as mentioned Jim in his post on Q3 2022 GDPexports and imports (mechanically) account for more than 100% of GDP growth in Q3 2022:

figure 1: Top panel: GDP growth (blue); Bottom panel: consumption, investment and government spending (blue bars), exports (tan), imports (green), all expressed as a percentage, q/q SAAR. Source: BEA, 2022Q3 advance release and author calculations.

The increase in real exports of goods and services and the decrease in real imports accounted for 2.8 percentage points of the increase of 2.6 percentage points, q/q SAAR. Domestic components (C, I, G) declined from a major contributor to overall growth in Q4 2021 to slightly negative growth in Q3.

In other words, the domestic component of aggregate demand is weakening, as further confirmed by the sequential increase in final sales to private domestic buyers compared to GDP.

figure 2: Real GDP growth (blue), GDPNow forecast 10/28 (sky blue squares), real growth in final sales to private domestic buyers (tan), all in %, q/q SAAR. Source: Bank of East Asia, 2022Q3 advance release, Atlanta Fedand the authors’ calculations.

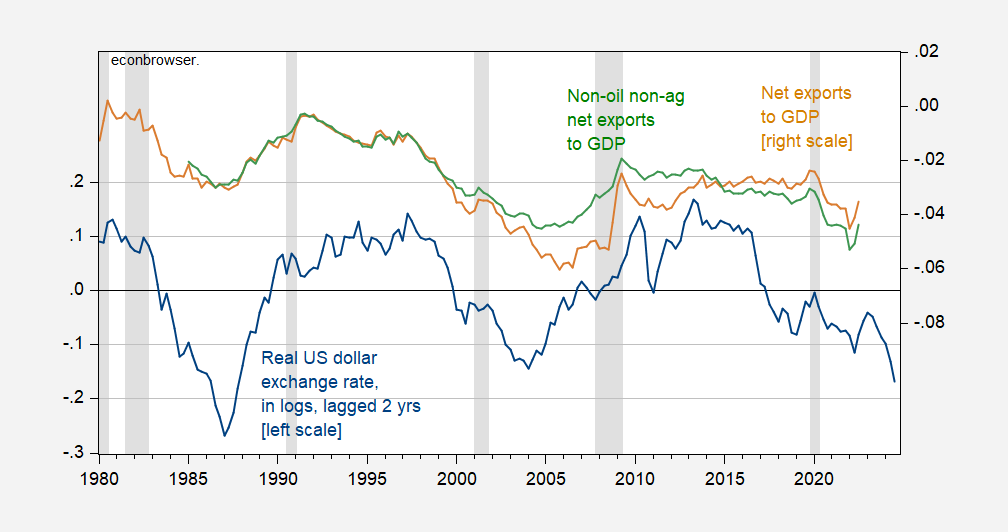

How might the external environment affect GDP? This is net exports (gross, ex-agricultural exports, ex-oil) as a percentage of GDP, compared to changes in the real dollar exchange rate.

image 3: Real U.S. dollar trade-weighted log exchange rate, two-year lag (blue, left scale), net exports to GDP (tan, right scale), net exports to GDP excluding agriculture, excluding oil (green, right scale). The NBER recession dates from peak to trough are shaded in gray. A fall in the exchange rate means an appreciation of the dollar. Trade weights for exports of goods up to 2015, followed by exports of goods and services. Source: Federal Reserve via FRED, BEA 2022Q3 Advance, NBER and author’s calculations.

The rebound in the third quarter was partly attributable to the currency’s weakness in the third quarter of 2020. The graph shows that net exports are likely to deteriorate again in the near future as the dollar’s appreciation reduces competitiveness.

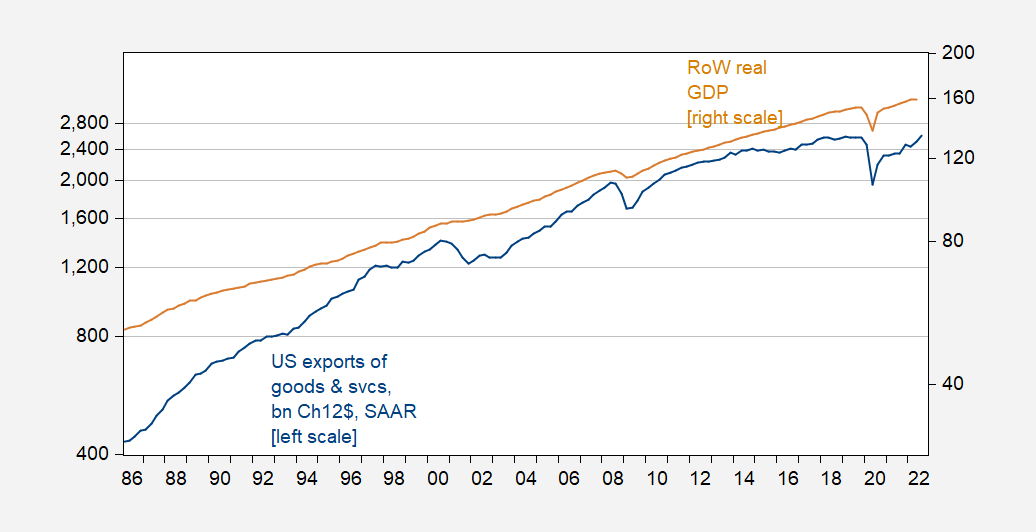

As discussed in these posts, exports also depend on foreign economic activity. As shown in Figure 3 below.

Figure 4: U.S. exports of goods and services, billion Ch.12$ SAAR (blue, right log scale), rest of the world export-weighted GDP (tan, right log scale). Source: BEA 2022Q3 Advance, Dallas Fed database of global economic indicators.

Long-term relationship between exports (expgs), GDP of the rest of the world (Yes*) and the real exchange rate (q) Yes:

expgs = 1.1 Yes* + 1.43 q

For 1986-2022Q2, estimated using Johansen’s maximum likelihood method.This is slightly lower than the reported income elasticity and price elasticity Chin (2010)but contains later samples than reported there.

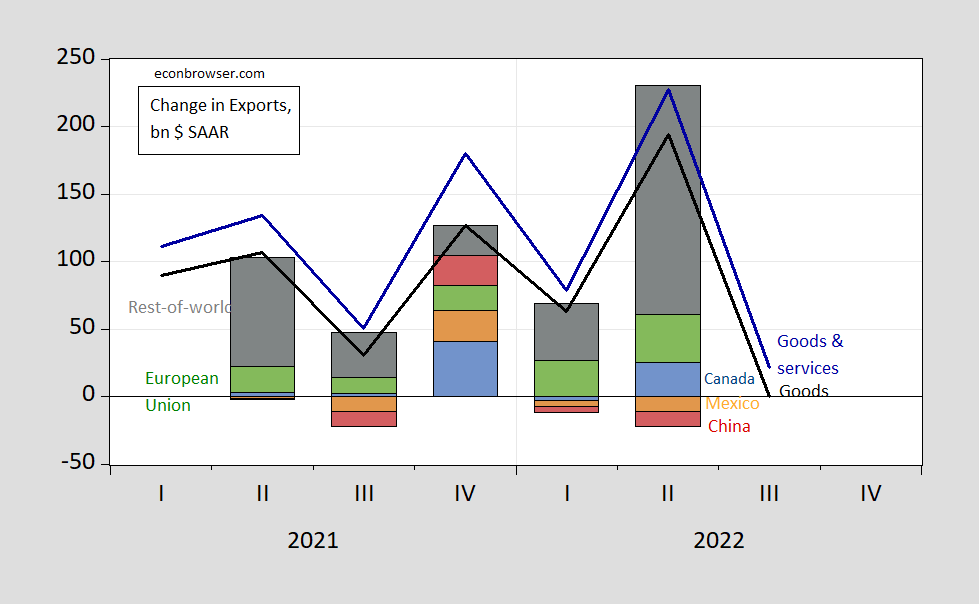

We can show the geographic contribution to the change in q/q of merchandise exports, at least in the second quarter.

Figure 5: Goods and Services Nominal Exports (blue), Goods (black), Nominal Exports to Rest of World (grey bars), EU (green bars), Canada (blue bars), Mexico (tan), China (red) change), in billions of dollars, q/q SAAR. Source: BEA 2022Q3 Advance, published by BEA/Census International Trade, author’s calculations.

While we are (rightly) concerned about China, China’s direct aggregate demand for US goods is small (and probably not so insignificant through the rest of the world’s indirect demand). So far, Canada and the EU have made considerable contributions to merchandise exports. The EU slowdown should be more of a concern in terms of directly affecting U.S. merchandise exports.

October 2022 International Monetary Fund world economic outlook Canada is expected to be 2.2% in 2022, 1.3% in 2023, Mexico 2.4%, 1.2%, Euro 1%, 1.4% area (non-EU), China at 4.3% and 2.6%.

{kind=link}

{kind=link}