prestige(JME, 1984), and Tryon (1979) It is proved that the change in exchange rate does not equal the forward premium, which is the so-called forward premium mystery. Since the forward premium is equal to the spread in the absence of current and initial capital controls and no default risk – this finding is equivalent to the result that interest rates are unequal on average after accounting for exchange rate changes.

In other words, if the US default risk free bond yields 2% and the UK default risk free bond yields 5%, then the dollar no generally 3% appreciation against GBP to balance returns. For example, this finding could be explained by the existence of a time-varying exchange rate risk premium for sterling assets (relative to US dollar assets); however, it is not easy to find strong evidence for the determinants of this time-varying premium.

While the puzzle largely persisted for the next 25 years, it seemed to disappear during and after the global financial crisis — only to resurface in recent years.

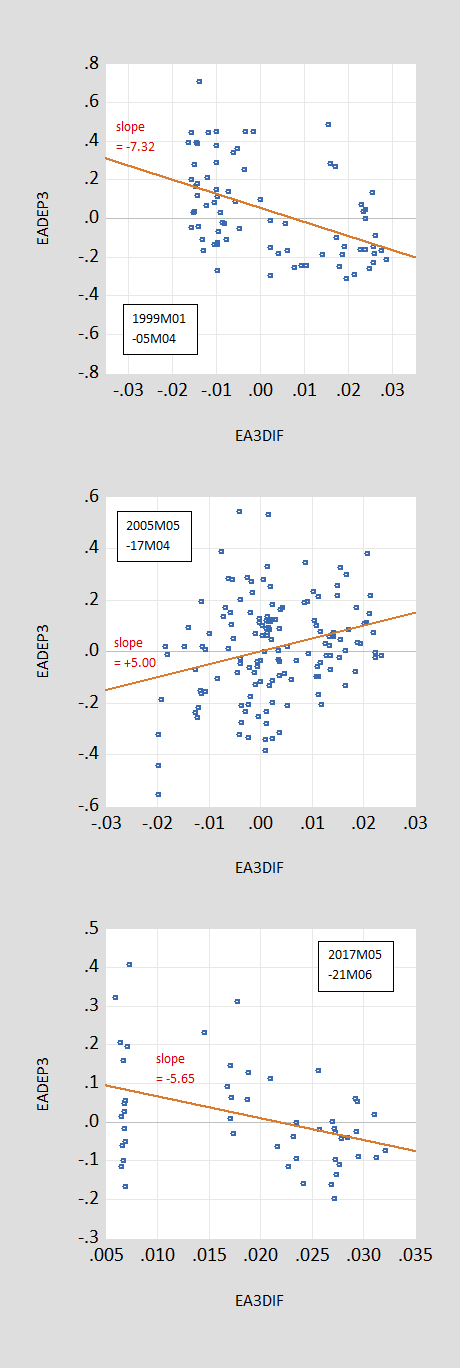

figure 1: 1999M01-2005M04 (top), 2005M05-2017M04 (middle) and 2017M05-2021M06 annualized depreciation of EUR/USD (vertical axis) relative to 3-month offshore USD-EUR spread (horizontal axis) ( The following figure). The sample is related to interest rate data, so the 1999M01-2005M04 sample includes ex post depreciation for the 3 months to 2005M07.

Recall this puzzle: if United If the Uncovered Interest Parity (UIP) assumption and perfect information rational expectations (sometimes called the unbiased assumption) hold, the slope of the regression line (red) will be indistinguishable from unity. In the top panels 1999M01-2005M04), the slope factor is significantly different from the value at 10% msl. (We cannot test UIP directly because market expectations for depreciation are not observed.) This coefficient reversal pattern applies to other USD-based exchange rates, as well as other currency pairs (with a few exceptions).The fact that the coefficient is positive in the post-global financial crisis period is what we call the “new Fama dilemma”, in the newly revised NBER Working Paper No. 24342 (non-gated version work documents),and Laurent Ferrara (SKEMA Business School), Mathieu Bussier (Bank of France), and Jonas Hepperts (Columbia Business School).

Outstanding interest parity is one of the most central concepts in international finance. Meanwhile, empirical proof of the concept proved elusive.In fact, the company’s failure United The uncovered interest parity (UIP) assumption and rational expectations (sometimes called the unbiased assumption) are among the most robust empirical laws in the literature, since Fama (1984) Interest rate differentials were found to point in the wrong direction for subsequent exchange rate ex post changes.

The most common explanations – such as the existence of an exchange rate risk premium, leading to a wedge between forward rates and expected future spot rates – have some empirical validation, albeit fragile (we are investigating returns on assets such as GBP, JPY, etc.) rate, Swiss francs, not Chinese yuan or Argentine pesos). In our explanation, we will take an alternative approach related to expectations, for the reasons described below.

In the middle panel of Figure 1 (2005M05-2017M04), we show that the slope coefficient flips to a positive 5.0, significantly different from the uniform value. Finally, in the bottom panel of Figure 1 (2017M05-2021M06), the slope coefficient flips to a negative value again, which is -5.65. (In this article, we looked at 1-year maturities and 1-year spreads, but the pattern of results is the same.)

One might be tempted to attribute this trend to a positive coefficient over the medium term to reduce risk; this does not seem plausible since periods during financial crises are marked by high risk, certainly taking the VIX as an example. In any case, adding regression with VIX did not change these slope coefficient estimates.

Using survey-based expectations—thus abandoning the rational expectations assumption—the data provide the following insights.First, spreads and expected exchange rate changes are positively correlated across all subsamples considered, consistent with the proposition that investors tend to equate at least some expected returns expressed in common currencies (see also Chinn and Frankel (2020) 1986-2017 results).

Second, the transformation of the beta coefficients arises because the correlation between expectations error (defined as expectations minus actuals) and spreads has changed significantly during the pre-crisis and post-crisis periods. This is important and can be seen by examining the probability limit of the β’ coefficient in the Fama regression:

s+1 – s = α’ + β'(ii*) + error

so:

Prim (β’) = 1 – [A] – [B] – [C]

Where

[A] ≡ (Covered interest difference, ii*)/Where(two*)

[B] ≡ (risk premium, ii*)/Where(two*)

[C] ≡ (prediction error, ii*)/Where(two*)

Coverage spread = – [(f – s) – (i-i*)]

risk premium = F – ε (s+1)

prediction error = ε(s+1) – s

F is the forward rate for the period +1

s is the current spot rate

ε (s+1) are subjective market expectations of future spot exchange rates (using the Consensus Forecasts survey data proxy).

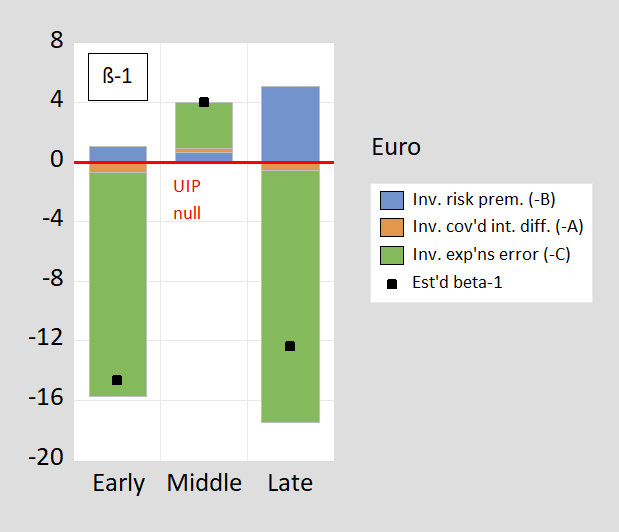

The breakdown of EUR/USD (β’-1) is shown in Figure 2 below, for the same sub-period (for the annual range, as described in this paper). Components are shown as theoretical β’-1+ [-A] + [-B] + [-C], which add up to the estimated β’-1 (i.e. UIP null, red line).

figure 2: EUR/USD breaks down β’-1. [A] is brown, [B] is blue, [C] are green; the black squares represent the estimated β’, the line at 0 represents the theoretical β’-1 under the unbiased assumption, both on a 3-month time horizon. Black squares represent OLS point estimates. The early stage is 1999M01-2005M04, the middle stage is 2005M05-2017M04, and the late stage is 2017M05-2021M06. Source: Author’s calculations (calculated for 1 year span BCFH (2022).

The linkage of exchange rate risk to spreads is not the main reason why the slope coefficient changes from positive to negative (although the changing behavior of exchange rate risk does play a role, as shown by the changes in the blue bars).Rather, it is crucial how the expected error co-occurs with the spread – i.e. [C] Components (green bars). This correlation changed as the dollar was expected to weaken during the crisis/post-crisis period (2005M05-17M04).

Note that the spreads covered (which have widened after the financial crisis and more recently with financial reforms raising the cost of hedging) and their correlation with spreads do matter – but with expected errors and their linkage to spreads. Therefore, we are not ignoring this development (remember, we are using offshore yields, so the spread covered cannot be attributed to capital controls.).For more discussion see here postal, and through Du, Tepper, and Ferdelhan (2018) (non-gated version).

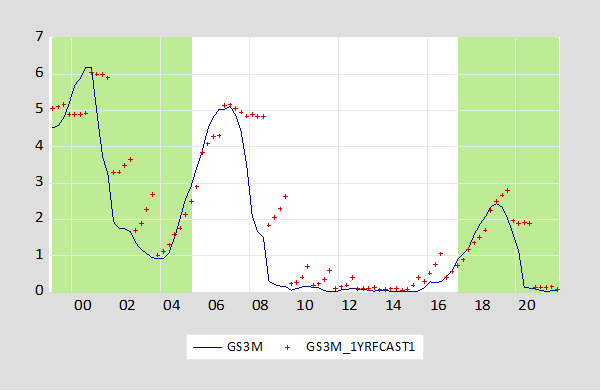

Why is this happening? We speculate that this has to do with market expectations that U.S. interest rates will rise faster than they actually are (and therefore a stronger dollar), especially until clear forward guidance is implemented. This conjecture is illustrated using actual 3-month Treasury yields (very close to the offshore 3-month Treasury yields used in this article).

image 3: Three-month Treasury yields through the third quarter (blue line) and survey of professional forecasters’ mean forecasts (red +), expressed as a percentage. Green shading indicates early, late. Source: Federal Reserve Board, Philadelphia Fed.

Finally, note that in our later period, after U.S. interest rates rose from the zero lower bound, the original negative coefficient reappeared as rate expectations moved closer to what happened.This finding is in addition to the findings we previously described in our study Older (2019) post.

A major implication of our findings – which goes beyond the results of the regression coefficients between now and then – is that the characteristics of exchange rate expectations are important, perhaps more so than the risk properties of highly fungible (dollar) assets.

Unrestricted version of the paper, here.

{kind=link}

{kind=link}