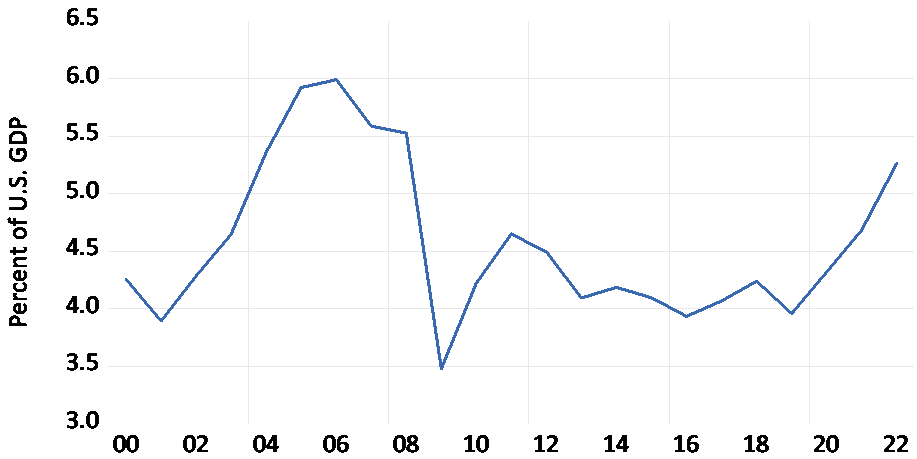

The U.S. current account deficit has grown from 2.1% of GDP in 2019 to 3.7% of GDP in 2020 and then to 4.8% of GDP in the first quarter of 2022. Bureau of Economic Analysis The increase was driven by a widening trade deficit in goods, the report said. Figure 1 depicts the US merchandise trade deficit.

figure 1. U.S. trade deficit for the period 2000-2022. resource: US Census Bureau.

The recent trade and current account deficits come against the backdrop of a large U.S. budget deficit, rising U.S. interest rates relative to its trading partners, and an appreciating dollar. In the 1980s, the United States also had large budget deficits, higher interest rates relative to its trading partners, and an appreciating dollar. In the 1980s, a strong dollar caused US export- and import-competing firms to lose price competitiveness. In 1985, the United States had a trade and current account deficit of 3 percent of GDP.

The G-5 countries (France, Germany, Japan, the United Kingdom, and the United States) are alarmed by these imbalances. To address these issues, they reached the Plaza Accord in September 1985. The U.S. agreed to reduce the budget deficit, U.S. trading partners implemented stimulus policies, the five countries worked together to lower the value of the dollar, and agreed to fight protectionism. The dollar did depreciate, and the US current account was balanced in 1991.

Estimated trade elasticity

After the Plaza Accord, exchange rate adjustments appeared to help rebalance trade. To investigate whether they would have this effect now, I estimated the elasticity of imports and exports in the United States. In previous work, Chin The dynamic ordinary least squares (DOLS) technique is used to estimate the trade elasticity of US imports and exports for the period from the first quarter of 1975 to the first quarter of 2010. In his baseline norm, he reports an exchange rate elasticity of -0.45 for commodity imports excluding oil, and an income elasticity of 2.6. For commodity exports excluding agriculture, he finds an exchange rate elasticity of 0.6 and an income elasticity of 1.9.

I use commodity import data excluding oil and commodity exports to estimate aggregate import and export elasticity US Census Bureau and US International Trade Commission. These are used from U.S. Bureau of Labor Statistics. According to the incomplete substitution model, it is assumed that imports depend on the real exchange rate and GDP of the United States, and exports depend on the real exchange rate and GDP of the rest of the world.The data for the depreciation of the real effective exchange rate by the broad consumer price index comes from Bank for International Settlements and U.S. GDP data OECD. GDP data for the rest of the world is calculated as a geometrically weighted average of the GDP of the 15 major trading partners, again from the OECD. The model is estimated using DOLS and data from the first quarter of 1994 to the fourth quarter of 2019. Also included in the model are first-difference right-hand variables, quarterly dummies, time trends, and four lags and two leads of the global financial crisis dummy.

The generated import function is:

Sample period = 1995Q2-2019Q4, adjusted R-squared = 0.991, heteroskedasticity and autocorrelation corrected standard errors in parentheses, *** indicates significance at 1% level.

In Equation (1), IM represents the US real imports excluding oil, RER represents the real effective exchange rate, and USGDP represents the US real GDP. The results show that a 10% appreciation of the dollar will increase imports by 5.0%, and a 10% increase in US GDP will increase imports by 21.0%.

The corresponding result for export is:

Sample period = 1995Q2-2019Q4, adjusted R-squared = 0.991, heteroskedasticity and autocorrelation corrected standard errors in parentheses, *** indicates significance at 1% level.

In Equation (2), EX represents the real exports of the United States, RER represents the real effective exchange rate, and ROWGDP represents the real GDP of the rest of the world. The results show that a 10% appreciation of the dollar will reduce exports by 5.2%, and a 10% increase in the rest of the world GDP will increase exports by 31.7%.

influences

The Marshall-Lerner condition states that, starting from the trade balance, if the sum of the absolute values of export and import elasticities exceeds 1, a currency devaluation will improve a country’s trade balance. The price elasticity in equations (1) and (2) satisfies exactly this condition.This suggests that a weaker dollar will help improve the trade balance

Between 2000 and 2021, the U.S. current account deficit averaged 3.4% of U.S. GDP. So far, the rest of the world has been willing to fund these U.S. deficits. If the rest of the world becomes increasingly reluctant to continue accumulating U.S. assets on this scale, the dollar will depreciate. The above results suggest that devaluation will help improve the trade balance. But the price elasticity is not large. This means that devaluation alone is not enough to rebalance trade. This will force part of the adjustment to come through a decline in US GDP. Such adjustments would be painful for American workers, consumers and businesses.

Average U.S. budget deficit 6.6% of GDP over the past 12 years. This fiscal stimulus increases U.S. gross domestic product, which in turn increases the U.S. current account deficit. The US budget deficit that caused panic in 1985 was less than 5% of GDP. As a result, the U.S. budget and current account deficits that led to the Plaza Accord’s urgent action are now being exceeded year after year. To help reduce the current account deficit and help fight inflation, the United States should reduce its budget deficit.

This article is by William Sobeck.

{kind=link}

{kind=link}