Last week, as the federal government was about to release its annual financial statement (aka “the budget”, although we don't use that term here, did we?) next Tuesday, state governments were also gradually releasing their own budget statements (them we Witnessing the absurdity of a public finance system that pretends the federal government is one big family and that monetary policy is somehow the most effective way to deal with inflation stemming from supply-side constraints, the Victorian government earlier this week. Made a pretty shocking fiscal announcement, cutting spending plans in many key areas such as health care (despite the pandemic still killing many people), public education, basic public infrastructure maintenance and upgrades, etc. Why? It amassed a sizable debt in the early years of the pandemic and is now in political danger as other state and territory governments pursue similar austerity agendas as conservatives who claim the government is headed for bankruptcy are weaponizing the national debt. While Victoria is leading the way as it provides more pandemic support to offset the damage caused by widespread restrictions, the federal government has boasted that as unemployment rises, hours are reduced and the planet needs massive investment to slow down. Climate change, it's heading towards a second consecutive surplus when we realize that about 85% of all state and federal debt issued between March 2020 and July 2022 was funded by the Reserve Bank of Australia, which is actually the federal government. itself), this madness is even more serious when citizens, if they truly understood the implications, would never agree to the drastic cuts in public spending and user pay tax increases etc. that have been justified by calls for increased debt. .This is just crazy.

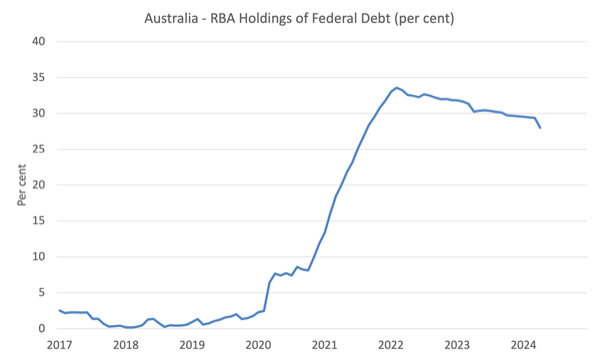

The chart below shows the total amount of federal government debt held by the Reserve Bank of Australia from January 2017 to April 2024.

At its peak (July 2022), the Reserve Bank of Australia held 32.69% of total outstanding federal debt.

As of April 2024, its proportion is 28%.

In the early years of the pandemic, the RBA bought most of the federal and state/territory debt issued.

In effect, the federal government, while purchasing its own debt, also absorbs debt issued by the next level of government.

Think about what this means.

The RBA simply plugs numbers into a bank account and owns the debt instruments it purchases in the secondary bond market (after the government issues debt in the primary market).

At the federal level, it's just a left and right pocket kind of deal.

The right pocket issues debt and pays the proceeds to the left pocket.

The left pocket then returns the proceeds to the right pocket (in the form of dividend payments from the RBA to the Treasury).

A riddle.

In the case of state/territory governments, these arrangements result in significant transfers of funds from state to federal governments.

Why?

The Reserve Bank of Australia purchases state government debt.

States and territories must repay their debt through yield-to-maturity and principal payments to the RBA.

The RBA then incorporates these payments into dividends paid to the Treasury.

States and territories have come under media pressure to cut basic spending plans due to outstanding debt, but there have been no media reports pointing to the RBA's large debt holdings.

Sky News' headlines yesterday were 'Dead to Die': Sky News presenter slams Victoria's debt' and launched a commentator as an 'expert' who simply lied to the public.

This was followed by the release of the video content “Victoria's debt comes from Labour's 'decade of disastrously bad' economic management”

The right-wing Melbourne Sun ran the headline: “The horrific debt cycle”.

A major TV station has aired reports of “major projects being scrapped in brutal Victoria budget”.

As such, the media promoted some imaginary sense of disaster and called for tougher fiscal cuts than those actually announced by the Victorian Labor government.

The reality is that Victoria's conservative opposition is a complete ragtag bunch – dysfunctional, incompetent and with no merit whatsoever to suggest they are ready to rule the state at the next election.

Yet all the talk of “debt” has sent their poll ratings soaring.

No need to wonder if they were actually elected.

Take your time.

Imagine if someone in the RBA office accidentally entered some zeros into the accounting system for the Commonwealth and state and territory government debt held by the RBA.

In other words, it has just wiped out the huge amount of money held by the RBA.

Nearly a third of federal government debt will disappear, and a significant portion of half-and-a-half (state and territory) debt will disappear.

Can the media still claim a major fiscal crisis at all levels of government?

Their graphs, which carefully manipulate vertical scale to show soaring government debt, are unlikely to look like Mount Everest.

Their sensational headlines look pretty silly.

Ask yourself if your world would be different the day after Reserve Bank of Australia officials enter zero.

No one will see any difference.

Yet when governments start cutting back on basic spending plans, including delaying investments in mitigating climate risks and improving failing hospital systems (as I noted on Monday), our world does change significantly — for the worse.

However, this could all be avoided if the RBA wiped out the debt.

Such actions will not have any negative consequences.

It would be crazy if they pretended otherwise.

But the madness doesn't stop there.

On Tuesday, the Reserve Bank of Australia decided to keep interest rates unchanged, but the governor, as usual, threatened drastic action in front of the media.

This comes against a backdrop of continued decline in inflation with no threat of acceleration.

Why has inflation fallen so quickly since September 2022?

Because the factors causing inflationary pressure have subsided – pandemic restrictions and disease, Putin, OPEC+.

The RBA has raised interest rates 11 times since May 2022, which were unnecessary and resulted in a massive redistribution of income from poorer mortgage holders to richer financial asset holders.

That alone is disgraceful.

But as Modern Monetary Theory (MMT) economists point out, rising interest rates have actually begun to drive inflationary pressures.

In Australia, the performance of the rental component of the Consumer Price Index is an example of the RBA effect, which is currently causing headline inflation to fall more slowly than when other fundamentals are taken into account.

Rising interest rates increases the burden on landlords who take advantage of lax regulations in the rental market to defraud tenants.

Just compare Japan to here.

In Japan, despite facing the same supply constraints as any country, inflation is now much lower.

The Bank of Japan did not raise interest rates during the surge in inflation.

It tells us something.

In addition, the federal government will release a fiscal statement next week.

Another fiscal surplus is expected due to a huge increase in tax revenue due to so-called tax bracket climbing.

In other words, the federal government is ruthlessly squeezing wage and salary earners and pretending that surpluses are the result of responsible fiscal management.

Over the past few days, mainstream economists, who regularly speak out in the national media, have been calling on the federal government to cut spending and increase taxes to drive a larger surplus.

Obviously, this is to help the RBA fight inflation.

However, all economic data shows that the economy is on the verge of recession.

Below is a chart of monthly working hours through March 2024.

It doesn't look healthy and we are now observing unemployment starting to rise.

Of course, the RBA wants unemployment to rise as long as no senior official joins the dole queue.

This is because they claim that the NAIRU (the unemployment rate that should be associated with stable inflation) is higher than the current unemployment rate.

But I have pointed out before that their logic is absurd.

There are glaring inconsistencies in the RBA's narrative, particularly in speeches made by the new governor before and after he took office, which justified the rate hike based on NAIRU's estimate of the Reserve Bank of Australia, which stood at 4.5% in June last year. Then it mysteriously dropped to 4.25% recently.

One of the problems with the New Keynesian approach is its insistence that the so-called non-accelerating inflation rate of unemployment (NAIRU) should guide monetary policy.

Mainstream textbook rubbish says that if the unemployment rate is below the NAIRU, then inflation will accelerate, and if the unemployment rate is above the NAIRU, the inflation will fall.

The RBA is currently claiming they must raise interest rates because the unemployment rate of around 3.7% to 3.9% is lower than NAIRU estimates.

I note that NAIRU is unobservable but is estimated through econometric methods and uses sampling errors that yield wide confidence intervals – making this concept impossible to use for accurate policy making.

But these characters still exist.

Judging from the situation in Australia over the past two years, the situation is very obvious.

The unemployment rate has been very stable over the past few years, fluctuating within a narrow range, but the inflation rate has been declining since September 2022.

This means that logically, NAIRU cannot be higher than the current unemployment rate, but must be lower than the current unemployment rate.

This means the RBA's insistence on adding 140,000 extra workers to the unemployment scrap heap is unfounded even within the theoretical framework they believe in.

Retail sales, corporate bankruptcies and other data — all of which tell us about the state of the economic cycle — all look bad.

in conclusion

It would be foolish to run a fiscal surplus at a time when inflation is steadily declining and the economy is headed for recession.

But that's where we are now.

I'm sure enlightened beings from other planets are looking down on this chaos and thinking how stupid we are for tolerating such idiocy.

My new book is now available for pre-order

A new book I co-authored with Warren Mosler is in the final stages of completion.

The book is titled: Modern Monetary Theory: The Excellent Adventures of Bill and Warren.

The content description is:

In this book, William Mitchell and Warren Mosler, original proponents of Modern Monetary Theory (MMT), discuss their views on how MMT has evolved over the past 30 years.

In a delightful, entertaining, and informative way, Bill and Warren recall how they came together from very different backgrounds to develop Modern Monetary Theory. They consider the history and personality of the MMT community, including anecdotal discussions of various scholars engaged in MMT and those who have strayed from MMT's core logic.

This is a much needed book that provides readers with a basic understanding of the original logic behind the MMT Money Story, including the role of mandatory taxation, the origins of unemployment, the origins of the price level, and the need for job security As the essence of a progressive society—the essence of Bill and Warren’s brilliant adventure.

The introduction is written by British scholar Phil Armstrong.

You can find out more about this book from the publisher’s page – here.

The book will be published on 15 July 2024, but you can pre-order a copy by emailing: info@lolabooks.eu

The special pre-order price is €14.00 (incl. VAT).

That's enough for today!

(c) Copyright 2024 William Mitchell. all rights reserved.

{kind=link}

{kind=link}