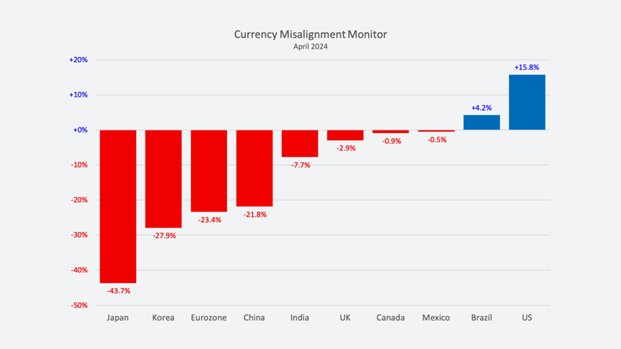

The Alliance for a Prosperous America and the Blue Collar Dollar Institute develop a measure of currency misalignments and report in their latest Currency Misalignments Monitor (April issue).

source: Certified Public Accountant.

Note that the US estimates are for multilateral equilibrium, whereas individual estimates are for USD/local currency changes implied by specific changes in the “equilibrium” exchange rate for individual countries.

I put the word “balanced” in quotes for a reason. CPA/BCDI estimates are based on the methodology employed William Cline's (2008) SMIM. Using trade elasticities, overvaluation is defined as the percentage of depreciation required to bring the current account into balance over time, requiring all other current account balances to remain consistent. However, Klein's approach does not assume that zero balance is the goal. So while the overall mathematical framework is the same (matrix, matrix!), the goals are very different. To see how crazy this zero balance standard is, it means that a “fair” exchange rate means a current account balance of zero, which in turn means a financial account balance of zero. In other words, in the medium term, countries will become neither borrowers nor savers. What this means for intertemporal models.

Note that intertemporal trade does not result in (in this case) a lower indifference curve.

See earlier CPA discussion of dollar value analysis, here. Discussion of measurement misalignment, here.Comparison with the IMF’s EBA here.

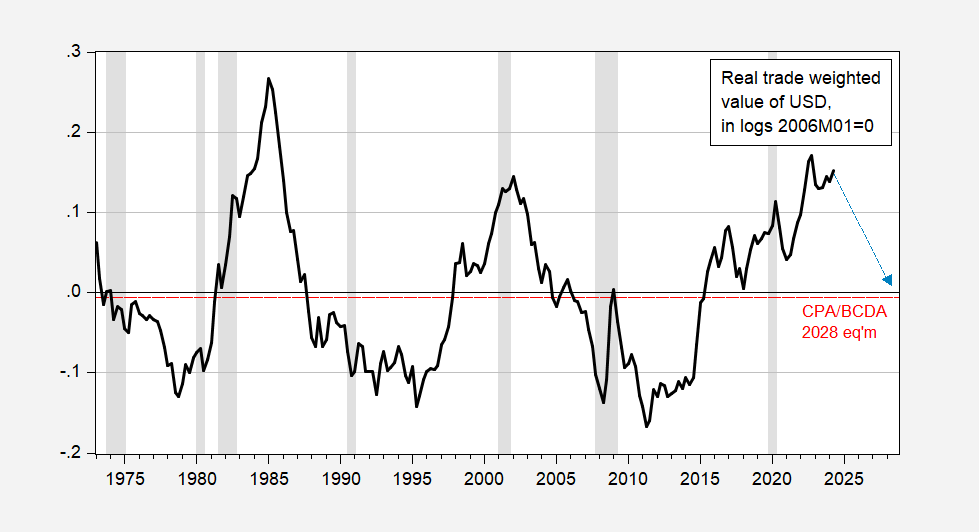

Here is the implied path for the US dollar to reach CPA/BCDI “equilibrium” by 2028.

figure 2: Broad real dollar value (black), 2028 CPA/BCDI “equilibrium” (dashed red line) and implied path (dashed blue arrow). NBER-defined recession peak-to-trough dates appear gray. Source: Federal Reserve via FRED, CPA/BCDI (April 2024)NBER, and author's calculations.

{kind=link}

{kind=link}