Today, we are pleased to introduce to you by Justin-Damian Guynet (Senior Economist), Zhonglinhe (Senior Economist), M. Ayhan Kose (Chief Economist and Director) and Franziska is careless (Manager) from the World Bank Outlook Team. The findings, interpretations and conclusions expressed in this blog are solely those of the author. They do not necessarily represent the views of the World Bank, its Executive Directors or the countries they represent.

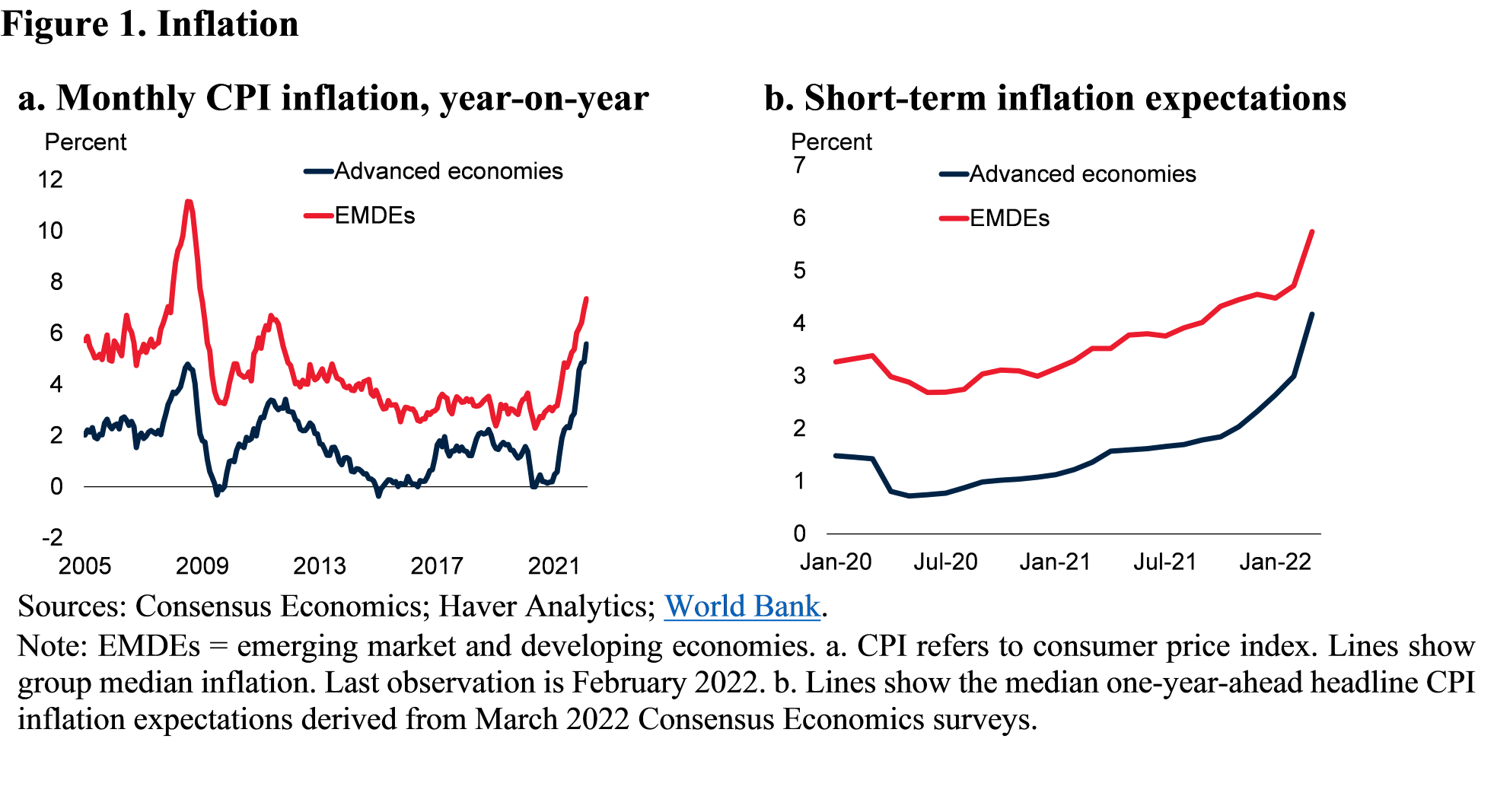

In February 2022, global inflation rose to its highest level since 2008. Year-on-year inflation in advanced economies has risen nearly 10 times over the past year. That was before the Russian invasion of Ukraine caused commodity prices to soar. High and rising inflation has prompted central banks in many emerging market and developing economies (EMDEs) to tighten monetary policy.

As the Fed’s recent decision shows, the economic fallout from the Ukraine war is unlikely to derail plans announced by central banks in some major advanced economies to tighten monetary policy to control inflation.If such policies are tightened faster than expected, it could lead to a significant price repricing Financial Market Risks in Emerging Market Economies and stifle the economic recovery. To create space for monetary policy action and anchor medium-term inflation expectations, the EMDE central bank needs to increase its credibility through, for example, transparent communication.

Inflation and Policy

After falling in the first half of 2020, inflation in advanced and emerging market economies pent-up demandpersistent supply disruption, and soaring commodity prices (Figure 1a). The rise in inflation is widespread: about nine in 10 countries experienced a rise in inflation last year. Rising inflationary pressures have pushed up near-term inflation expectations in many countries, especially in the wake of the Ukraine war (Figure 1b); in some economies, long-term inflation expectations also climbed up. In response to rising prices and steadily rising inflation expectations, many EMDE central banks have raised policy rates throughout 2021.

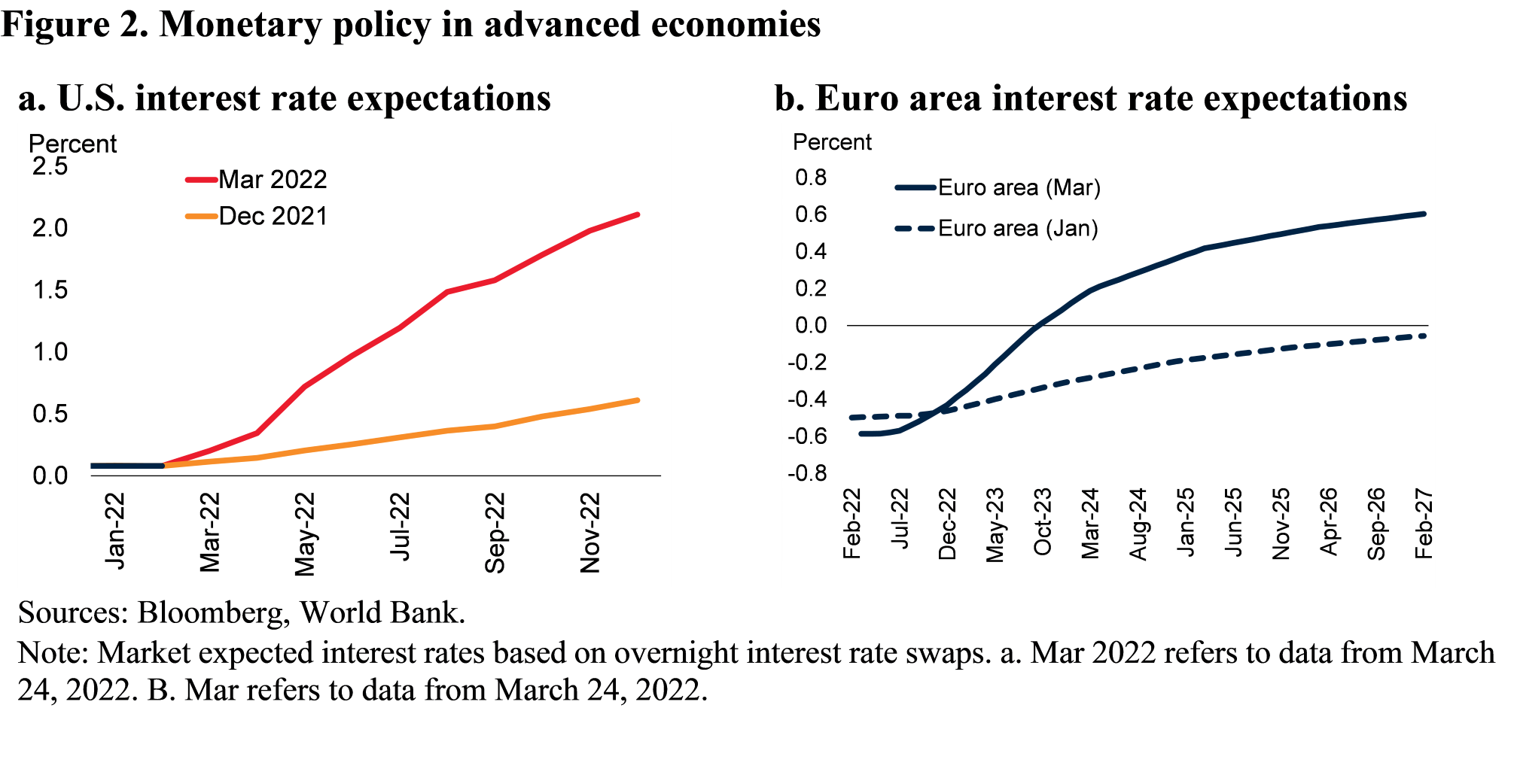

In advanced economies, central banks have so far responded gradually to rising inflationary pressures, tapering off unconventional support introduced during the pandemic and (in some cases) raising policy rates. They also expressed their intention to raise interest rates further in the coming months. On March 16, the Fed raised the federal funds rate by 25 basis points and signaled a series of rate hikes through the end of 2022 (Figure 2).

Financial markets have sharply raised expectations for the trajectories of major central bank policy rates (Figures 2a and 2b). The expected increase in policy rates has led to heightened volatility in financial markets, but has yet to trigger a material tightening of financial conditions in advanced economies.

Consequences of Faster Tightening

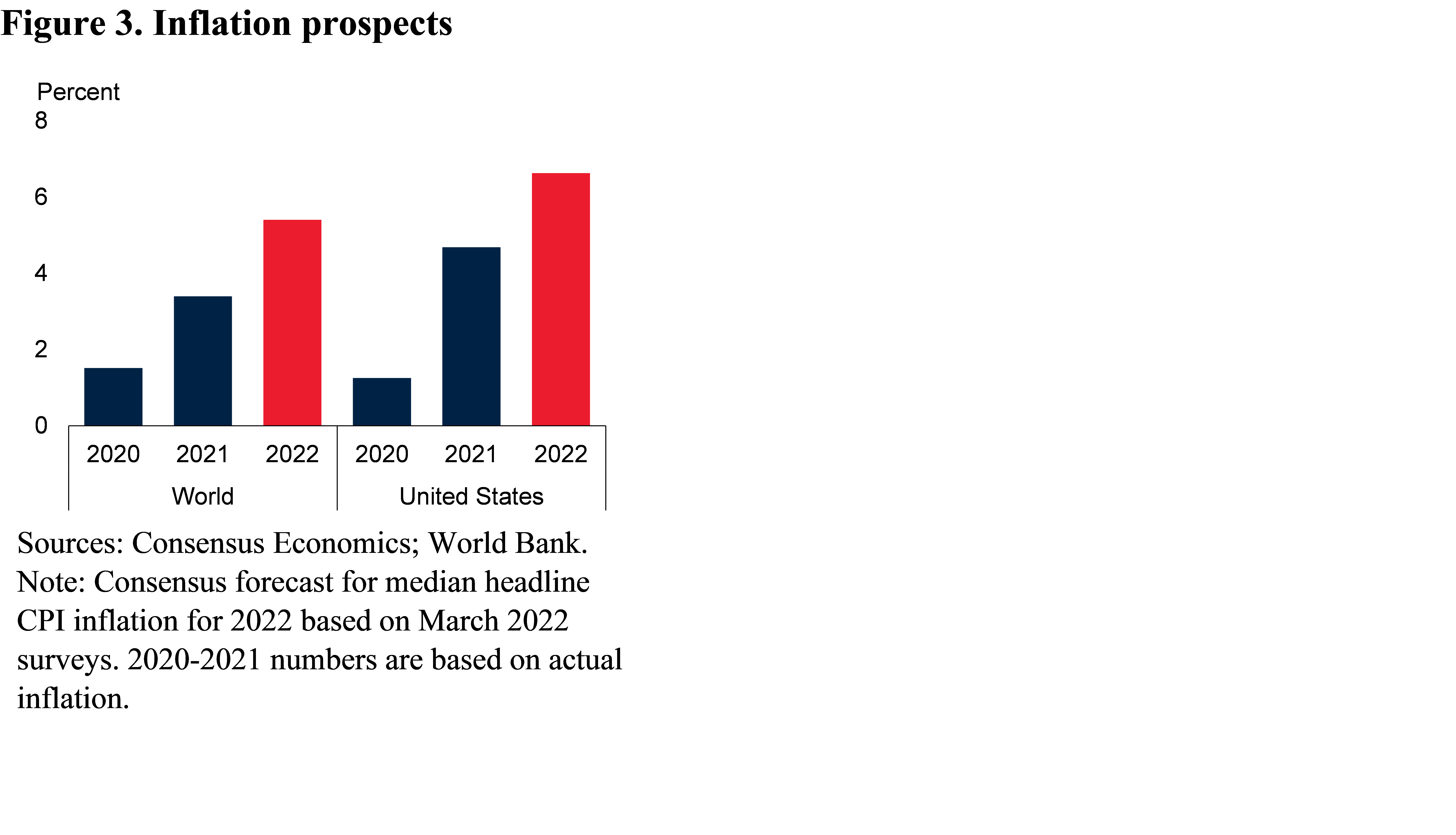

Global Consumer Price Inflation It is expected to peak later in the year and then gradually decline, supported by good expectations in most economies (Figure 3). ease inflation This is in line with expectations of slower global growth in 2022-23, judging from an exceptionally strong rebound in 2021.This global growth slowdown will be Steepest post-recession rebound Will be widely used in advanced economies and EMDEs over the past half century.

However, inflation is already above target in more than nine-tenths of advanced economies and two-thirds of emerging market economies with inflation targeting.There is also a risk that instead of abating inflationary pressures in the short term, it could lead to Inflation expectations are rising steadily. For example, if supply disruptions recur or commodity prices climb further—especially due to the war in Ukraine—global inflation could remain elevated for an extended period or even rise further, leaving many countries well above target Scope. While inflation data has yet to reflect the war in Ukraine, market-based inflation expectations have already priced in additional inflationary pressures from the conflict.

If this risk materializes, advanced-economy central banks may have no choice but to raise policy rates quickly.Rising U.S. rate expectations could lead to sharp Repricing of Risk in Financial Markets. The macroeconomic impact of a sudden tightening of global financial conditions and weakening consumer and business confidence will exacerbate the easing of global fiscal support and deepen the global slowdown.This may have intensified Macroeconomic vulnerabilities intensify A larger growth slowdown could be triggered as negative spillovers from confidence, trade and commodity price channels reduce private sector activity.

These countries will experience capital outflows due to heightened investor risk aversion, devaluing their currencies, increasing their debt burdens and driving up inflation. In 2020, foreign currency-denominated debt accounted for one-half or more of government debt in one-half of emerging market economies.Even if not denominated in foreign currencies, government and private debt remain in Decade High Makes these economies vulnerable to rising borrowing costs and rollover risks. Domestic credit spreads will widen, triggering higher default rates, especially in countries with pre-existing balance sheet vulnerabilities. Debt service costs increase With a higher rollover risk, governments in many EMDE countries, especially those with limited fiscal space, will have to reduce public spending and delay investment projects. Emerging market and developing economies are set to experience a new bout of downturn, with growth set to drop sharply this year.

Policy: Need for calibration, credibility and communication

Although EMDE policymakers have limited influence over the design of monetary policy in advanced economies, they can effectively focus on the alignment, credibility, and communication of their own policies.Specifically, mitigating the adverse effects of a tightening cycle requires caution calibration, credible formulate and clarify communication policy. This approach can greatly increase the EMDE’s resilience to sudden changes in global financial markets.

For monetary policy, adjusting policy levers to stay ahead of inflation without dampening the recovery will be key. For EMDE, Communicate monetary policy decisions Obviously, using a solid monetary framework, and maintain the independence of the central bank It will also be key to the management cycle. On the financial front, policymakers must work to rebuild reserve buffers and recalibrate prudential policy — including capital and liquidity buffers. In addition, they will need to strengthen risk monitoring and strengthen insolvency regimes.

With regard to fiscal policy, the information is largely the same. The speed and magnitude of the withdrawal of fiscal support must be precisely calibrated and closely aligned with a credible medium-term fiscal plan.In addition, policymakers need to address investor concerns Achieving Long-Term Debt Sustainability by Strengthening Fiscal Frameworksimprove debt transparency, upgrade debt management functions, and improve the revenue and expenditure sides of government balance sheets.

This article is by Justin-Damian Guynet, Zhonglinhe, M. Ayhan Kose and Franziska is careless.

{kind=link}

{kind=link}