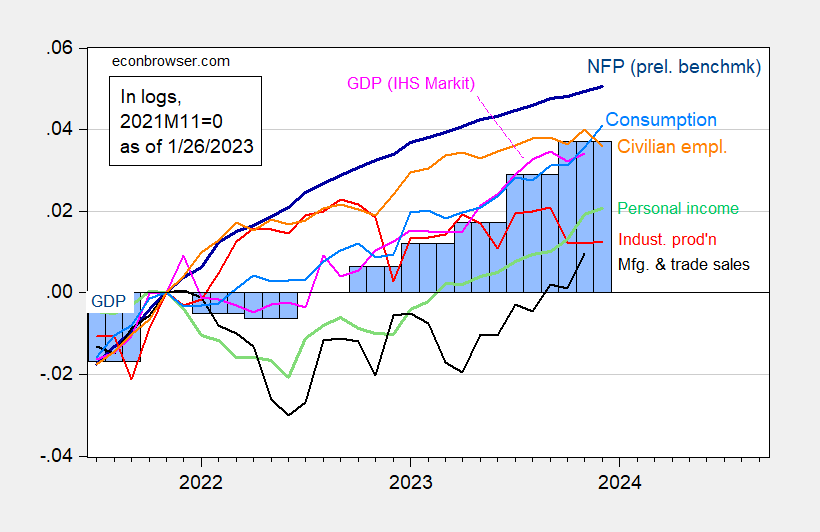

back Yesterday's GDP release (discussed by Jim), actual personal consumption continued to rise, exceeding market expectations (monthly rate +0.5%, Bloomberg +0.3%), while nominal personal income reached market expectations of +0.3%. Here are some of the key indicators followed by the NBER Business Cycle Dating Committee along with a picture of monthly GDP.

figure 1: Non-agricultural employment is included in the preliminary benchmark (bold dark blue), using the Bloomberg consensus implicit level as of 1/3 (blue+), civilian employment (orange), industrial production (red), excluding current employment in 2017 Transferred personal income $ (bold green), 2017 manufacturing and trade sales $ (black), 2017 consumption $ (light blue), 2017 monthly GDP $ (pink), GDP second release (blue Color bar), all logarithms normalized to 2021M11=0. Source: BLS via FRED, U.S. Bureau of Labor Statistics preliminary benchmarksFederal Reserve, BEA 2023Q3 2nd Edition, contains comprehensive revisions, S&P Global/IHS Markit (Nigerian macroeconomic consultant, IHS Markit) (1/2/Released in 2024) and the author's calculations.

Outside of industrial production, it's difficult to see a decline in the data reported so far.

For data related to the new year, Lewis-Mertens-Stock New York Federal Reserve Weekly Economic Index (WEI) For the week ending January 20, the reading was 1.90%.this Builder Leva Leon Sims The weekly economic conditions index was -0.10%. If the US GDP trend is 2%, then this also means a growth of 1.90%.

{kind=link}

{kind=link}