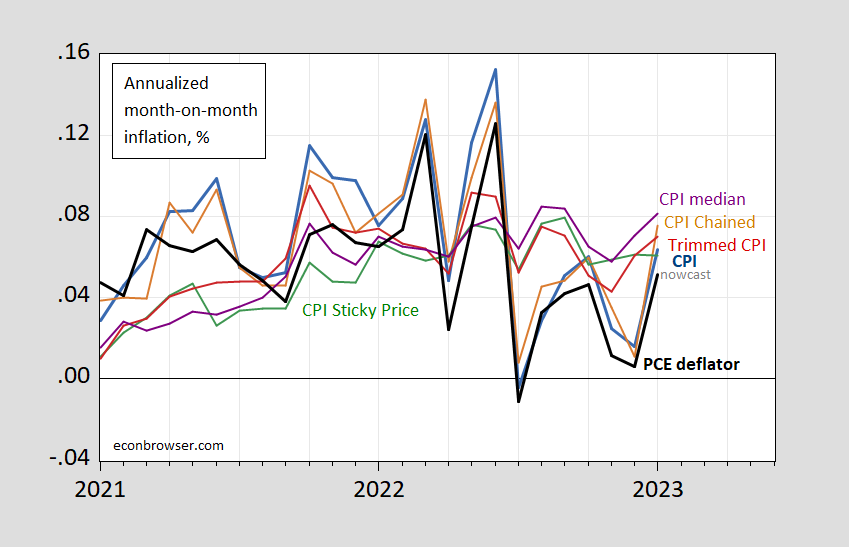

Both headline and core inflation fell year-over-year, but both were slightly above consensus (headline 6.4% vs. Bloomberg consensus 6.2%). (Month-to-month ratios are in line with consensus, rounded). Other measures provided equivocal signals.

First, we have several ways of measuring the monthly change in headline CPI.

figure 1: Month-on-month CPI inflation (blue), month-on-month CPI (brown), 16% adjusted CPI inflation (red), sticky price CPI inflation (green), personal consumption expenditures deflator inflation (black), all in decimal form (ie , 0.05 means 5%). The January PCE deflator is the nowcast of the Cleveland Fed’s 2/14. Chained CPI salog level X-13 (brown). Recession dates (peaks and valleys) shaded of gray as defined by NBER. Sources: BLS, BEA, Atlanta Fed, Cleveland Fed, and authors’ calculations.

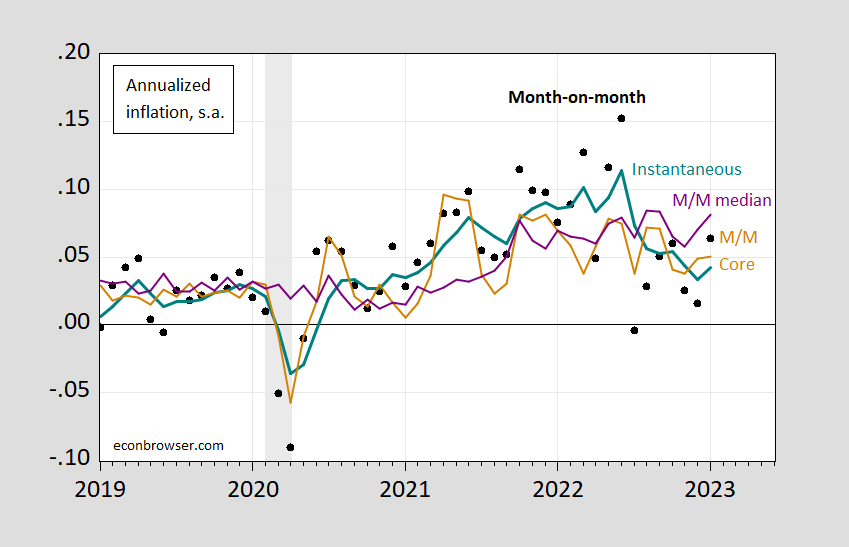

All month-on-month indicators rescued the sticky rise in price CPI inflation in January. However, we know that month-on-month changes, while providing more synchronized inflation data, have a greater noise component.Therefore, I have plotted m/m versus median, core and instantaneous (per Eckhout) inflation (t=12, a=4).

figure 2: Month-on-month CPI (black circles) and instantaneous inflation rate (τ=12, a=4) (bold turquoise), month-on-month median inflation rate (purple), month-on-month core CPI inflation rate (tan) , all calculated on an annual basis. Recession dates defined by NBER peak-to-valley are shaded in gray. Sources: BLS, NBER, and authors’ calculations.

Instantaneous (τ=12, a=4) inflation rose to 4.4% from 3.4% in December (using December’s upwardly revised CPI and incorporating new seasonal factors), but remained well below June 2022’s 11.4 %. (For further discussion of instantaneous inflation, see this postal.)

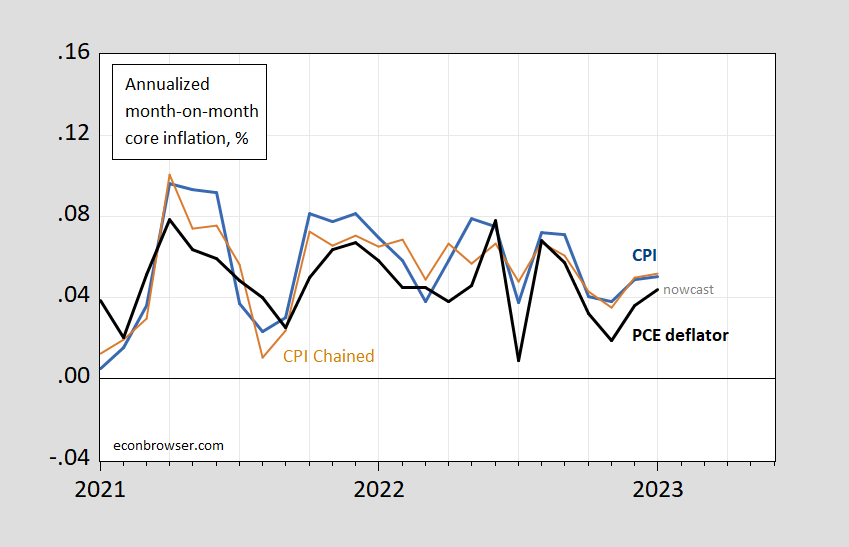

Second, core inflation measures have stabilized in the m/m range (and continue to fall to y/y).

image 3: MoM CPI core inflation (blue), MoM CPI core (brown), PCE core deflator inflation (black), all in decimal form (ie 0.05 means 5%). The January PCE deflator is the nowcast of the Cleveland Fed’s 2/14. Chained CPI seasonally adjusted log levels using X-13 (brown). Recession dates (peaks and valleys) shaded of gray as defined by NBER. Sources: BLS, BEA, Atlanta Fed, Cleveland Fed, and authors’ calculations.

Fed Funds (CME) Futures That means there was no change in rates at the March 22 meeting, but rates rose slightly in May and June.

{kind=link}

{kind=link}