Many researchers are interested in how cost sharing affects health care utilization, costs, and patient outcomes. This is especially true as high-deductible health plans (HDHPs) become more common in the United States. 2023, 29% of covered workers in the United States have an HDHP.

Claims data is a useful data source for analyzing HDHP. However, there are some challenges with using this data:

The first [of claims data] Includes detailed information about plan structure, but generally has less externality validity because it typically comes from a single health insurance company or a small group of participants. The second type improves external validity by aggregating across insurance companies, but typically does not include the plan structure variables needed to distinguish HDHPs from plans with lower deductibles, or to explain what the binary “HDHP” variable represents.

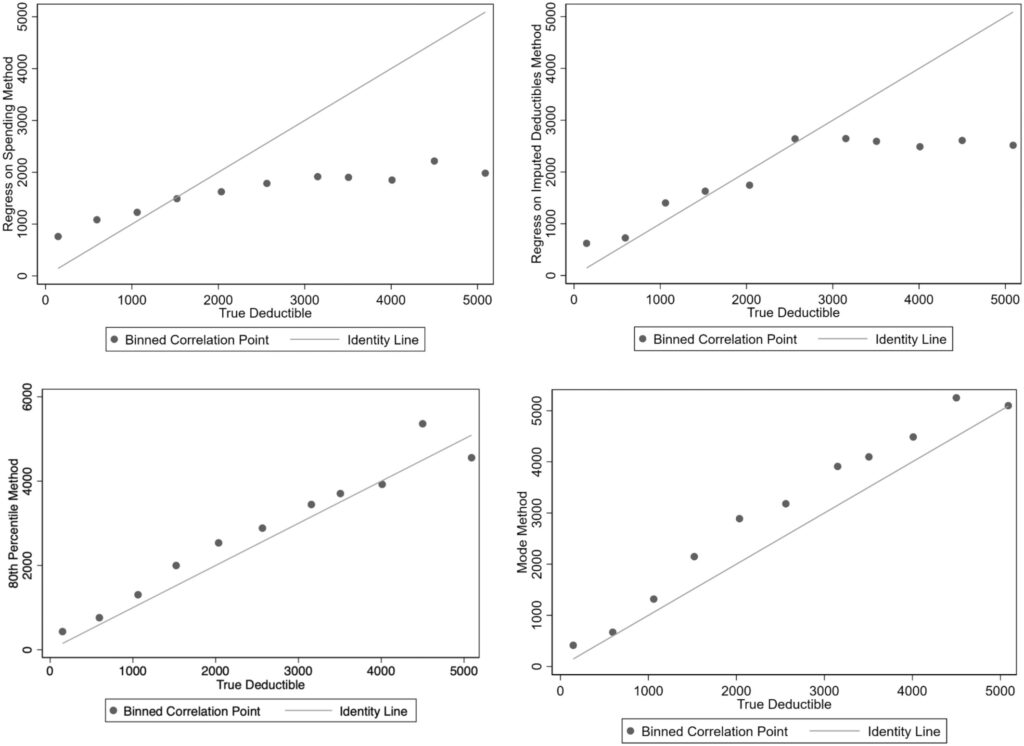

A paper by Cliff et al. (2024) Designed to examine how well claims data from Optum Labs data predicts plan deductibles. Optum data does include plan deductible information used as the “gold standard.” Four different imputation methods are used:

- Expenditure parameter forecast (expenditure regression method). Participants' annual deductible spending is regressed on their total annual spending (plan plus out-of-pocket expenses), common demographic covariates (gender and age), and fixed effects for each plan. Regression is used to predict the plan fixed effects setting. Deductible based on a certain level of expenditure. The coefficients of the best-fit regression model were used to predict each plan's deductible at a fixed total spending amount (which the authors set at $10,000 to exceed most deductibles).

- Parametric forecasting with imputation and planning features (regression with imputation deductible method). This method uses two phases. First, enter deductibles for an easily identifiable subset of plans. For the second stage, a set of covariates is established describing observed deductible expenditures and plan characteristics, and profiles are collapsed to the plan level. Using a subset of plans with estimated deductibles, the estimated deductibles are regressed on the set of covariates; the resulting coefficients are then used to predict deductibles for plans that could not be estimated in the first stage.

- Modal Deductible Expenses (Modal Method). This simple method enters the highest (non-zero) modal deductible expense amount for a participant in the plan and applies this deductible to all participants in the plan.

- 80th percentile of deductible expenses (80th percentile method).The following Labido(2021), which tracks personal expenses month by month, and individuals who experience an increase in expenses but no change in deductible expenses in a given month are considered to have met their deductible. The individual-level data are then collapsed to the plan level, and deductibles for all participants in the plan are set to the 80th percentile of the plan's annual deductible spending.

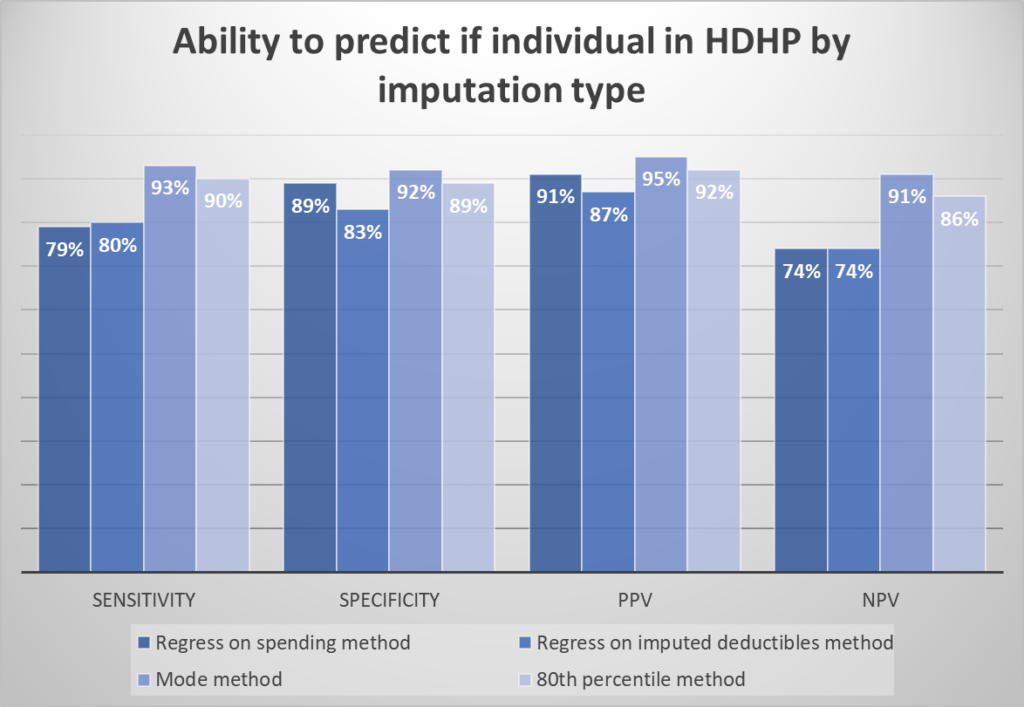

To assess the accuracy of the imputation methods, the authors calculated the sensitivity, specificity, and positive/negative predictive value (PPV/NPV) of each method for classifying participants into HDHP versus non-HDHP plans.

Surprisingly, the simple “pattern approach” performed best at classifying individuals as HDHP versus non-HDHP. It also does a good job of predicting deductible expenses.

The mode method performed best; 72% of plans were correctly classified into each category, and 69% of plans had estimated deductibles within $250 of actual deductibles.For this method, limiting the estimate to groups with more than 50 participants improved the sensitivity to 85% of plans correctly classified by category and reduced the average difference between estimated and actual deductibles from $700 to $496

You can read the full article here.

{kind=link}