The Australian Bureau of Statistics released the latest – Australian National Accounts: National Income, Expenditure and Product, March 2023 – Today (1 March 2023), this suggests that the Australian economy has grown by just 0.2% in the third quarter of 2023 and 2.3% over the past 12 months. If we extend the March results to the full year, then GDP would have grown by 0.8%, well below the rate of growth needed to keep the unemployment rate down. Hours worked fell in the March quarter, a trend I expect to accelerate in the coming quarters given the actions of central banks and treasuries. Results for the March quarter pointed to a marked slowdown in growth, with households cutting consumer spending further while saving less relative to disposable income in an effort to keep consumption growing amid rising interest rates and temporary inflationary pressures. I expect growth to fall further and we’re going to have higher unemployment and lower household wealth due to the RBA’s misjudgment.

The main features of the national accounts for the third quarter of 2023 are (seasonally adjusted):

- Real GDP rose 0.2% in the quarter (down from 0.5% in the previous quarter). The annual growth rate was 2.3%, but the annualized growth rate in the March quarter was only 0.8% – headed for recession.

- Australia’s terms of trade (seasonally adjusted) rose by 2.8% and 0.1%, respectively, over the 12 months.

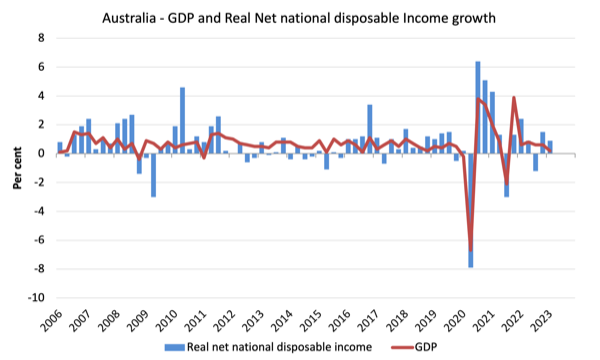

- Real net national disposable income, a broader measure of change in the national economy’s well-being, rose 0.9 per cent in the quarter and 2.1 per cent over the past 12 months, meaning Australians are living (on average) higher than they would in 12 months ago at that time.

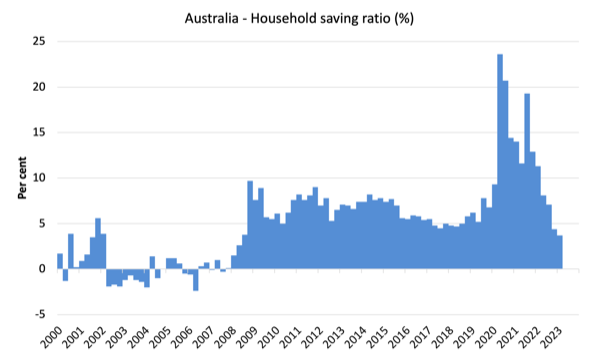

- The household savings rate (from disposable income) fell from 4.4% to 3.7%. So the squeeze on household wealth is having an effect, with the ratio falling sequentially.

Overall growth picture – growth continues at a much lower pace

ABS—— media release – explain:

Australia’s Gross Domestic Product (GDP) grew by 0.2% in the third quarter of 2023 (measured on a seasonally adjusted, quarter-over-quarter basis), compared with 2.3% in the third quarter of 2022…

It was the sixth consecutive increase in quarterly GDP, but the slowest since the COVID-19 Delta lockdown in the September 2021 quarter…

Gross private and public fixed capital formation was the main driver of GDP growth in the quarter…

Household spending continues to slow in Q3 2023…

The household savings-to-income ratio fell to 3.7%, the lowest level since the second quarter of 2008…

Net trade reduced GDP by 0.2 percentage points, exports increased by 1.8%, and imports increased by 3.2%.

The first graph shows quarterly growth over the past five years.

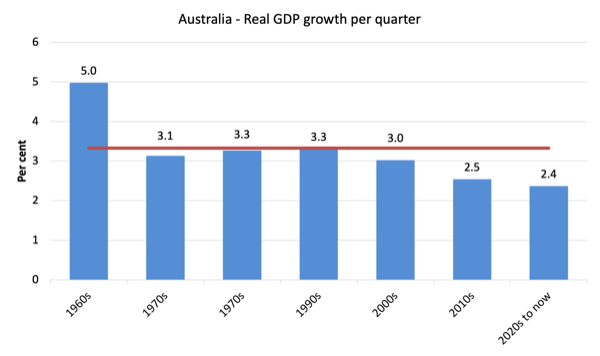

To put this in historical context, the chart below shows the ten-year average annual real GDP growth rate since the 1960s (the horizontal red line is the average (3.26%) for the entire period from the March quarter of 1960 to the March quarter of 2008 ).

The 2020-to-date average has been impacted by the pandemic.

But it is also evident that growth performance over the past two decades has been well below historical trends as the obsession with fiscal surpluses intensified on both sides of politics.

Even with our terms-of-trade gigantic household credit boom and once-in-a-century mining boom, our real GDP growth has been well below long-term performance.

The 1960s were the last decade in which the government maintained true full employment.

Analysis of Expenditure Composition

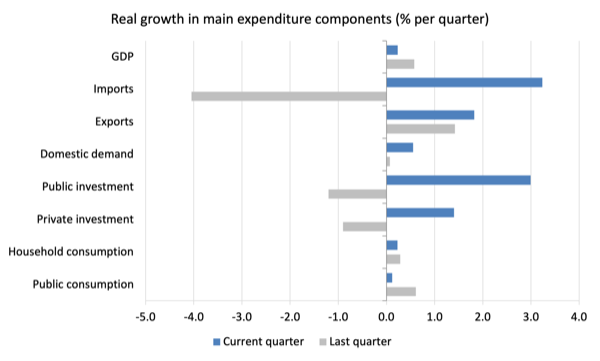

The chart below shows real quarterly percentage growth for the major spending components for the December 2022 quarter (gray bars) and the March 2023 quarter (blue bars).

Notes for the March quarter:

1. Household consumption spending grew by just 0.23% (down from 0.29%) – Spending growth has fallen over the past three quarters, while household saving is shrinking to support the current slumping growth.

2. General government consumption expenditure increased by 0.12% (less than 0.61%). Recurrent government spending is also now tightening.

3. Private investment spending rose 1.4% after falling 0.9% in the previous quarter.

4. Public investment increased by 2.99%, supported by large national and local government infrastructure projects.

5. Export spending increased by 1.8%. Imports increased by 3.2%).

6. Real GDP growth was only 0.23% (less than 0.6%).

contribution to growth

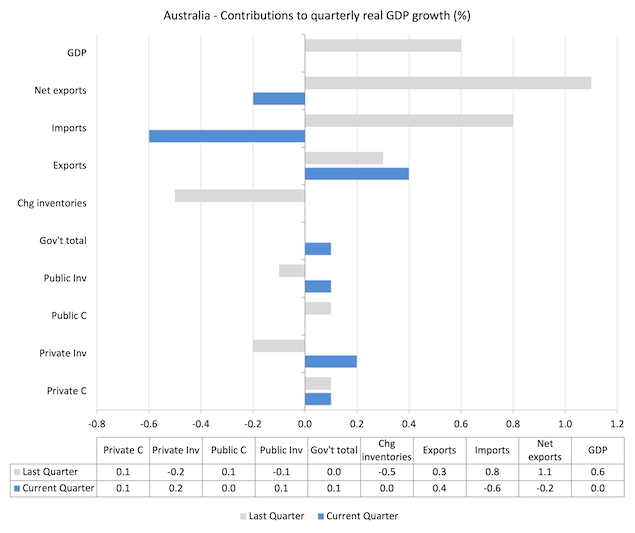

What spending components are added and subtracted from the 0.2% increase in real GDP in Q3 2023?

The bar chart below shows the contribution (expressed as a percentage) of the major spending categories to real GDP growth. It compares the March 2023 quarter’s contribution (blue bar) with the previous quarter (grey bar).

no order:

1. Household consumption expenditure contributed 0.1 percentage points to the overall growth rate (stable).

2. Private investment spending rose by 0.2 points (down 0.2 points in the previous quarter).

3. Public consumption increased by 0.0 point this quarter after increasing by 0.1 point in the previous quarter.

4. Public investment rose 0.1 point this quarter (down 0.1 point last quarter).

5. Overall, the government sector contributed 0.1 percentage point to economic growth (increase nothing in the previous quarter).

6. Inventory growth didn’t add anything (after decreasing by 0.5 percentage points in the previous quarter).

7. Net exports subtracted 0.2 percentage points from growth, with exports (+0.4 percentage points) offset by import growth (-0.6 percentage points) — remember, imports eat up spending.

The material standard of living rose slightly in the third quarter

ABS tells us:

A broader measure of changes in national economic well-being is real net national disposable income. The measure adjusts the quantitative measure of GDP for terms-of-trade effects, real net income from abroad, and consumption of fixed capital.

While real GDP growth (ie gross output measured in volume terms) increased by 0.2% in the March quarter, net real national disposable income growth increased by 0.9%.

How do we explain it?

Answer: The terms of trade rose to 2.8% in the current quarter from 0.3% in the December quarter.

The ABS noted, “The decline in import prices was driven by lower global oil prices and a stronger Australian dollar. This was the largest quarterly decline in import prices since December 2010. The decline in export prices was largely driven by rural and mining commodities.

The household savings rate fell 0.7 percentage points to 3.7%

The ABS states:

The household savings-to-income ratio fell to 3.7 percent, the lowest level since the June 2008 quarter… due to higher income tax and interest payables on housing and higher spending due to rising cost of living pressures…Household consumption grew faster this quarter than could Gross disposable income rises.

With inflation temporarily high and interest rates currently being pushed up by the RBA, tighter incomes have led households to sustain (moderate) growth in consumer spending by lowering their savings rates.

Drawing on savings to keep consumer spending flowing would weaken household wealth and is a limited process, especially given record levels of household debt.

The chart below shows the household saving rate (as a percentage of disposable income) from the March quarter of 2000 to the current period. It shows the period before the GFC, when the credit frenzy was in full swing and savings rates were negative compared to the rise during the GFC and the recent rise.

As things stand, households are being squeezed by rising costs of living and interest rates, as well as stagnant wage growth, which is widening the gap between income and spending.

If this trend continues, Australia will return to the pre-global financial crisis period when household savings rates were negative and consumption growth was sustained by increasing debt.

However, with household debt so high, households are likely to cut back on consumption spending and the economy will head into recession.

This would be an act of sabotage orchestrated by the RBA.

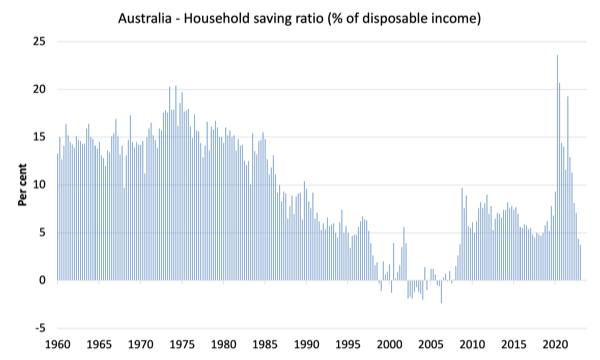

The graph below shows the household savings rate (as a percent of disposable income) from the March quarter of 1960 to the current period.

Back in the days of full employment, when governments ran persistent fiscal deficits to support the economy and employment (mostly), households saved a significant portion of their income.

During the neoliberal period, savings rates fell (to negative territory on the eve of the global financial crisis) as credit kept pouring down their throats.

The hope is that households will be able to repay the record levels of debt they are now carrying and improve their financial viability.

The table below shows the impact of the neoliberal era on household savings. These patterns are replicated around the world, making our economy more vulnerable to financial crises than it was in the pre-neoliberal decades.

Results for the current decade (2020-) are March 2020 averages.

| ten years | Average household savings rate (% of disposable income) |

| 1960s | 14.4 |

| 70s | 16.2 |

| 80’s | 11.9 |

| 1990s | 5.0 |

| 2000s | 1.4 |

| 2010s | 6.5 |

| 2020- | 12.3 |

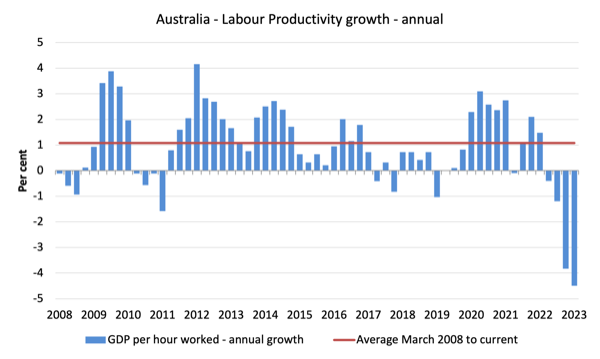

Real GDP growth rises but hours worked fall

Real GDP rose 0.2 percentage points in the quarter, while hours worked fell 0.8%.

The ABS reported that GDP per hour worked fell (despite the previous sentence implying a rise in productivity). So the numbers here are a bit fishy and I expect a revision next quarter.

The chart below shows the quarterly growth rates of real GDP and hours worked using national accounts data over the past five years to the March 2023 quarter.

Looking at the above figure from a different angle, the figure below shows yearly Growth in GDP (labor productivity) per hour worked from Q3 2008 to Q3 2023. The horizontal red line is the average annual growth rate (1.1%) since Q3 2008, which itself is an underestimated indicator of long-term trend growth of about 1.5% per year.

Relatively strong growth in labor productivity in 2012 and mostly above-average growth in 2013 and 2014 help explain why employment growth has lagged real GDP growth. Increased labor productivity means that each level of output requires less labor.

GDP per hour worked has now fallen over the past four quarters – a poor result.

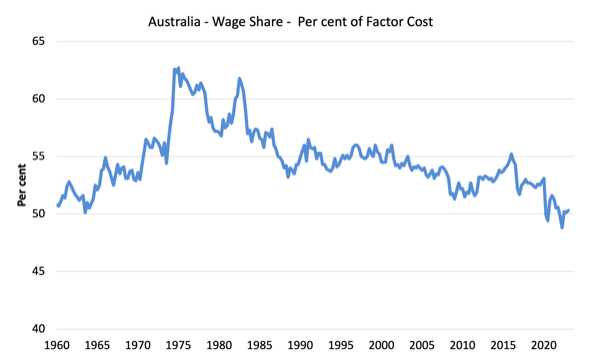

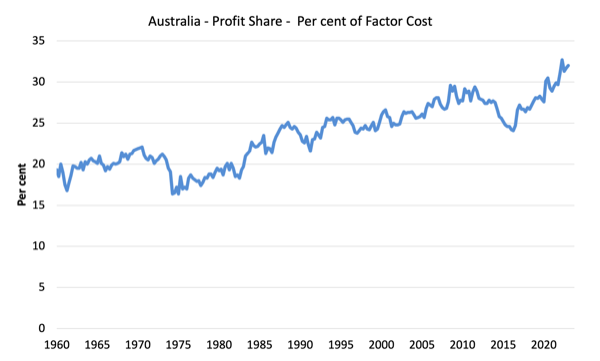

National Income Distribution – Basically Stable

Wages’ share of national income edged up to 50.3%, while the profit share rose by 0.3 percentage points as the terms of trade improved and corporate profits hit record highs.

The share of other claimants, such as the government, therefore fell slightly.

But as the chart below shows, the shift is insignificant in the face of recent trends.

The first graph shows the wage share in national income and the second graph shows the profit share.

Falling wage shares have historically been a product of neoliberalism, a trend that must eventually be reversed if Australia is to enjoy sustainable improvements in living standards without relying on record levels of household debt for consumption growth .

in conclusion

Remember that national accounts data is three months old – a backward view of the past – and using it to predict future trends is not straightforward.

The data tell us that growth continued to be modest in the March quarter after an initial rebound from the lockdown.

To sustain consumption growth in the face of rising interest rates and temporary inflationary pressures, households are now saving less relative to their disposable income.

I expect growth to fall further and we’re going to have higher unemployment and lower household wealth due to the RBA’s misjudgment.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}