Today, we are fortunate to present to you an article by natasha che, Alexander Kopestak and david fussery (all at the IMF) and Tamaro Terraciano (IESE Business School, Barcelona). The views expressed in this article are those of the authors and not necessarily those of the institution to which they are affiliated.

Cryptoassets vary widely in design and value proposition—from hedging against inflation to providing more efficient payments, censorship-resistant computing, or property rights—yet their prices fluctuate according to a common cycle. The index return period has attracted retail and institutional investors, while the ensuing crash has drawn increasing attention from politicians and regulators. Volatility in the cryptocurrency market may also become increasingly in sync with other asset classes: Bitcoin provided a partial hedge against market risk until 2020, but since then it has become increasingly correlated with the S&P 500 (Adrian, Iyer and Qureshi, 2022).

in a new article, we illuminate the drivers of cryptoasset prices by answering the following questions. To what extent do cryptoassets have common cycles? Is the cryptocurrency market becoming more in sync with the global stock market? If so, why? Given that U.S. monetary policy has been identified as a key driver of global financial cycles (Miranda-Agrippino and Rey, 2020), will U.S. monetary policy affect cryptocurrency cycles to a similar extent? If yes, through which channels?

We first use a dynamic factor model to identify a single dominant trend in crypto asset prices. Using daily price panels for several of the longest-lived coins (which collectively account for about 75% of the total cryptocurrency market capitalization), we break down their changes into asset-specific idiosyncratic distractions and common components. We found that the resulting “encryption factor” explained approximately 80% of the variance in encrypted price data.

We then examine the relationship of this crypto factor to a set of global equity factors constructed using stock indices of the countries with the largest GDP (in the spirit of Rey, 2013; Miranda-Agrippino and Rey, 2020). We find positive correlations across the sample, driven by particularly strong correlations from 2020. The growing correlation is not limited to Bitcoin versus the S&P 500, but involves cryptocurrencies and global equity factors more broadly. By disaggregating the equity markets, we find that since 2020, the cryptocurrency factor has the strongest correlation with the global technology factor and the small cap factor, while interestingly, it has a lower correlation with the global financial factor.

The strengthening correlation between cryptocurrencies and stocks is consistent with the growth of institutional investor participation in the cryptocurrency market since 2020. Although institutions have smaller exposures relative to their balance sheets, their absolute trading volumes are much larger than retail traders. In particular, trading volumes by institutional investors on cryptocurrency exchanges increased by more than 1700% (from roughly $25 billion to over $450 billion) from Q2 2020 to Q2 2021 (Auer et al. 2022). As institutional investors trade both equities and crypto assets, this leads to a gradual increase in the correlation between marginal equity and the risk profile of crypto investors, which in turn correlates with a higher correlation between global equities and crypto factors. When decomposing the factor changes following Bekaert, Hoerova, and Lo Duca (2013), we find that the correlation between the overall effective risk aversion of cryptocurrencies and stocks can explain a large part of the correlation between these two factors (up to 65% ).

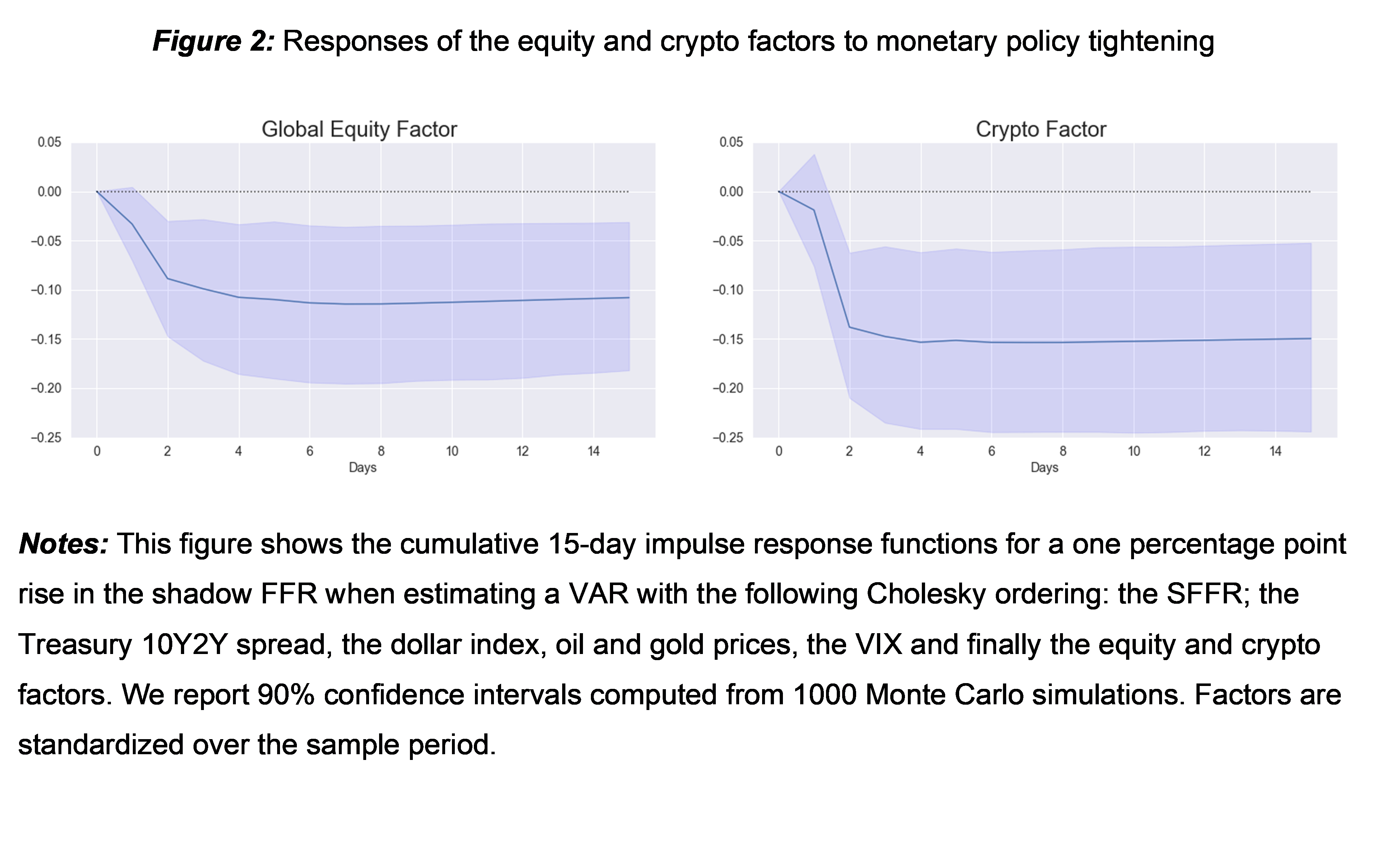

As monetary policy in the United States affects the global financial cycle (Miranda-Agrippino and Rey, 2020), the high correlation between stocks and cryptocurrencies suggests a similar impact on cryptocurrency markets. We test this hypothesis using daily VAR and Wu and Xia’s (2016) shadow federal funds rate (SFFR) to explain the important role of balance sheet policy in our sample period. We find that U.S. monetary policy affects the cryptocurrency cycle in the same way it affects the global stock market cycle, which is in stark contrast to the claim that crypto assets can be a hedge against market risk. A 1 percentage point increase in SFFR leads to a sustained 0.15 standard deviation drop in the crypto factor and a 0.1 standard deviation drop in the equity factor over the next two weeks.

We find evidence that the risk-taking channel of monetary policy is an important channel driving these results, similar to the findings of Miranda-Agrippino and Rey (2020) for global equity markets. Monetary tightening led to a decrease in the cryptocurrency factor, while the overall effective risk aversion indicator of the cryptocurrency market surged. When splitting the 2020 sample, we find that the effect on cryptocurrency market risk aversion is only significant in the post-2020 period, which is consistent with the entry of institutional investors strengthening the transmission of monetary policy to the cryptocurrency market .

We rationalize our results in a model with two heterogeneous agents, namely cryptocurrency investors and institutional investors. The higher the relative wealth of institutional investors, the more similar the overall effective risk aversion of cryptocurrencies is to their risk appetite, and the higher the correlation between cryptocurrencies and the stock market. Even in our simple framework, spillovers from cryptocurrencies to stocks can emerge: If institutional holdings of cryptocurrencies become larger, a collapse in cryptocurrency prices reduces the equilibrium return to stocks.

Overall, our results highlight that, despite a variety of interpretations for cryptoasset values, most changes in cryptomarkets are highly correlated with stock prices and highly influenced by Federal Reserve policy. Growth in institutional participation reinforces these conclusions and increases the risk of spillovers from the cryptocurrency market into the broader economy.

refer to

Adrian, Tobias, Tara Iyer, and Mahvash S. Qureshi, 2022, Taking stock: the transmission of monetary policy to stock markets, IMF Blog.

Auer, Raphael, Marc Farag, Ulf Lewrick, Lovrenc Orazem, and Markus Zoss, 2022, Banking in Bitcoin’s Shadow? institutional adoption of cryptocurrencies, Bank for International Settlements working paper.

Bekaert, Geert, Marie Hoerova and Marco Lo Duca, 2013, Risk, Uncertainty and Monetary Policy, Journal of Monetary Economics.

Miranda-Agrippino, Silvia, and Helene Rey, 2020, U.S. Monetary Policy and the Global Financial Cycle, Review of Economic Studies.

Rey, Helene, 2013, Dilemmas not Triangles: Global Financial Cycles and Monetary Policy Independence, Jackson Hole Conference Proceedings.

Wu, Jin Cynthia, and Fan Dora Xia, 2016, Measuring the Macroeconomic Impact of Zero Lower Bound Monetary Policy, money, credit and banking magazine.

The author of this article is Natasha Che, Alexander Kopeestek, david fussery and Tamaro Terraciano.

{kind=link}

{kind=link}