reader Bruce Hall Any discussion on the impact of trade policy is expected, including showing progress in manufacturing over the longest period of time. Without further ado, here’s what I could quickly glean.

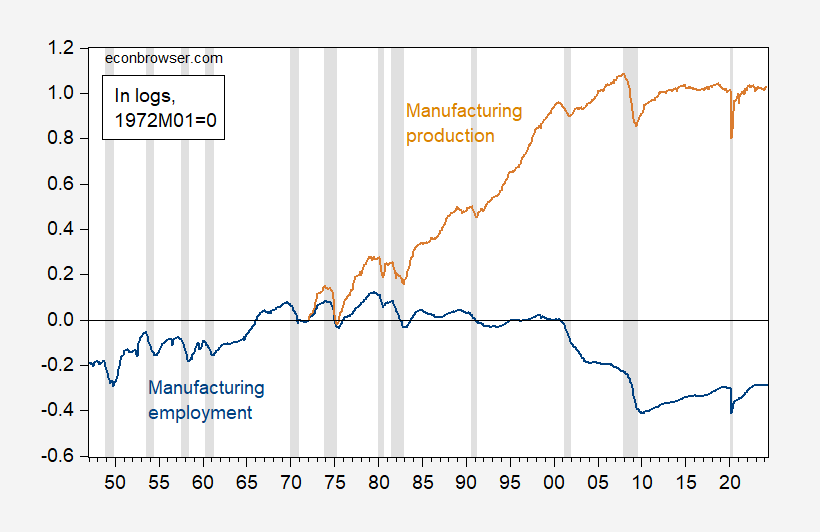

figure 1: Manufacturing employment (blue) and manufacturing production (tan), both seasonally adjusted and expressed in logarithms, 1972M01=0. NBER-defined recession peak-to-trough dates are in gray. Sources: BLS, Federal Reserve (via FRED, NBER), and author's calculations.

And in a shorter period of time:

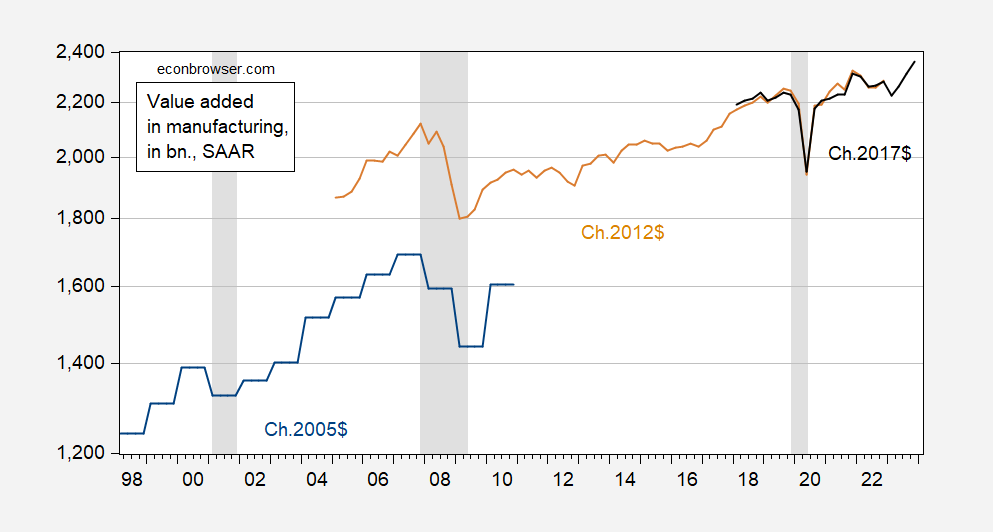

figure 2: Value added (billions) Ch.2005$ (blue), unit: billions. Ch.2017$(lack), all SAAR. NBER-defined recession peak-to-trough dates are in gray. Source: BEA, FRED, NBER, and author's calculations.

While total manufacturing employment is slightly above pre-trade war levels and manufacturing (total) output is almost flat, real value added is much higher than pre-trade war levels. The added value is much higher than when China joined the WTO.

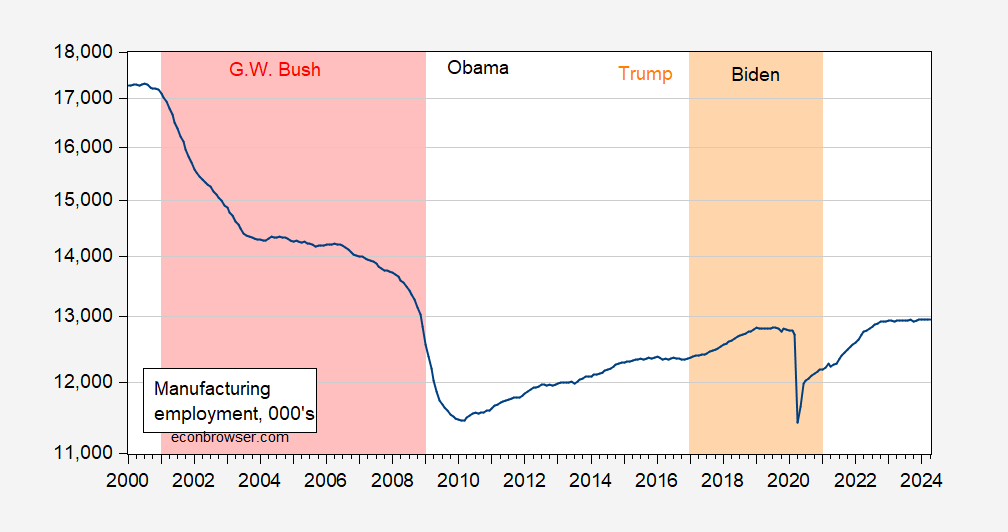

Addendum: When large-scale employment losses occur:

image 3: Manufacturing employment, 000, sa (blue). Source: BLS via FRED.

{kind=link}

{kind=link}