From today’s Bloomberg, “TThe post-inflation transaction is buckling across Wall Street”:

This year’s reinflation trading that has slumped bonds, pushed stock indexes to record highs and revived long-term dormant value stocks is rapidly declining.

What is driving the drama is the bond market. The yield on the benchmark 10-year US Treasury note fell below 1.3% on Wednesday as the real interest rate excluding the impact of inflation fell below minus 1%, indicating that traders are dissatisfied with the growth prospects.

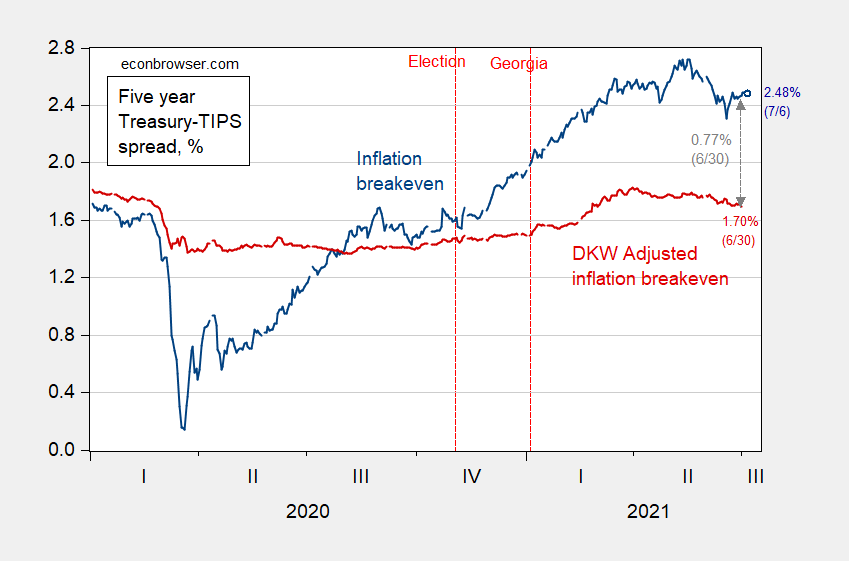

This is a 5-year situation, using standard inflation break-even calculations (negative 5-year TIPS for 5-year government bonds) and DKW adjusted inflation expectations.

figure 1: The five-year inflation break-even point is calculated as the five-year treasury bond yield minus the five-year TIPS yield (blue). The five-year break-even point is adjusted by the inflation risk premium and the liquidity premium per DKW, both in% unit. source: Feed through FRED, Ministry of Finance, Kunshan After D’amico, Kim and Wei (DKW) visited 7/7 and the author’s calculations.

Although the traditionally calculated breakeven reached a peak of 2.72% (closing price) on 5/18, the peak of the series after adjustment according to DKW was 1.81% on 3/29. As of June 30, the gap between the two series was 0.77%.

As Joseph E. Gagnon with Madi Sarsenbayev Point out, Both the bond market and economists have done a good job of forecasting (Although the performance of the DKW series does not seem to be bad In a quick and dirty comparison).

In any case, the inflation rate that the market sees in all its wisdom (or lack of wisdom) seems to be lower than previously expected.

{kind=link}

{kind=link}