Some of them-but some signs indicate that it is not the majority.

Let’s define the trade balance in NIPA terms, so we look at “net exports”, in this case normalized by GDP.

Where predecessor Is an export, I’m It is imported.

Assume that U.S. exports depend on foreign economic activities and imports depend on U.S. economic activities. This assumes that imports cannot replace exports to a large extent, and exports cannot well substitute domestic commodities.

![]()

![]()

Where Yes Is GDP, q It is the trade-weighted real exchange rate, which is defined as the actual U.S. dollar/actual foreign currency unit.

The norm implicitly assumes that the supply elasticity of exports and imports is perfect.This seems counterintuitive, but I have not found evidence of time series effects (see this Paper).Therefore, in my research, I focus on the changes in the above specifications [1], [2].

Take the total differential:

![]()

Since Kopits’ focus is on non-oil commodity trade balances, each export and import term is defined accordingly. Then the change in the proportion of U.S. net exports of goods other than oil in U.S. GDP can be decomposed into: on the one hand, exogenous changes in the autonomous RoW demand for U.S. merchandise exports, changes related to changes in RoW GDP, and changes related to changes in the real exchange rate. , The exogenous changes in the United States’ independent demand for imports from other parts of the world, changes related to changes in US GDP, and changes related to changes in the real exchange rate.

Mr. Kopitz It is asserted that stimulus measures are the source of the worsening trade deficit and that several fiscal packages that have been passed may increase imports. However, changes in autonomous imports (as the pandemic shifts consumer preferences to goods rather than services) will certainly have an impact, and its impact may be as large as government spending and transfers that increase personal income in the United States. However, as the decomposition shows, the decline in the world’s GDP will also affect the trade balance (the same is true for changes in real exchange rates—although the trade-weighted real dollar is roughly the same as in February 2020).

I only focus on this field, but take into account the wider development Mundell-Fleming Model Will not change the conclusion.

One might argue that exports to the rest of the world are restricted by supply chain issues (or, strangely, due to unemployment per person Mr. Kopitz – So the stimulus causes people to lose their jobs and therefore cannot produce and export? ). I don’t think there are too many arguments that this is a major issue.

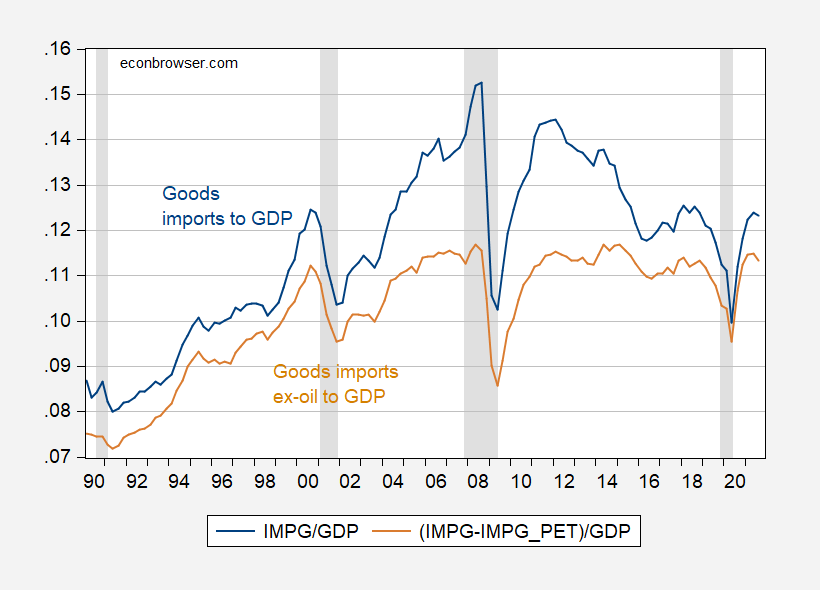

Therefore, it makes sense to look at commodity imports as measured by nominal GDP. As shown in Figure 1.

figure 1: Imports of goods and services (calculated in the balance of payments) as a share of GDP (blue line), imports of goods other than oil (brown line). The NBER decline dates are shaded gray from peak to trough. Source: BEA, NBER and author’s calculations.

Now, do all the packages starting in 2020 support consumption? However, given the public health conditions, even without these packages, we will switch to commodities. Therefore, the question is how much of the increase in merchandise imports is due to the stimulus itself, not the pandemic situation.

Facts have proved that in the past year ending in the third quarter of 2021, commodity consumption increased by 683 billion Ch12 U.S. dollars relative to the fourth quarter of 2019, while non-oil commodity imports increased by 227 billion Ch12 U.S. dollars (since the fourth quarter of 2019) Since then, the average has been 62 billion Ch12 U.S. dollars). Therefore, in the past year, approximately one-third of commodity consumption (excluding oil) was attributable to increased levels of commodity imports (excluding oil), partly due to the pandemic of various recovery plans adopted since then .

However, since exports mainly respond to the real exchange rates of economic activity and business cycle frequencies in other parts of the world, the deterioration in the trade balance (and recent recovery) cannot be entirely attributed to stimulus, especially considering the less stimulating fiscal Policies are pursued in many of our trading partner economies.

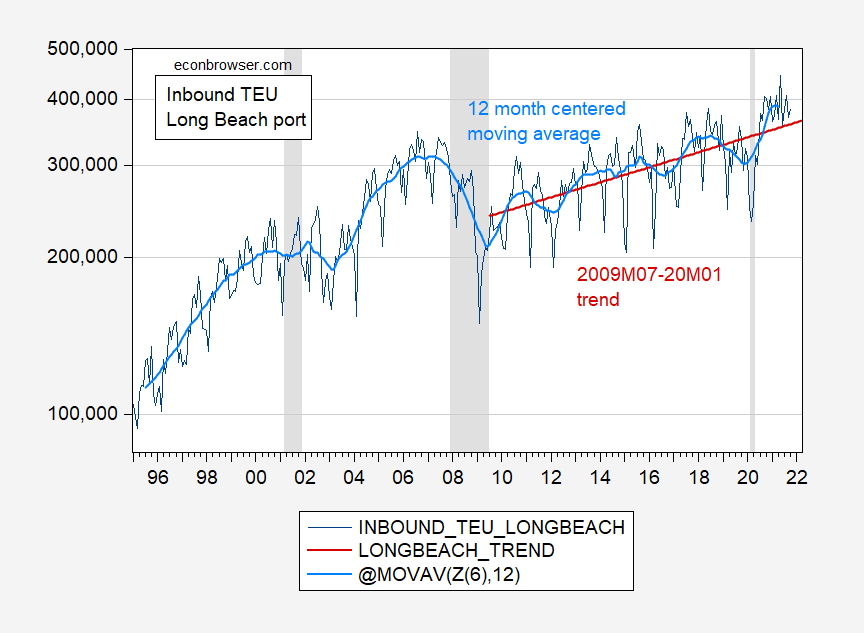

As a side, it’s interesting, for example, how far the TEU flow in Long Beach deviates from the trend, as described in this article postal, Imports are not much. But many are used for export.

figure 1: Entry TEU, Port of Long Beach (dark blue), 12-month central moving average (sky blue) and 2009M07-20M01 trend (red). NBER-defined recession date peak-trough shaded in gray. TEU = 20-foot equivalent unit. source: Port of Long Beach, NBER and author’s calculations.

Inbound traffic is above the trend, as measured by at least a 12-month moving average. This is consistent with the view that the increasing demand for goods is driving some of the logistics problems currently encountered.

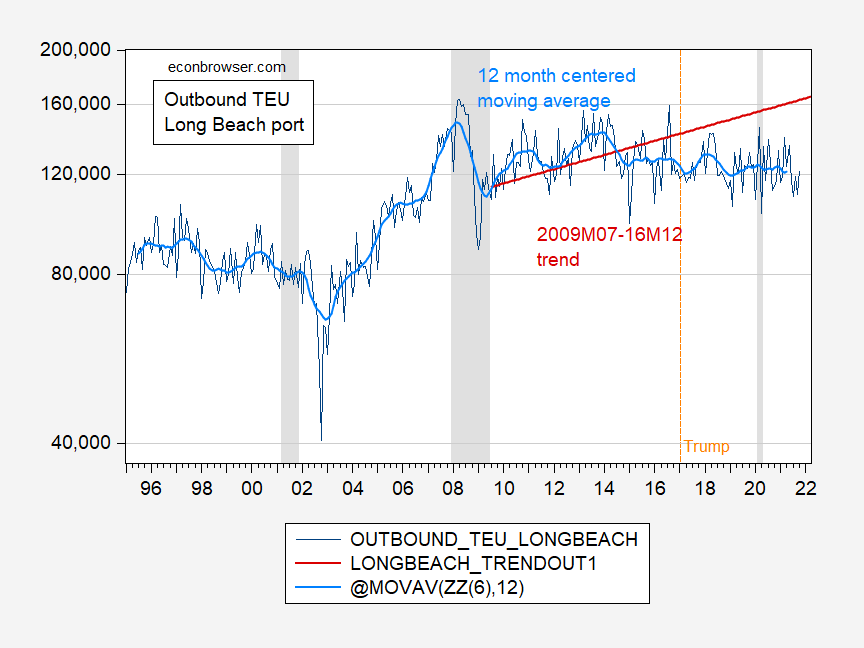

An interesting aspect of the series is that it started to decline significantly even before the pandemic hit. This, in turn, is consistent with the impact of tariffs on imports or slower growth. On the other hand, outbound traffic has been out of fashion for many years.

figure 2: Outbound TEU, Port of Long Beach (dark blue), 12-month central moving average (sky blue) and 2009M07-16M12 trend (red). NBER-defined recession date peak-trough shaded in gray. TEU = 20-foot equivalent unit. source: Port of Long Beach, NBER and author’s calculations.

{kind=link}

{kind=link}