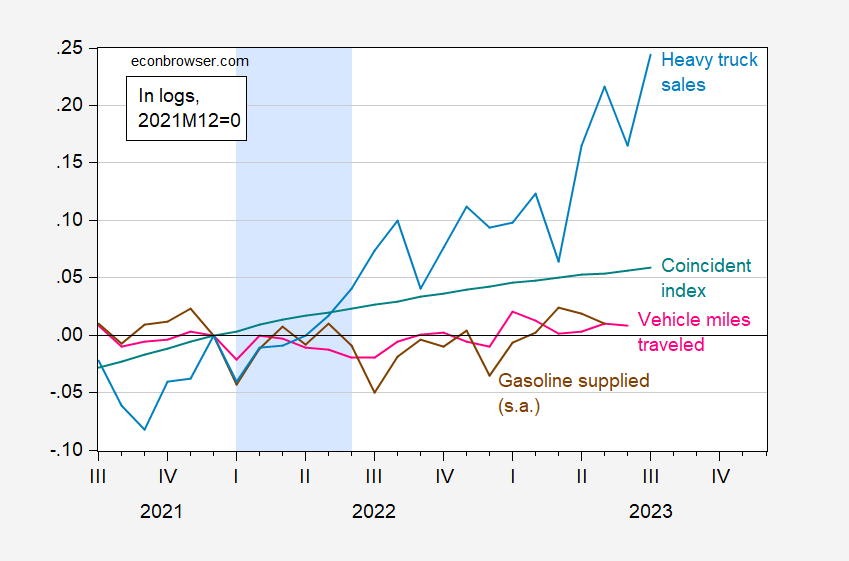

What about the other important predictors pointed to by Mr Kopitts? Figure 2 shows the vehicle mileage as well as the gasoline product supplied (consumption is highly correlated with a regression coefficient of 1, so it is also a proxy for it).

figure 2: Vehicle miles driven (pink), motor gasoline supplies (brown), heavy truck sales (light blue), US Concordance Index (teal), all in log form, seasonally adjusted. Gasoline availability is seasonally adjusted using a multiplicative moving average. Light blue shading indicates (by Mr. Steven Kopits) a hypothetical recession in the first half of 2022. Sources: VMT, Heavy Truck Sales from FRED, Motor Gasoline (NSA) from EIA, Concorde from Philadelphia Fed, from FRED.

Note that each index in Figure 1 is rising from December 2021 to June 2022. I think VMT is providing a false signal (assuming NBER doesn’t declare a recession in 1H22). Gasoline supplies also appeared to point to lackluster growth last year. On the other hand, conventional indicators such as the Philadelphia Fed Coincidence Index continued to rise. Heavy-duty truck sales in mid-2022 are up nearly 5% from end-2021 levels.

high and rising value of Heavy Truck Sales Index For me, there is no recession as of June 2023. But there is no guarantee for the second half of 2023.

{kind=link}

{kind=link}