The index rose 0.9% month-on-month, compared with a 0.2% gain month-on-month.

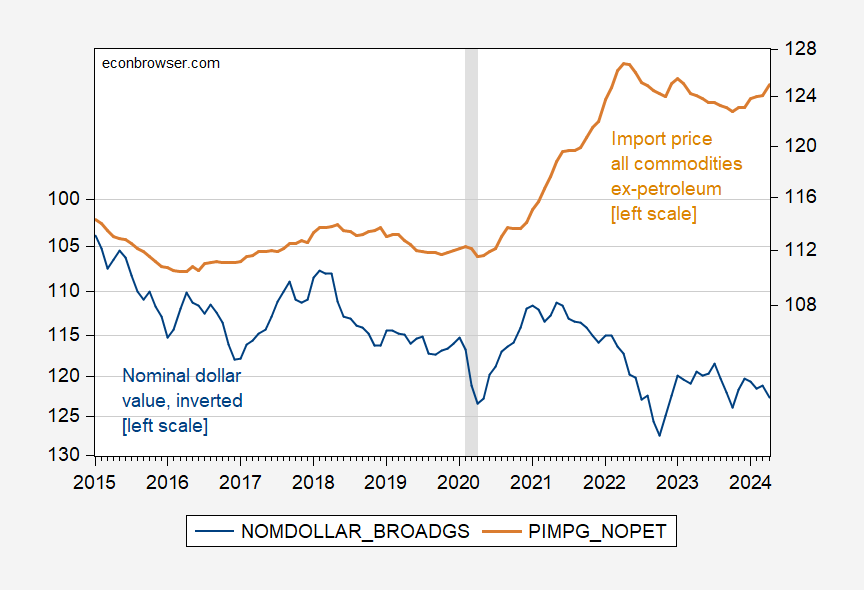

I have inverted the USD Index so that if there is exchange rate pass-through, the exchange rate and import prices should move in tandem.

figure 1: USD nominal value reversal (blue, left axis), and prices of all imports except oil, NSA (tan, right axis). NBER-defined recession peak-to-trough dates appear gray. Sources: Fed, BLS (from FRED), NBER.

Note the increase in import prices excluding oil (this is also reflected in commodity import prices). As a result, Goldman Sachs raised its PCE deflator inflation forecast by 1 basis point (month-on-month).

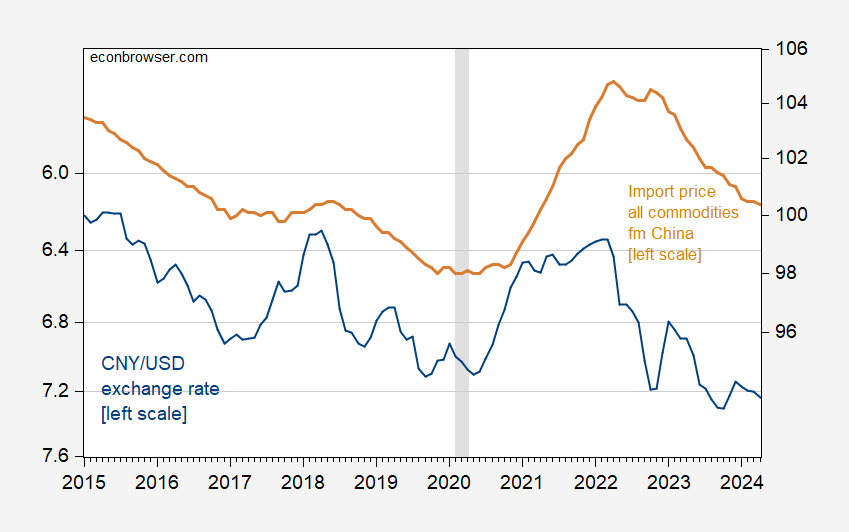

Interestingly, import prices from China track USD/CNY.

figure 2: Nominal CNY/USD reversals (blue, left axis), and prices of all imports from China, NSA (tan, right axis). NBER-defined recession peak-to-trough dates are in gray. Sources: Fed, BLS (from FRED), NBER.

Please note that import prices from China do not include customs duties costs (see here).

While the series appears to be moving in tandem, it is interesting to note that the exchange rate pass-through in the most recent period (from January 2017 to April 2024) is actually quite low , about 0.05.Using an exchange rate pass-through coefficient of 0.3 (lower than 0.5 before 2005-2010), import prices were about 5% higher than forecast (although imprecision in estimates puts actual prices within plus or minus one standard error).This would seem to indicate that U.S. tariffs do not actually depress pre-tariff import prices (i.e., essentially full tariff pass-through, as in U.S. International Trade Commission, 2023p. 145).

Warning: Regressions are of total size, so these are only rough estimates.

{kind=link}

{kind=link}