The October employment report provided many interesting facts. First, employment growth was faster than expected, and second, employment growth in September was faster than originally estimated.

figure 1: Non-agricultural employment (black), private non-agricultural employment (blue-green), and civilian employment (red) were all in the 2000s. The NBER-defined recession date is gray. Source: US Bureau of Labor Statistics, US National Bureau of Statistics.

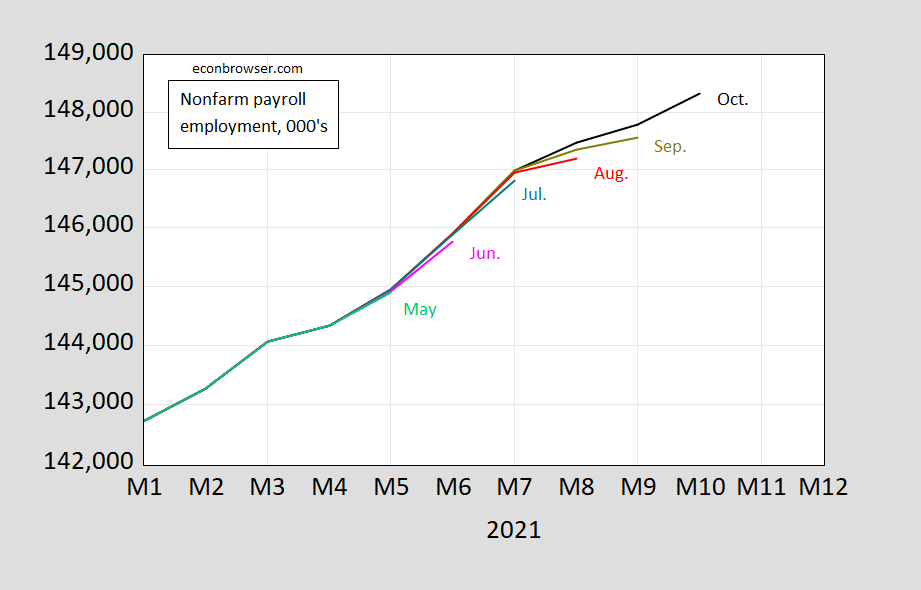

The originally mediocre September data has been revised upwards significantly. This is a pattern that has occurred in the past five months, although it was not so obvious in the previous situation.

figure 2: The number of non-agricultural employment in October (black), September (yellow-brown), August (red), July (blue-green), June (pink), and May (light green) was in the 2000s. sa source: BLS.

This reminds people that the first reading of employment data is an estimate.The average absolute revision of the monthly changes between the first and second estimates is 48 (in thousands), and the average absolute revision between the first and third estimates is 61 (full results are in Bureau of Labor Statistics).

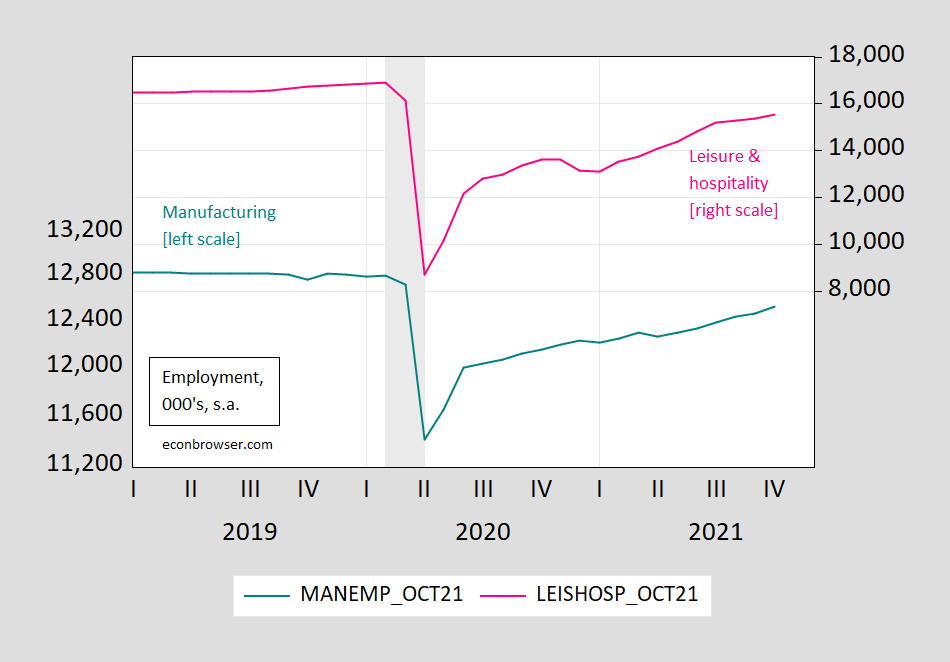

Note that from August to October, the growth rate of high-touch services approximately doubled, due to the weakening of the delta surge. Manufacturing has accelerated, but not so obviously.

image 3: Manufacturing employment (cyan, left logarithmic scale), leisure and hospitality employment (pink, right logarithmic scale), are in the 2000s, and the recession dates defined by NBER are shaded gray. Source: US Bureau of Labor Statistics, US National Bureau of Statistics.

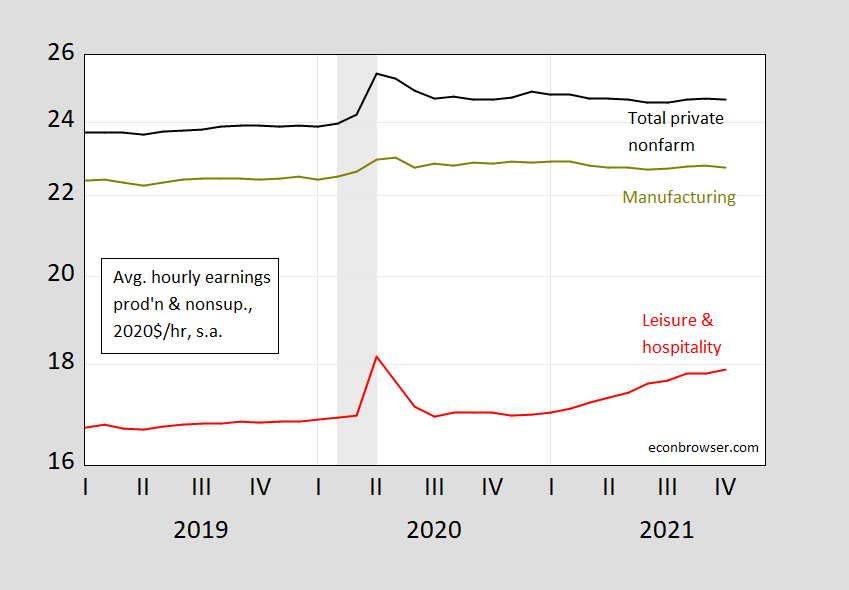

Finally, while there are concerns that inflation will erode wage growth, it is important to note that for the entire private sector and manufacturing industry, average real (CPI reduction) wages are higher than they were at the beginning of the pandemic. For the leisure and hospitality industries, real wages are much higher than pre-pandemic levels and are still rising rapidly.

Figure 4: Non-agricultural wage production and non-regulated average hourly income (black), manufacturing (yellow-green), leisure and hospitality (red), all in 2020, sa (CPI reduction). The October earnings observation uses the current forecast CPI as of November 5th. The decline date defined by NBER is shaded in gray. Source: U.S. Bureau of Labor Statistics, Cleveland Federal Reserve, NBER and author’s calculations.

If people care about the actual income of those at the lowest end of the salary range—such as leisure and hospitality—people should be happy to see the latter trend (5.6% y/y, 5.0% m/m AR, using real-time forecast October CPI).

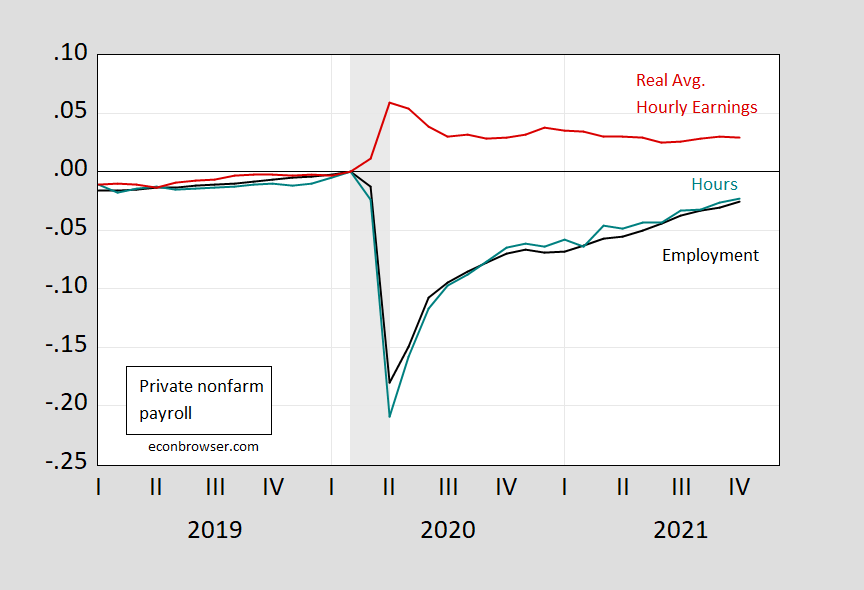

The final snapshot of private sector employment, working hours and real wages:

Figure 5: Private non-agricultural employment (black), total working hours of production and non-supervised workers (blue-green), actual average hourly income in 2020 $/hour (red), all October income observations are used as of 11/5 The current forecast CPI. The decline date defined by NBER is shaded in gray. Source: U.S. Bureau of Labor Statistics, U.S. National Bureau of Statistics, Cleveland Federal Reserve, And the author’s calculations.

{kind=link}

{kind=link}