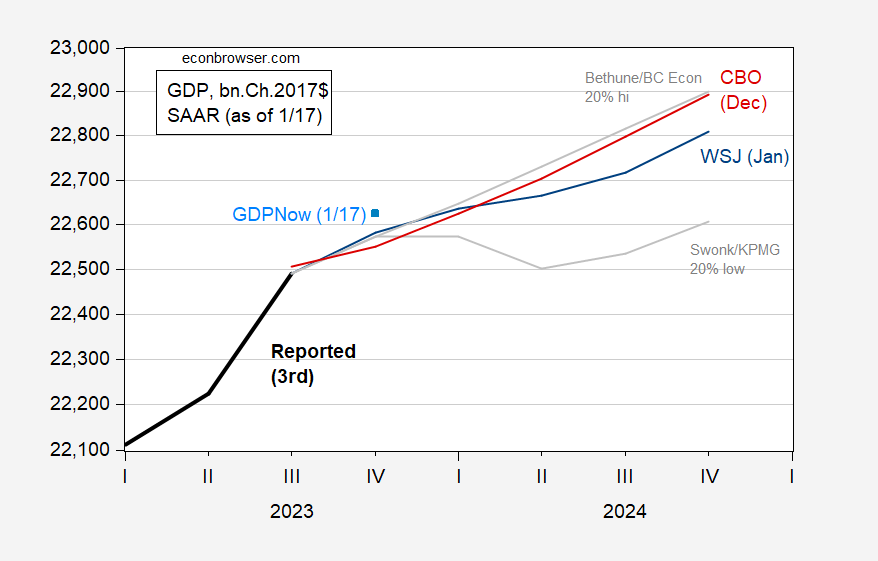

As real GDP outcomes continue to surprise upwards, the average forecast trajectory continues to rise (4Q average growth has risen from 0.9% to 1.7% since October), but forecasts are rather scattered, as shown in Figure 1.

figure 1: GDP (black), January 2024 Wall Street Journal survey average forecast GDP (blue), Bethune/Boston College Economics 20% high-end revision (Q4/2023). (grey), Swonk/KPMB downgrade (gray), CBO December forecast (red), GDPNow forecast of 1/17 (light blue square), all in billions. Ch.2017$SAAR. Sources: BEA, Wall Street Journal surveys (various), CBO, and author's calculations.

Neither the average response nor the median response showed a slowdown between the two quarters. Nonetheless, Diane Swonk's (KPMG) low 20% range entry (Q4/2024) shows 0% Q1 growth and -1.30% Q2 AR growth. About 22% of respondents expect two or more consecutive quarters of negative growth.

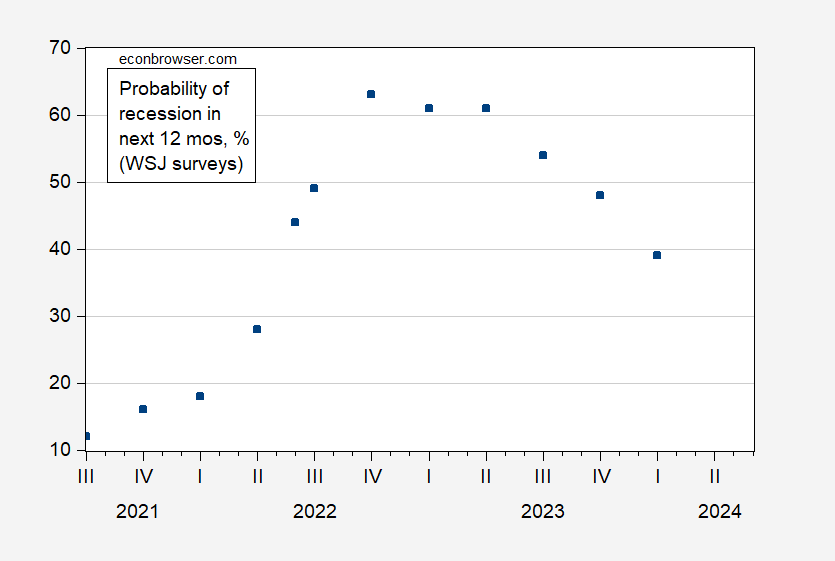

The likelihood of a recession has dropped again.

figure 2: The likelihood of a recession over the next twelve months. Source: Wall Street Journal survey, various issues.

{kind=link}

{kind=link}