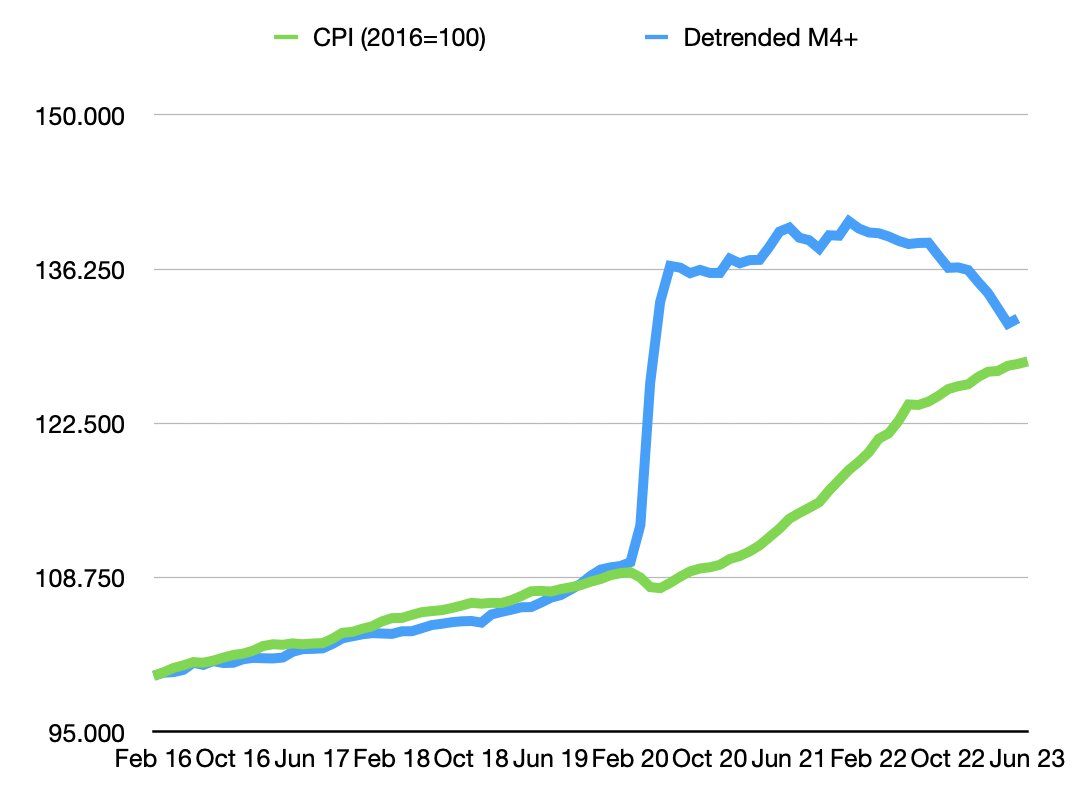

reader economical Ask me to critique ecomonetarism.I don’t have an overall assessment, but I will say I don’t understand how (1) Cameron Harwick The conclusion that the case for ecomonetarism is justified by the inflation results, and how the related (2) graph below is constructed, is what I believe to be the basis for that conclusion.

Here’s Harwick’s diagram.

source: C. Harwick (2023).

Certainly, the chart seems to indicate that by June 2023, the actual price level and the currency (detrended) will be very close.

Unfortunately, the article doesn’t say how the M4+ de-trends. Apparently something other than the Hodrick-Prescott filter is being used (I tried).

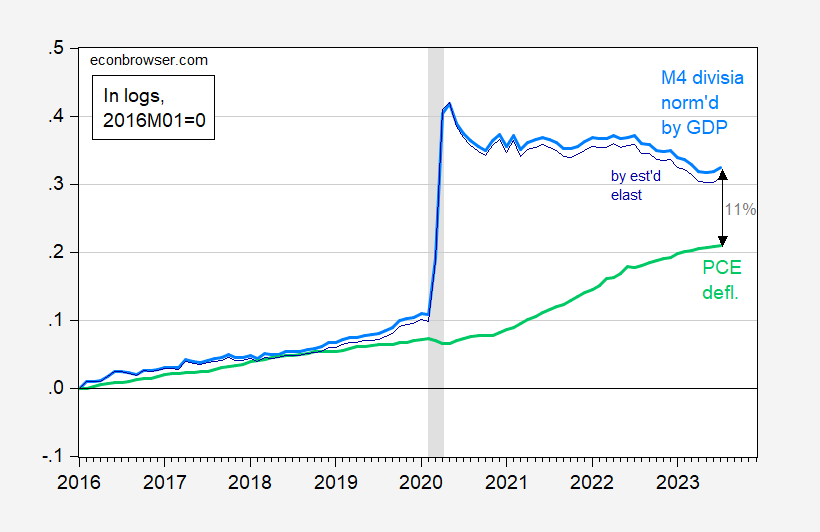

I remove the trend by dividing by GDP, which is consistent with some versions of quantity theory. This produces a similar picture (in log form):

figure 1: PCE price deflator (light green), M4 divided by real GDP (light blue), M4 divided by GDP to the power of 1.1 (dark blue), all expressed in logarithms, 2016M01=0. Recession peak-to-trough dates as defined by NBER are grayed out. Source: Bank of East Asia, cleveland fed, SPGMI, chronic fatigue syndromeNBER, and author’s calculations.

[Observations for 2023M07 for PCE deflator is the Cleveland Fed nowcast as of 8/29; for GDP is forecasted using lagged GDP and current NFP.]

As of July, the gap between the price level measured using the PCE deflator and the normalized division M4 was 11%. One could argue that using GDP to detrend is inappropriate; perhaps it would be better to use the income elasticity of real money demand estimated from the money demand equation. Using Johansen for the period 1967-2019 gives an elasticity of about 1.1. Using this estimate results in a 10% gap (and growing!).

As an aside, If we live in a monetarist world with flexible prices, then the price level should rise at the same time as the Divisia currency increases, about 30%. Obviously, that didn’t happen.

Finally, to differentiate models, one may have to compare predictive power (e.g., here).I haven’t done a comparison recently, but I estimated Expectations and supply shocks strengthen the Phillips curve. If one thinks about how inflation has fallen recently with measured cost-push shocks (e.g. NY Fed GSCPI), one might argue that the Phillips curve makes more sense than quantity theory.

{kind=link}

{kind=link}