I asked myself this question while preparing my handouts. As it turns out, things aren’t that bad between 1986 and 2022.

consider:

The variable on the left is annualized quarter-to-quarter PCE inflation, yes is logarithmic GDP, yesf is the log of full employment or potential GDP, expected inflation is the Michigan survey’s expectations one year in advance, and z is a cost driver variable consisting of the New York Fed Global Supply Chain Stress Index (GSCPI), quarter-over-quarter annualized oil price inflation, and a lock-in dummy variable (taken from March 1, 2020 to February 2021)

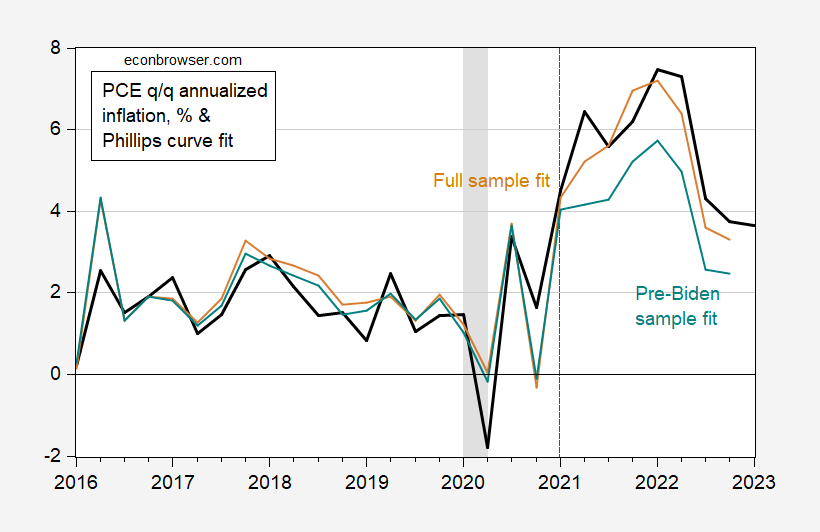

A simple regression of inflation on the output gap yields an adjusted R2 to zero. The full model estimated on the entire sample yields an adjusted R2 0.57, very good fit (tan line).

figure 1: Real quarter-over-quarter annualized PCE inflation (black), in-sample fit of the augmented Phillips curve equation estimated 1998-2022 (tan), and in-sample and out-of-sample equation fits estimated 1998-2020 (blue-green). 2023Q1 is the first two months of the first quarter. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: BEA, NBER and authors’ calculations.

Of course, in-sample fitting (after adjustment) is very easy. The largest recent forecast error is 0.9 percentage points in the second quarter of 2022 (the quarter after Russia expanded its invasion of Ukraine). The question is whether we should be surprised by the inflation results, given previous parameter estimates from the Biden administration. I tried to assess this by estimating the model for the period 1998-2020 (adjusted R2 0.36) and out-of-sample forecasts. The forecast is shown as the turquoise line; the forecast error for Q2 2022 is 2.3 percentage points (note that I didn’t say forecast error because I used the post-hoc realization of the variable on the right to make the forecast; alternatively, you can take 2021-22 year period is called ex-post historical simulation).

The difference is driven by a lower coefficient in the truncated sample related to expected inflation (0.24 vs. 0.44 in the full sample) and a lower coefficient for the supply chain stress coefficient (0.60 vs. 0.92 in the full sample).

Full sample estimates suggest that if GSCPI stays where it was in Q4 2020, inflation of 6.4% in Q4 2021 will change to 3.2% in Q4 2021 (with all other variables changing as they do, which is of course unrealistic ).

{kind=link}

{kind=link}