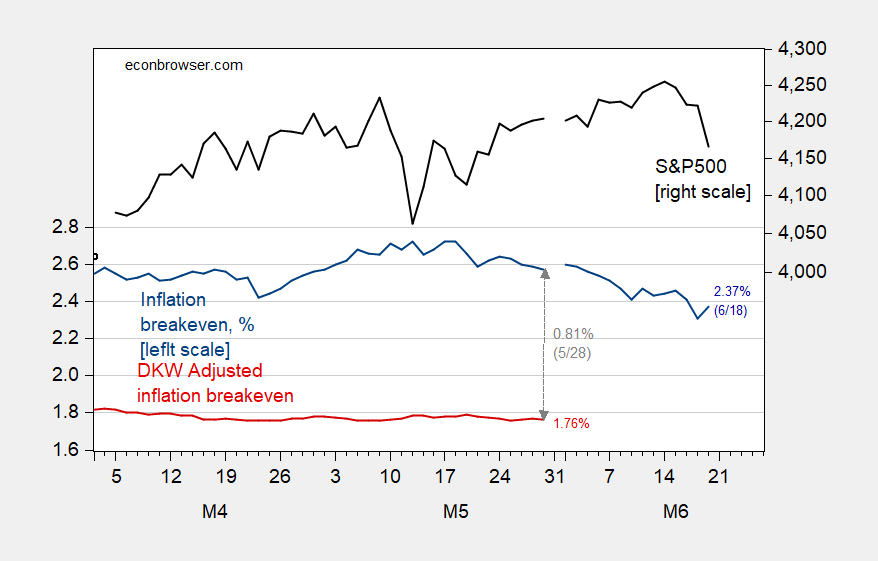

The Standard & Poor’s 500 Index fell 1.3% on Friday; many accounts attributed the decline to the Federal Reserve’s statement that the pace of interest Brad’s comment), probably in response to higher inflation prospects than previously expected. Interestingly, Friday’s market indicators do not support this interpretation.

figure 1: The five-year inflation break-even point is calculated as the five-year treasury bond yield minus the five-year TIPS yield (blue, left scale). The five-year break-even point is based on the inflation risk premium per DKW and the liquidity premium (red , Left scale) for adjustment, all in %; and S&P 500 index (black, right logarithmic scale). Source: FRB followed D’amico, Kim and Wei (DKW) through FRED, Ministry of Finance, KWW to interview 6/4, and the author’s calculations.

From 6/15 to 6/18, the five-year breakeven has dropped from 2.46% to 2.37%. However, we know that changes in the inflation risk premium and TIPS liquidity premium will lead to the calculation error of the expected inflation calculated by the simple breakeven.

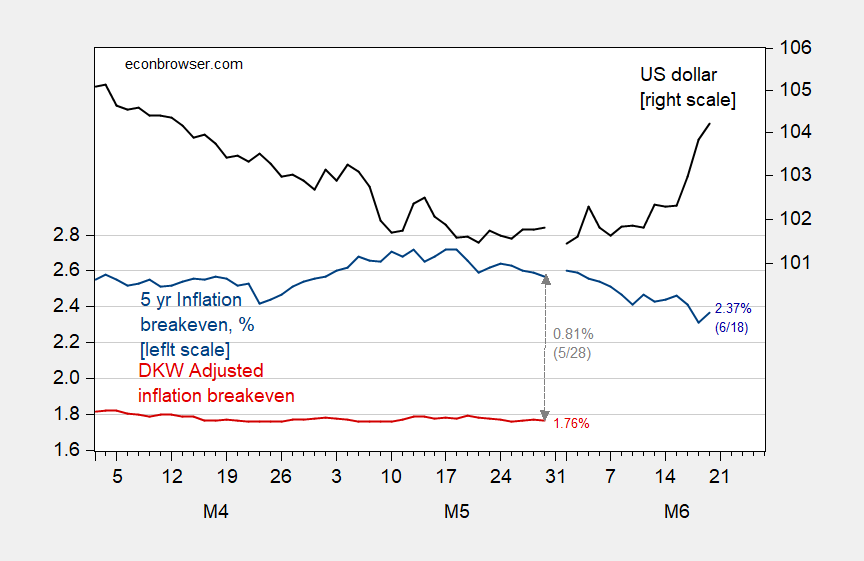

Interestingly, the appreciation of the U.S. dollar indicates that the foreign exchange market takes monetary tightening seriously (regardless of inflation expectations) and raises real interest rates (five-year TIPS rose from -1.67% to -1.48%, from 6/15 to 6/18).

figure 2: The five-year inflation break-even point is calculated as the five-year treasury bond yield minus the five-year TIPS yield (blue, left scale). The five-year break-even point is based on the inflation risk premium per DKW and the liquidity premium (red , The scale on the left) is adjusted in %; the nominal value of the Fed’s dollar index to the currencies of developed economies, 2006M01=100 (black, logarithmic scale on the right); spliced to the DXY index 6/11-6/18. Source: FRB followed D’amico, Kim and Wei (DKW) through FRED, Ministry of Finance, KWW to interview 6/4, and the author’s calculations.

Therefore, the news does not appear to be a sign of rising inflation (It seems that the impact on the previous CPI version is relatively small), but FOMC members tend to raise interest rates earlier than postpone them (the market may also think that the Fed has internal information about inflation).

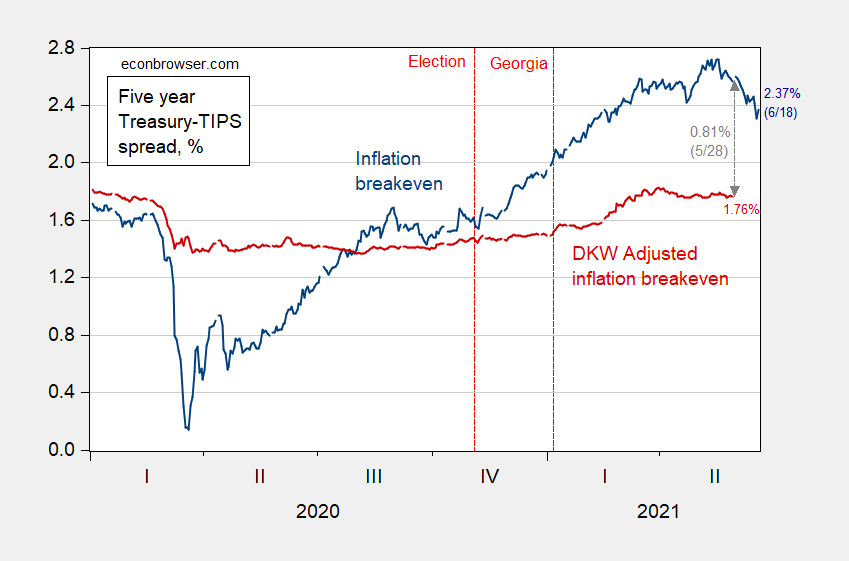

Just to consider the current inflation expectations, adjust the estimated inflation risk and liquidity premium, here is a replay of the data after 2019.

image 3: The five-year inflation break-even point is calculated as the five-year treasury bond yield minus the five-year TIPS yield (blue). The five-year break-even point is adjusted by the inflation risk premium and the liquidity premium per DKW, both in% unit. Source: FRB through FRED, Ministry of Finance, Kunshan After D’amico, Kim and Wei (DKW) interviewed 6/4 and the author’s calculations.

{kind=link}

{kind=link}