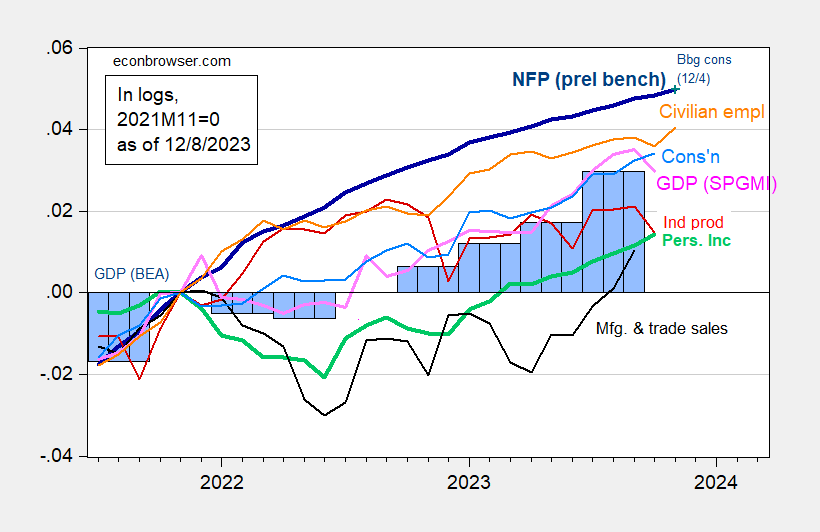

With the release of November non-farm payrolls (+199K vs. consensus of +180K), we can see the following NBER BCDC business cycle indicators (plus monthly GDP). The following employment series contains preliminary baseline revisions.

figure 1: Non-farm payroll employment incorporates preliminary benchmark (bold dark blue), using Bloomberg consensus implied levels as of 12/4 (blue+), civilian employment (orange), industrial production (red), excluding transfers in 2017 Personal income $ (bold green), Manufacturing and trade sales $ in 2017 (black), Consumption $ in 2017 (light blue), Monthly GDP $ in 2017 (pink), GDP, second Released (blue bar), all logs are normalized to 2021M11=0. Source: BLS via FRED, U.S. Bureau of Labor Statistics preliminary benchmarksFederal Reserve, BEA 2023Q3 2nd Edition, contains comprehensive revisions, S&P Global/IHS Markit (Nigerian macroeconomic consultant, IHS Markit) (12/1/2023 release) and the author's calculations.

Job growth shows continued strength in the economy. The participation rate rose 0.1 percentage points to 62.8 (0.1 percentage points above consensus), while the 4.0% year-over-year salary increase was in line with consensus.

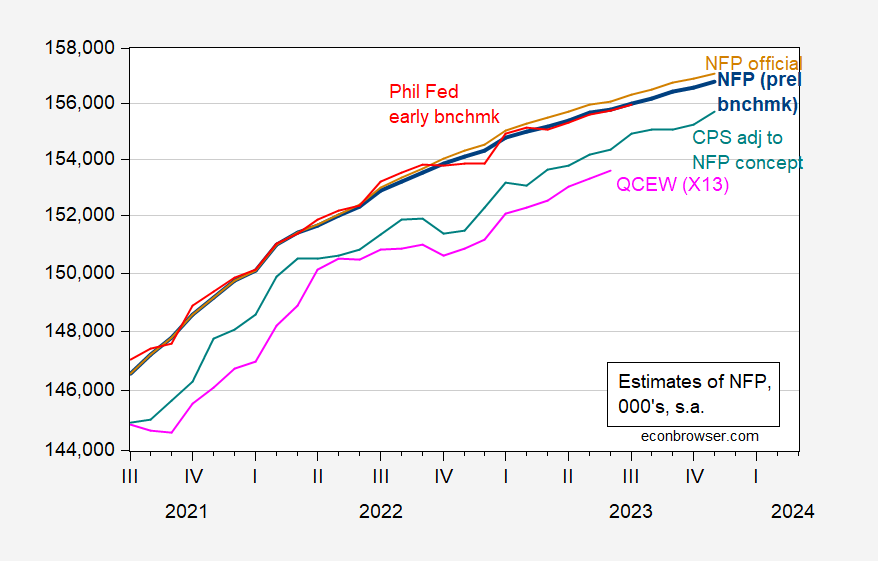

Lest anyone think the standard nonfarm payrolls data is being distorted, it's necessary to look at trends in other nonfarm payrolls indicators.

figure 2: Nonfarm payrolls (tan), nonfarm payrolls incorporated into preliminary baseline (bold dark blue), Philadelphia Fed early baseline (red), CPS civilian payrolls adjusted for NFP concepts (cyan), and author's use of X13 Seasonally adjusted QCEW total covered employment (pink), all 000's, sa Source: BLS via FRED, Philadelphia Fed, Bureau of Labor Statistics, BLS-QCEWand the author's calculations.

Census data ends mid-year, so we cannot rely too heavily on series based on that data to guide us. The Bureau of Labor Statistics (BLS) research series using CPS data adjusted for the Nonfarm Payrolls (NFP) concept actually grew faster than CES NFP data in November (3.7% m/m AR vs. 1.5%).

Incidentally, as we get more labor market data (including census-based data), it is becoming increasingly clear that the labor market is not in recession at least in the first half of 2022 (as some observers believe ).

{kind=link}

{kind=link}