Today, we are pleased to present the contribution of our guest steven cumming (AEI), former director of the Federal Reserve’s Department of International Finance. The views presented are those of the author and not necessarily those of the institution to which the author is affiliated.

In recent months, there has been a lot of discussion in the financial press about how Fed tightening can drive up the dollar and have (at least) two dangerous consequences for the global economy. First, rising U.S. interest rates and a stronger dollar are creating difficulties for emerging market economies (EMEs), who must buy dollars to service their dollar-denominated debt in cheaper local currencies. Second, those cheaper currencies in advanced and emerging market economies are driving up the cost of imports, exacerbating already strong inflationary pressures and forcing foreign central banks to tighten their own monetary policies. Both developments are said to be pushing the world into a global recession.

There is some truth to these concerns. Dollar appreciation is one of the channels through which tighter U.S. monetary policy helps cool the economy, which inevitably involves exporting a certain amount of inflation to other economies. It is also true that, historically, Fed tightening has meant bad news for emerging market economies: plunging currencies, rising credit spreads and damaging capital outflows.

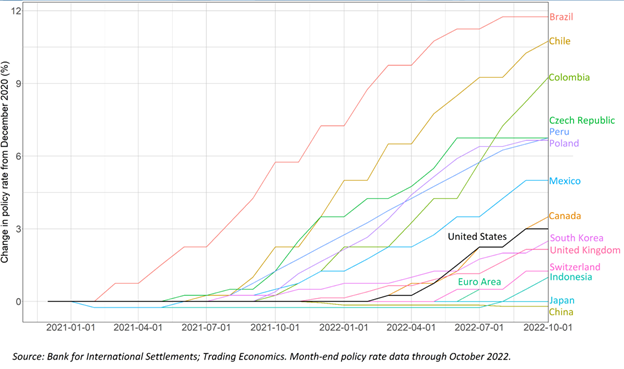

However, as I explore in a recent note, Will a Strong Dollar Trigger a Global Recession?, much of the current discussion overstates the role of Fed tightening and dollar appreciation in the dimming world economic outlook. First, contrary to the unusually aggressive Fed impression conveyed by many commentators, many central banks began tightening monetary policy before the Fed, and most of them raised rates more aggressively.

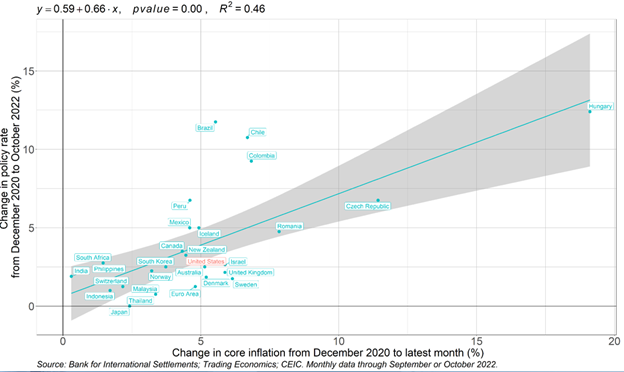

Countries with larger increases in core inflation (excluding food and energy) typically implement larger interest rate increases – the Fed’s response to inflation fits this relationship very well.

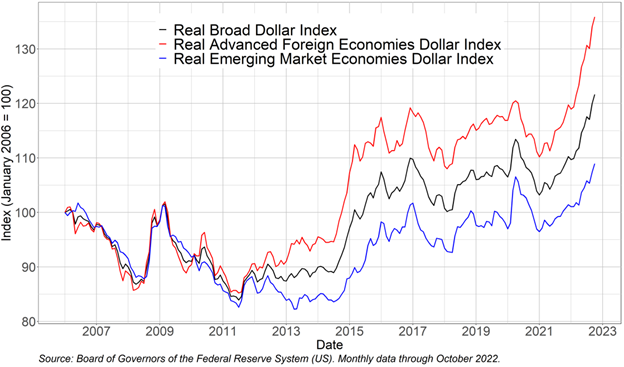

Second, a strong dollar is less of a pressure on emerging market economies than is generally believed. Most discussions on this issue focus on the value of the dollar against the currencies of advanced economies. Even after paring some of those gains over the past week, they are still up about 15% since the start of 2021, according to the Federal Reserve. In contrast, the value of the dollar against the currencies of our emerging market economy trading partners has only risen by about 8% over the same period.

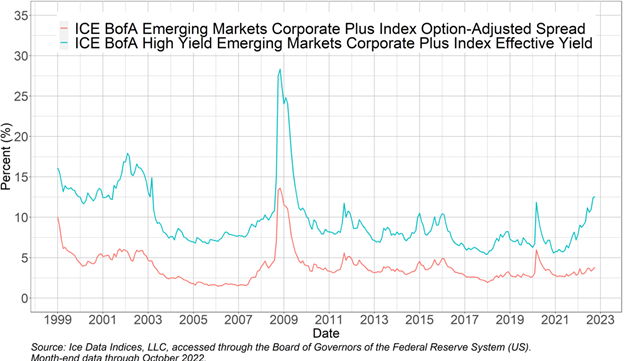

The smaller appreciation of the dollar against emerging market economies means that their debt burdens have risen less. In fact, most major emerging market economies are doing pretty well so far this year. As the chart below shows, credit spreads on dollar debt owed by emerging market economies relative to U.S. Treasuries widened on average, but remained generally within historical ranges, a good indicator of market assessments of their creditworthiness. To be sure, particularly vulnerable economies such as Sri Lanka, Pakistan and Argentina have seen higher high-yield spreads rise, but this largely reflects their own fundamental imbalances that are unlikely to push the global The economy slipped into recession.

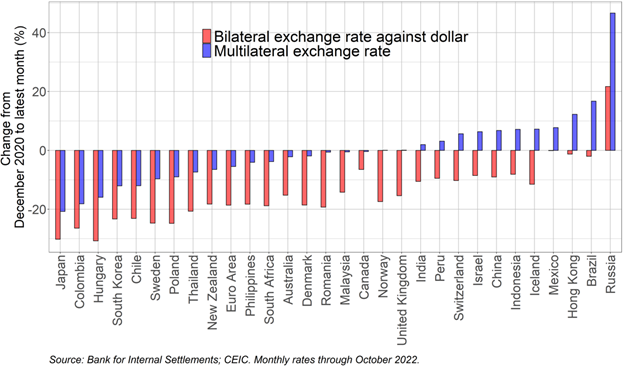

Finally, the role of a strong dollar in driving inflation abroad has been overstated. With almost all currencies falling against the dollar, each foreign economy’s “multilateral exchange rate”—that is, its average exchange rate against all trading partners—falls much less (or even rises) than its “bilateral” exchange rate against the dollar. )Dollar. As a result, import costs and consumer prices in foreign economies increase less than would be implied by the depreciation of their currencies against the dollar. (In addition to imports from the United States, commodities such as oil are also priced in dollars, but their prices generally fall as the dollar rises.) That means foreign central banks have to tighten monetary policy.

All in all, dollar appreciation poses challenges to the global economy, but these challenges should not be overstated. A narrow focus on a strong dollar ignores the more important forces driving the world economy toward recession: rising energy and food costs; Russia’s invasion of Ukraine causing energy shortages, especially in Europe; soaring inflation prompting central banks around the world to tighten monetary policy; Growth’s zero-COVID policy; the legacy of the COVID-19 pandemic is economic scarring and debt accumulation.

This article was sponsored by steven cumming.

{kind=link}

{kind=link}