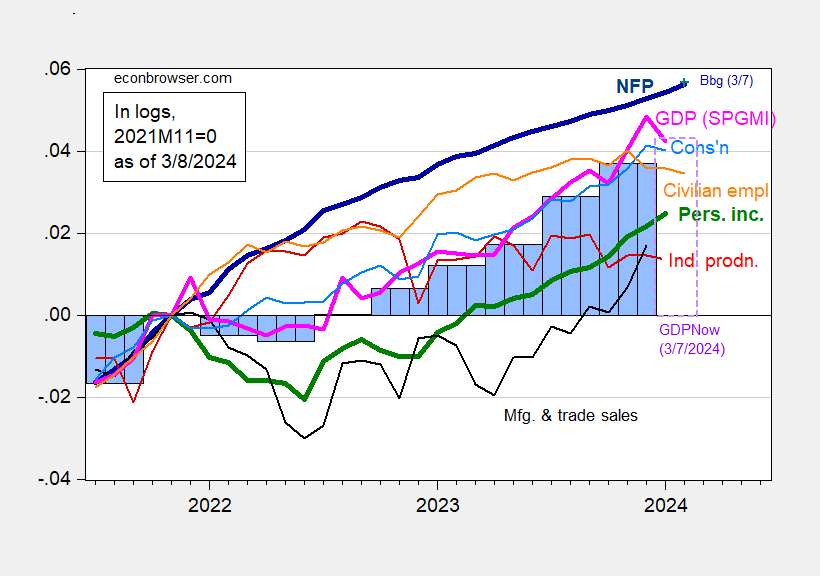

NFP employment growth unexpectedly rose to +275 in January compared to the consensus of +198,000. The total for the first two months was revised downward to 168,000, with employment levels broadly in line with the implicit consensus. Here's a picture of the key indicators followed by the NBER Business Cycle Determination Committee, along with monthly GDP and GDPNow.

figure 1: Nonfarm payrolls including baseline revisions (bold dark blue), using implied levels of Bloomberg consensus as of February 1 and December 2023 NFP (blue+), civilian employment (orange), industrial Production (red), Personal Income excluding current transfers from China in 2017$ (bold green), Manufacturing and Trade Sales in 2017$ (black), Consumption$ in 2017 (light blue), and Monthly GDP $ (pink), GDP, third release (blue bar), Q1 2024 GDPNow as of 3/7 (lilac box), all log normalized to 2021M11=0. Data source: U.S. Bureau of Labor Statistics (BLS) through FRED, Federal Reserve, BEA 2023 Q4 2nd Edition, S&P Global Market Insights (Nigerian macroeconomic consultant, IHS Markit) (3/1/Released in 2024) and the author's calculations.

While the official non-farm payrolls data series points to continued growth, alternative indicators point to slower growth.

figure 2: Nonfarm payrolls released in February (bold red), the implied level of the author’s preliminary benchmark and the change in the Bloomberg consensus in February (light red+), Philadelphia Fed early benchmark (light green), based on nonfarm payrolls Data Concept Adjusted Civilian Employment Household Survey Series (pink), QCEW covers total U.S. employment (yellow-green), seasonally adjusted using X-13 (log). Source: BLS via FRED, Bureau of Labor StatisticsPhiladelphia Fed.

The civilian employment series (from the household survey) adjusted for non-agricultural employment data shows a clear decline (partly reflecting the civilian employment situation in Figure 1). How believable is this series? I would say less than at CES.

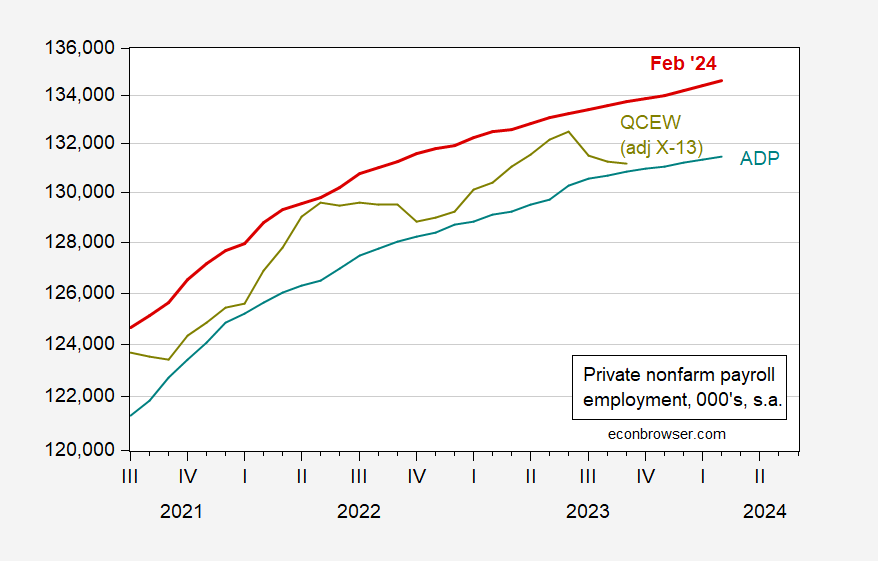

I say this because of the trend of independent series (including the ADP series) and to a lesser extent QCEW covering private sector employment.

Figure 4: BLS Private Nonfarm Employment (red), ADP (cyan), and QCEW (yellow-green). Sources: BLS, ADP (via FRED), BLS, and author's calculations.

It's hard to see a slowdown in labor market data (give appropriate weight to CES vs. CPS).Statistically, there has not yet been a recession Sam's Rules.

{kind=link}

{kind=link}