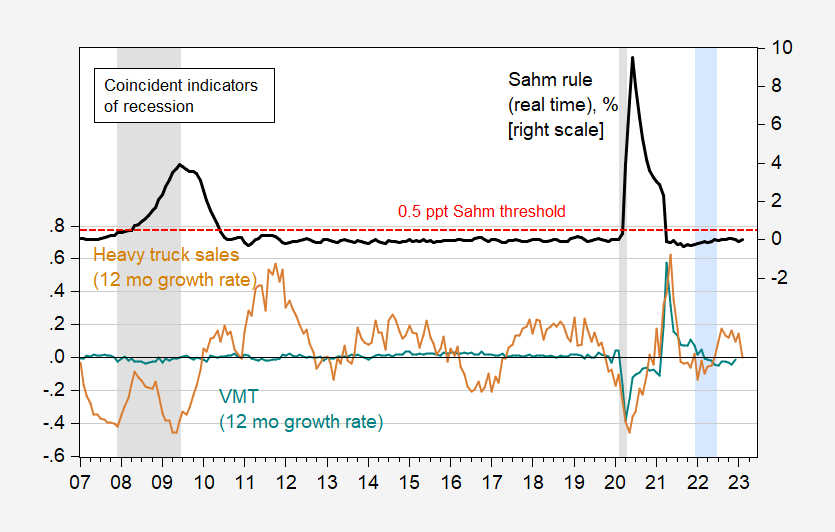

Ever wondered if vehicle miles traveled (VMT) is a good predictor of recessions?You should stop after watching this Econbrowser post on January 4th, but I thought it would be interesting to update the latest data as we get the December data. First look at the role of VMT during the recession, compared to heavy truck sales (advised at some point by calculated risk) and the eponymous Sahm rule (real-time version).

figure 1: 12-month growth rate for vehicle miles traveled, nsa (teal), heavy truck sales, sa (tan) and Sahm rule metrics – real time (black). Sahm’s rule is the 3-month moving average of the unemployment rate relative to the lowest unemployment rate over the past 12 months. The dashed red line represents the threshold for the Sahm rule metric. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Hypothetical 2022H1 recession shaded lavender. Source: FHA via FRED, Census via FRED, FRED, and NBER.

It’s hard to see, but the 12-month change in VMT was down a few months ago before recovering in December (which Mr. Steven Kopits pointed to), while heavy truck sales were up year-over-year in January. As of yesterday’s February data, the Sahm rule is at exactly zero (0.5 percentage points are needed to cross the threshold).

In any case, VMT growth is a poor indicator of recession (McFadden R2 of 0.07) compared to heavy truck sales (0.28) (see regression results in this report) postal).

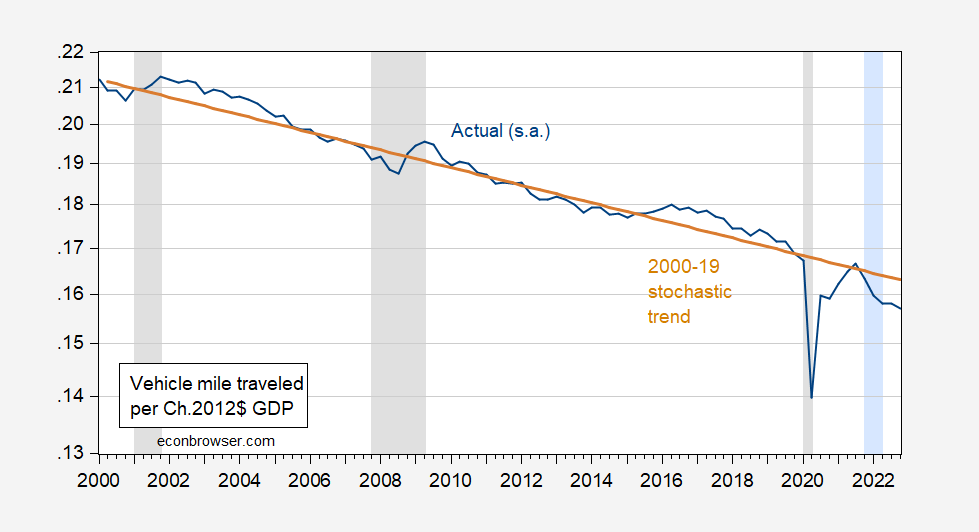

Going forward, I would be more cautious about using VMT as an indicator, as the relationship between VMT and GDP appears to have undergone a structural break. In Figure 2, I plotted vehicle miles driven (seasonally adjusted) against US GDP per quarter (so the units are vehicle miles driven/real USD GDP). During the period 2000-19, there was a clear trend, with an annual decrease of 1.15%. (Given my inability to reject a unit root in the log ratio, I estimated a random trend.) Using the estimated trend forward, I get:

figure 2: Vehicle miles traveled in 2012 USD GDP (blue line) and estimated stochastic trend from 2000-19 (tan line), on a logarithmic scale. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Hypothetical 2022H1 recession shaded lavender. Sources: FHA, BEA, NBER, and authors’ calculations.

In other words, Mr. Kopits sees the downshift to what appears to be a new trendline as a cyclically induced reduction in VMT.

{kind=link}

{kind=link}