Today, CEA published a Blog post Regarding the question of how the government’s infrastructure and “rebuild better” plan will not lead to inflation. I think it’s interesting to see how the market (which will undoubtedly prove to be wrong) sees inflation and output will evolve.

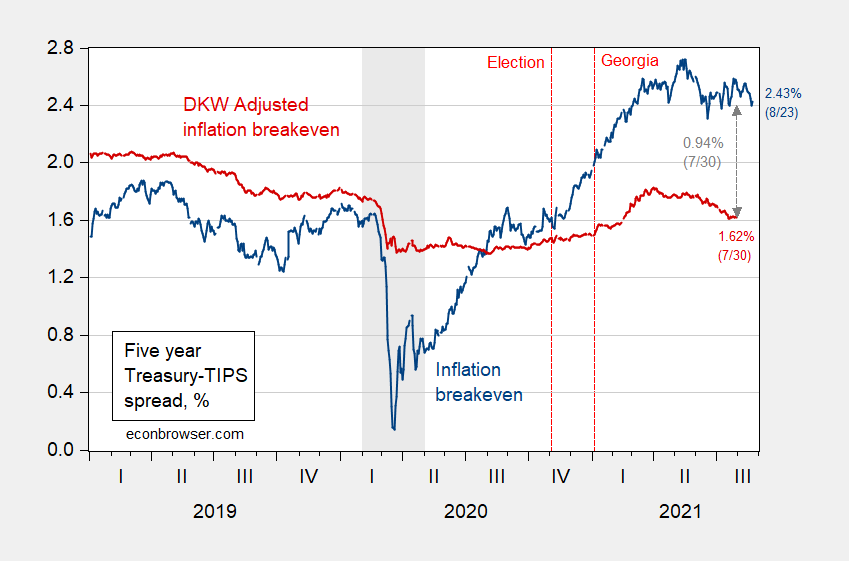

For the medium-term inflation expectations, I will focus on the five-year inflation break-even, and the expected inflation in the next five years that is inferred using the break-even and additional surveys and market information.

figure 1: The five-year inflation break-even point is calculated as the five-year treasury bond yield minus the five-year TIPS yield (blue). The five-year break-even point is adjusted based on the inflation risk premium and the liquidity premium per DKW (red). All are in %. NBER defines recession dates as shades of gray (from the beginning of the peak month to the end of the trough month). Source: FRB through FRED, Ministry of Finance, Kunshan After D’amico, Kim and Wei (DKW) interviewed 8/5, NBER and the author’s calculations.

The implied inflation rate calculated by a simple break-even calculation is the same as around June 9, 2021 in the past two and a half months.

As the term spread implies, the expected slowdown in inflation in the past five months is partly due to the slowdown in expected growth.

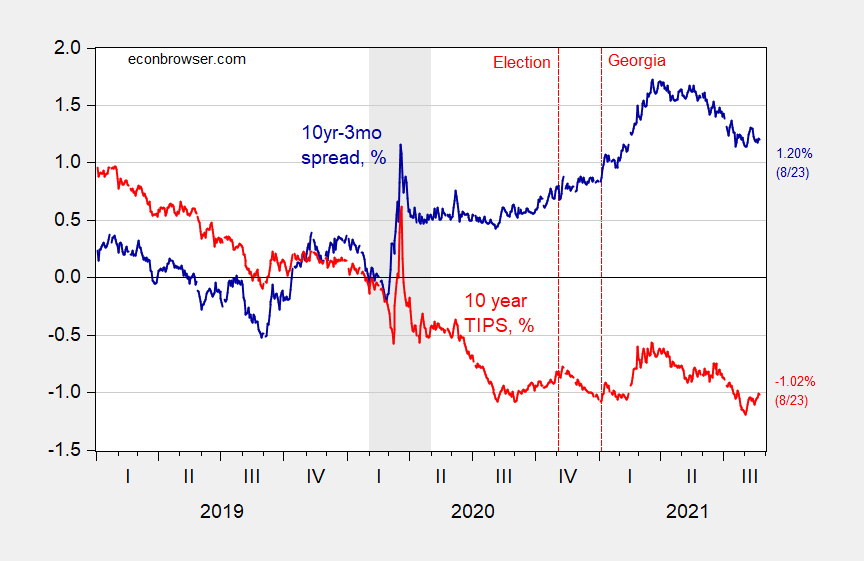

figure 2: Ten-year and three-month Treasury bond spreads (blue) and ten-year TIPS yield (red), both in %. The decline date defined by NBER is shaded in gray. Source: Ministry of Finance, NBER and author’s calculations.

It is true that the link between maturity spreads and growth (and recession) is loose, but the decline in real interest rates, as measured by the 10-year TIPS yield, supports the implications of lowering expected growth.

For me, this implies a Inflation anxiety continues to decline, with Worries about the pace of recovery intensify.

{kind=link}

{kind=link}