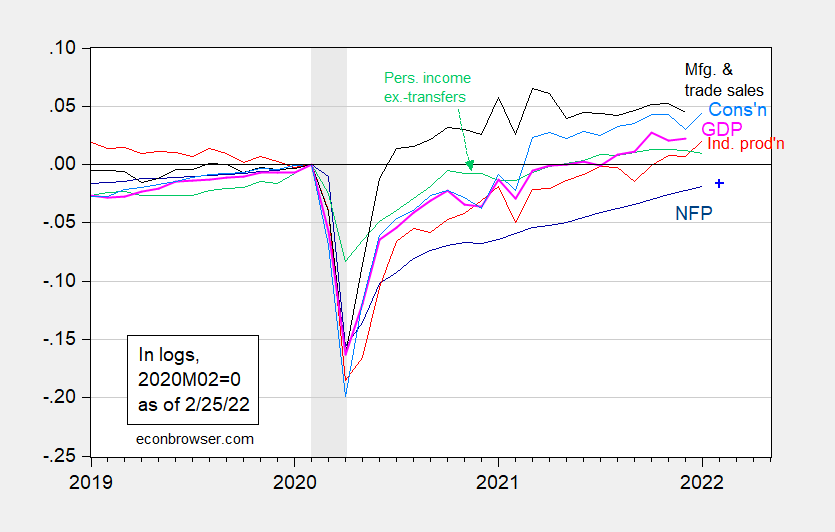

Personal income and consumption for January and manufacturing and trade sector sales for December were released last week. The PCE deflator for January has also been released, rounding out the January inflation data.

figure 1: Nonfarm payrolls (dark blue), Bloomberg consensus for February NFP (blue+), industrial production (red), 2012 dollars excluding transferred personal income (green), manufacturing and 2012 dollars Trade sales (black), consumption of Ch.2012$ (light blue) and monthly GDP of Ch.2012$ (pink), all normalized to 2020M02=0. NBER defines the decay date, peak to trough, shades of gray. Sources: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published Feb. 1, 2022), NBER, and author’s calculations.

Consumption continued to grow despite a drop in personal income excluding transfers.

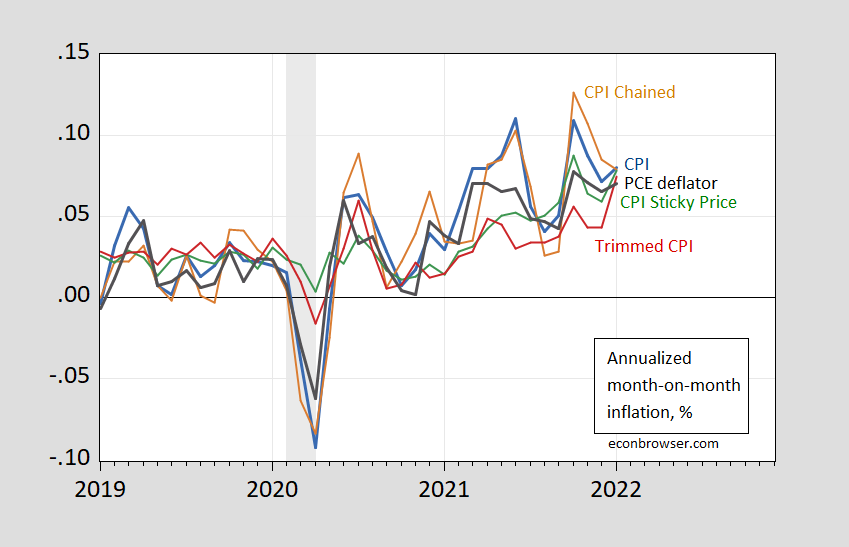

PCE Inflation (m/m) rose slightly – all other indicators except chain CPI rose slightly.

figure 2: CPI month-on-month inflation (blue), chained CPI (brown), 16% adjusted CPI inflation (red), sticky price CPI inflation (green), PCE deflator (black), all in decimal form (i.e. , 0.05 means 5%). Chained CPI (brown) seasonally adjusted using arithmetic bias. NBER-defined recession dates (peaks and valleys) shades of gray. Source: BLS, BEA, Atlanta Fed, NBER, and author’s calculations.

{kind=link}

{kind=link}