Based on September employment data released today (Bloomberg consensus 336,000 vs. 170,000), we get the following economic picture.

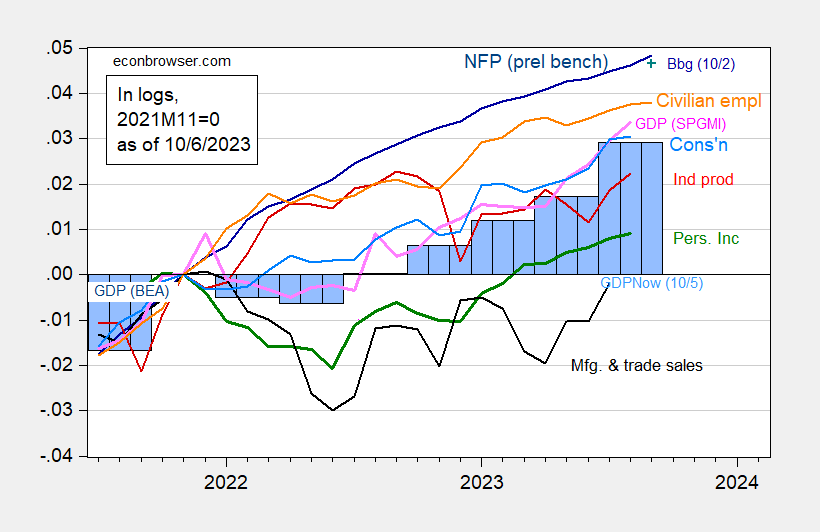

figure 1: Nonfarm Payroll employment included in preliminary benchmark (dark blue), Implied September NFP included in Bloomberg 10/2 consensus (blue+), civilian employment (orange), industrial production (red), 2017 excluding transferred individuals Income (green), Manufacturing and trade sales $ in 2017 (black), Consumption $ in 2017 (light blue), Monthly GDP $ in 2017 (pink), GDP (blue bars), all logarithms All are normalized to 2021M11=0. Source: BLS via FRED, U.S. Bureau of Labor Statistics preliminary benchmarksFederal Reserve, BEA 2023Q2 released for the second time through FRED, S&P Global/IHS Markit (Nigerian macroeconomic consultant, IHS Markit) (10/2/2023 release), Federal Reserve Bank of Atlanta (released October 5, 2023), and author’s calculations.

Figure 1 shows nonfarm payrolls incorporated into the preliminary baseline, which revised March 2023 employment downwards by 306,000. Figure 2 shows a comparison of the official series (tan) with alternative indicators of employment in non-agricultural employment.

figure 2: Nonfarm payrolls (tan), NFP employment including preliminary baseline calculated by the authors (bold blue), Philadelphia Fed early baseline (green), household employment adjusted to conform to NFP concepts (light blue), and Employment covered by QCEW adjusted for Tenth Census – 13 authors (red), all in thousands, seasonally adjusted. Sources: BLS via FRED, Federal Reserve Bank of Philadelphia, BLS, BLS-QCEW, and author’s calculations.

The home series adjusted according to the NFP concept looks softer than the CES series. However, this partly reflects weak readings from the CPS survey (see Figure 1, orange line).

As of September 2023, there is still no significant recession, although these figures will be revised and therefore cannot be guaranteed.

{kind=link}

{kind=link}