Ten-Year Treasury Bond and Federal Funds:

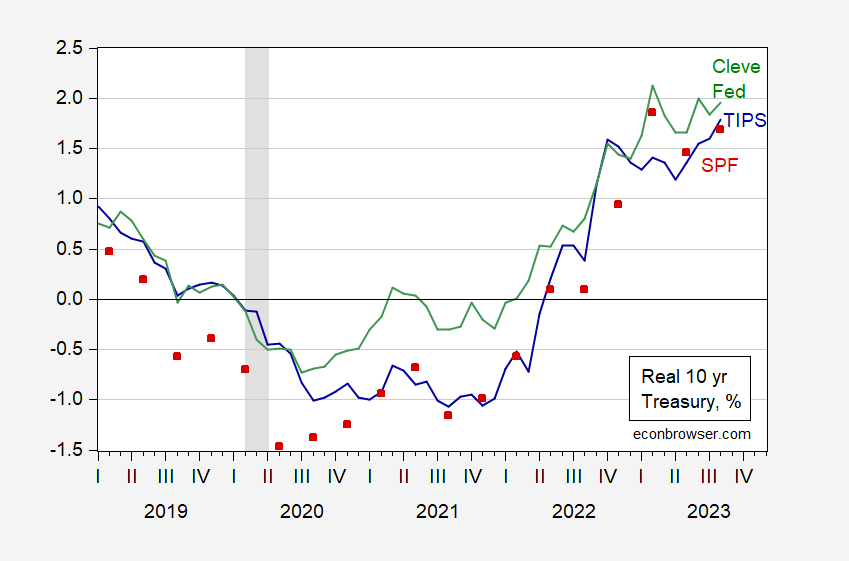

figure 1: The 10-year Treasury fixed yield is adjusted for the median survey of professional forecasters (red squares), the Cleveland Fed’s 10-year expected inflation rate (green), and the TIPS 10-year fixed yield to maturity, all expressed in %. NBER-defined recession peak-to-trough dates are in gray. Source: Federal Reserve, Treasury (via FRED), Philadelphia Fed, Cleveland Fed, NBER, and author’s calculations.

In real terms, interest rates rose rapidly from their trough. TIPS 10-year rose by 2.8 percentage points, the 10-year SPF rose by 3.06 percentage points after adjustment, and the 10-year Cleveland Fed forecast rose by 2.7 percentage points after adjustment.

figure 2: The federal funds rate, adjusted for one-year expected inflation, based on the Michigan Survey (blue), the New York Fed (tan), and the Cleveland Fed (green), all expressed in %. NBER-defined recession peak-to-trough dates are in gray. Source: Michigan Federal Reserve, via FRED, Cleveland Fed, NBER, and author’s calculations.

Real federal funds, calculated using the Michigan survey, have risen 8.1 percentage points since the trough (March 2022). Mixed information indicators such as the Cleveland Fed’s inflation expectations showed a smaller increase, but still a substantial increase of 5.7%.

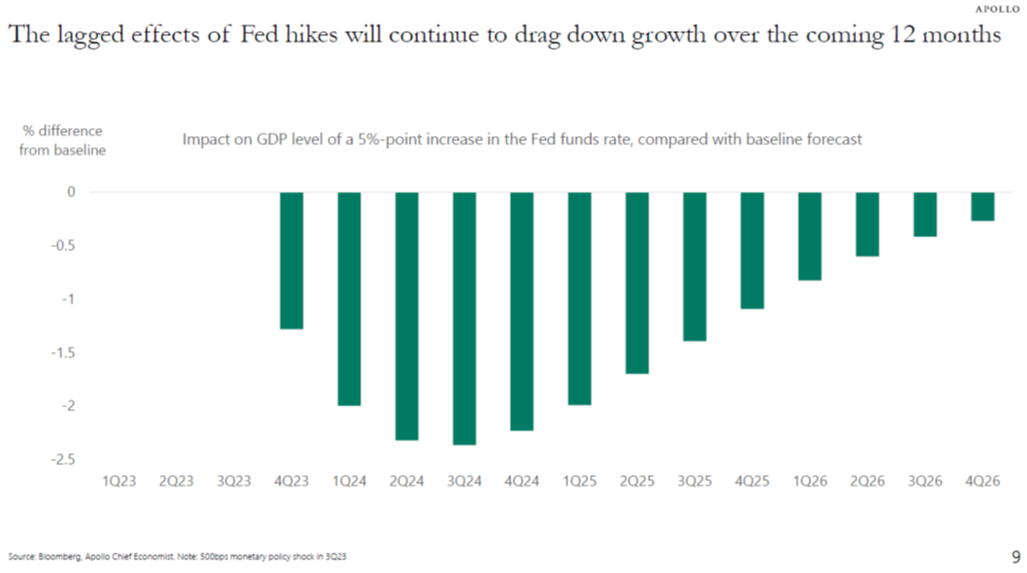

Torsten Slok estimates the impact on economic growth of a 500 basis point increase in the federal funds rate in the third quarter of 2023 (deviation from the baseline).

source: Slok, Public and Private Market Outlook, September 2023 (Apollo).

There are two complications: the estimate is for a 500 basis point shock, and I have shortened the actual rate change. Real interest rate changes occur starting in the second quarter of 2022.

To me, this means that even if the Fed stops raising rates now, our economy will take a considerable drag.

{kind=link}

{kind=link}