this December 2022 employment release Provides the latest available monthly data on economic conditions. Here are the various labor market indicators:

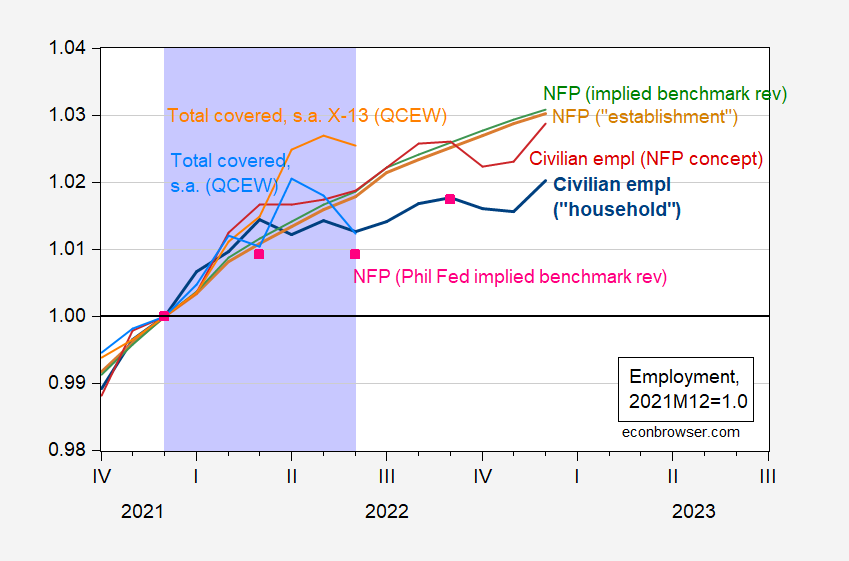

figure 1: Civilian employment over age 16, FRED series CE16OV (bold blue), civilian employment adjusted for nonfarm employment (red), nonfarm employment, FRED series PAYEMS (tan), adjusted to reflect authors’ preliminary baseline revision Nonfarm payrolls series (green), Philadelphia Fed adjusted nonfarm payrolls to reflect preliminary benchmark revisions (pink squares), total employment covered by the Quarterly Census of Employment and Wages (QCEW), X-13 conducted by the authors Census adjusted (orange), QCEW adjusted by geometric moving average (sky blue), both expressed relative to 2021M12 values, both seasonally adjusted. The lavender shading represents (by Mr. Steven Kopits) a hypothetical peak-to-trough recession in 2022H1.Source: CE16OV from BLS via FRED’s PAYEMS, Preliminary Benchmark Series constructed by the author Using data from the BLS, Federal Reserve Bank of Philadelphia, Alignment of civilian employment with the BLS concept of NFPQCEW from BLS, and the authors’ calculations.

If you consider the household series to be a better measure of employment than institutions, then – in assessing trends in the non-agricultural sector – the estimated employment change from end-2021 would not differ much if the series were made compatible in terms of coverage (ie, tan line vs. red line).

why? This was due to a (overall) jump in December’s civilian employment series. Figure 2 shows extreme volatility in the household series as well as large corrections. This is why macroeconomists tend to focus more on firm series than on household series (Furman (2016); China Eastern Airlines (2017); Goto et al. (2021)).

figure 2: Nonfarm payrolls change from October release (green), November release (tan), December release (blue) and Bloomberg consensus (sky blue squares); data from October release (purple), November release Civilian employment change starting with data released (yellow green) and data released in December (red), all in thousands, sa Source: BLS via FRED, various releases, Bloomberg, and author’s calculations.

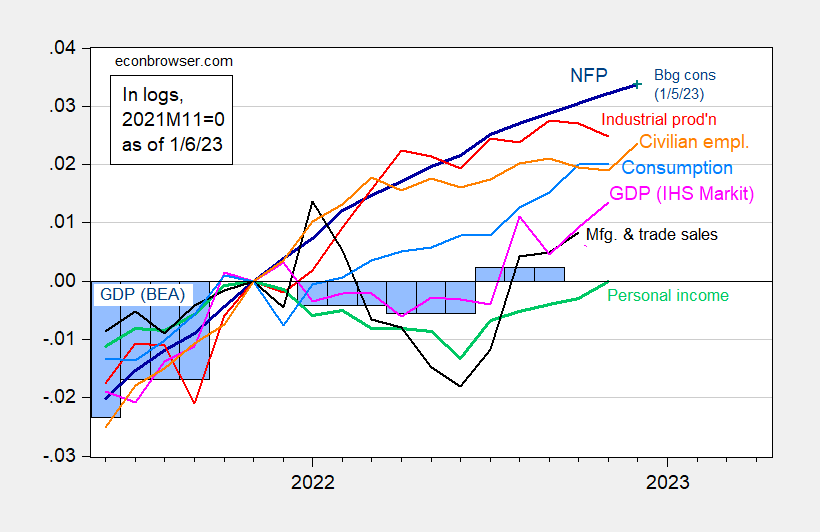

What do business cycle indicators look like given the employment data? This is shown in Figure 3 below.

image 3: Non-farm payrolls, NFP (dark blue), Bloomberg 1/5 consensus (blue+), civilian employment (orange), industrial production (red), China 2012 personal income excluding transfers (green), manufacturing and Trade Sales Ch.2012 USD (black), Ch.2012 USD Consumption (light blue) and Ch.2012 USD Monthly GDP (pink), GDP (blue bars), all log normalized to 2021M11=0. Sources: BLS, Federal Reserve, BEA, from FRED, IHS Markit (nee Macroeconomic Advisers) (published 3 January 2023), and authors’ calculations.

Taken together, the economy appears to have maintained its momentum in November-December, before recognizing NBER BCDC’s focus on non-farm payrolls and personal income transfers. JOLTS data point to tight labor market in November.

I might also note that, in a way, the Civilian Employment series peaked before the NFP series (In the last four recessions, the commons peaked ahead of the NFP 50% of the time and 50% of the time), then our fears of a recession that had already begun in November would be eased.

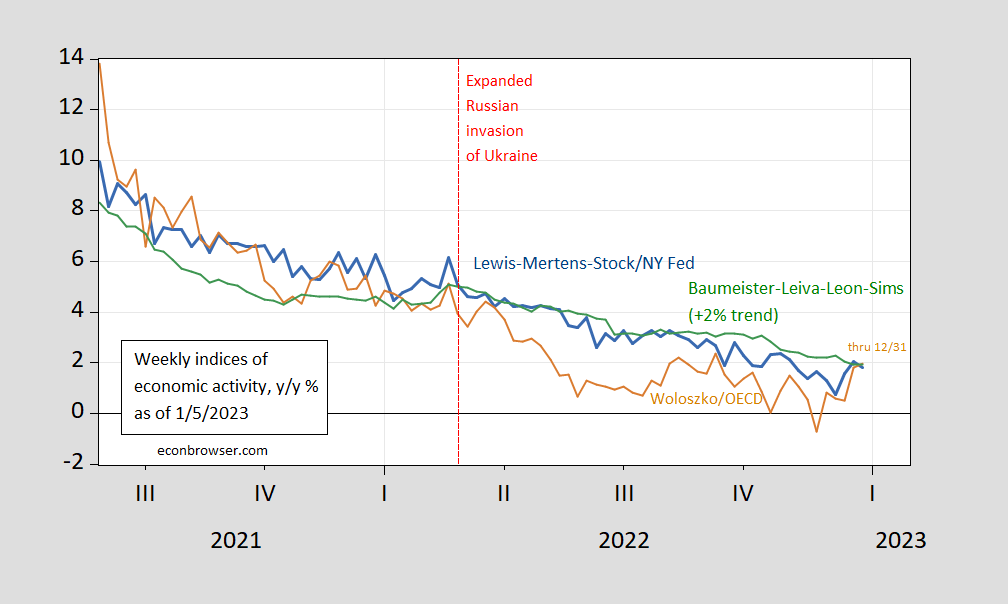

We gain additional insight from our weekly economic indicators, which cover data through December 31.

Figure 4: Lewis-Mertens-Stock weekly economic index (blue), OECD weekly tracker (tan), Baumeister-Leiva-Leon-Sims US weekly economic conditions index plus 2% trend (green).Source: New York Fed via fred, OECD, WECIand the authors’ calculations.

A WEI reading of 1.8% for the week ended December 31 could be interpreted as a 1.8% year-over-year growth rate if the 1.8% reading persisted throughout the quarter. The reading of 2.0% in the weekly OECD tracker index can be interpreted as a year-on-year growth rate of 2.0% as of December 31.this Baumeister et al. A reading of -0.1% is interpreted as a growth rate of -0.1% above the long-term trend growth rate. US GDP growth averaged around 2% over the 2000-19 period, so this translates to 1.9% annual growth through 12/31.

{kind=link}

{kind=link}

{kind=link}