Productivity growth underperformed (-2.7% vs. Bloomberg consensus -1.8%, AR quarterly), while unit labor costs unexpectedly rose (+6.3% vs. +5.5% consensus, prior to 3.3%).

As output falls, hours worked increase. Seems like pretty bad news, but I think it’s useful to put these recent growth rates in context by looking at levels.

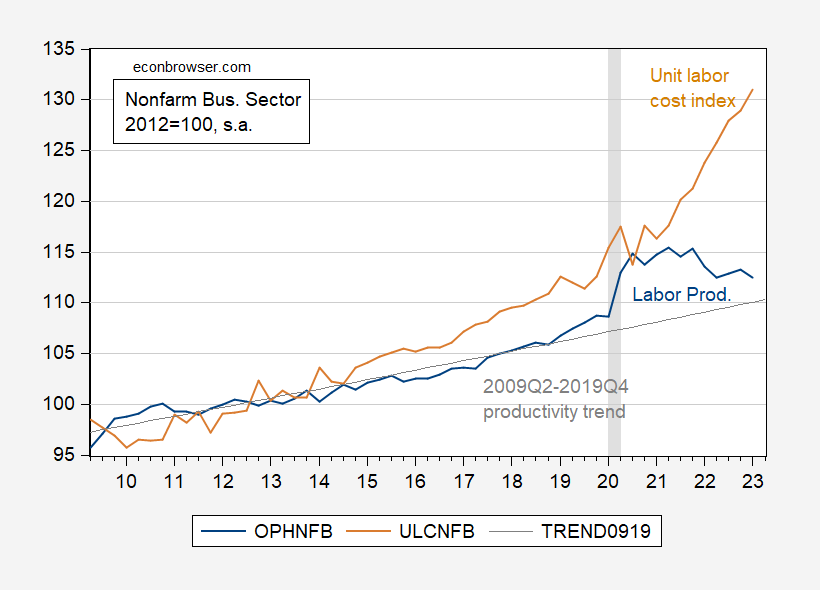

figure 1: Non-farm business sector output per hour index (blue), 2009Q2-2019Q4 deterministic trend (gray line), and unit labor cost index (tan), all 100 in 2012, all on a logarithmic scale. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: BLS, NBER, and authors’ calculations.

The lackluster productivity growth should be viewed in the context of the large surge in measured productivity associated with labor losses during the pandemic and underemployment relative to pre-pandemic trends. Current levels are above pre-pandemic trends (which is not where productivity should be – it depends on many other factors). Now, we are adjusting from labor loss to labor hoarding, which explains the reduction in labor. measured Labor productivity.

(Note that these estimates are subject to revision over time; the 80% change from early to final release to q/q AR productivity ranges from -1.0% to +1.4%.)

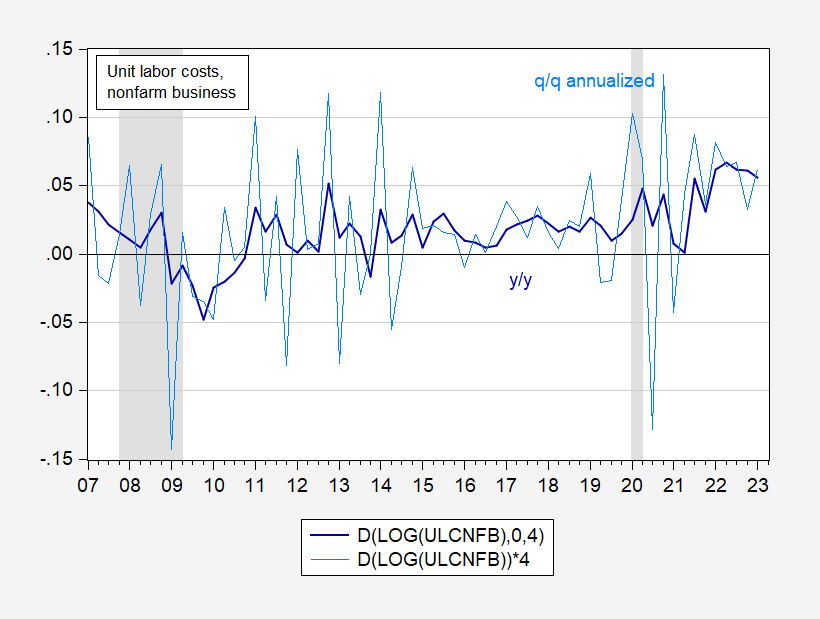

On the other hand, unit labor costs—the ratio of compensation to actual output per hour—continue to rise. One way to think about this variable is that it represents a form of cost-push shock. Therefore, the rapidly rising unit labor cost (ULC) index poses a more serious challenge to the Fed than the decelerating ULC growth.

figure 2: Unit labor cost (ULC) year-over-year (dark blue) and quarter-over-quarter annualized growth (light blue) are calculated using log differences. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: BLS, NBER, and authors’ calculations.

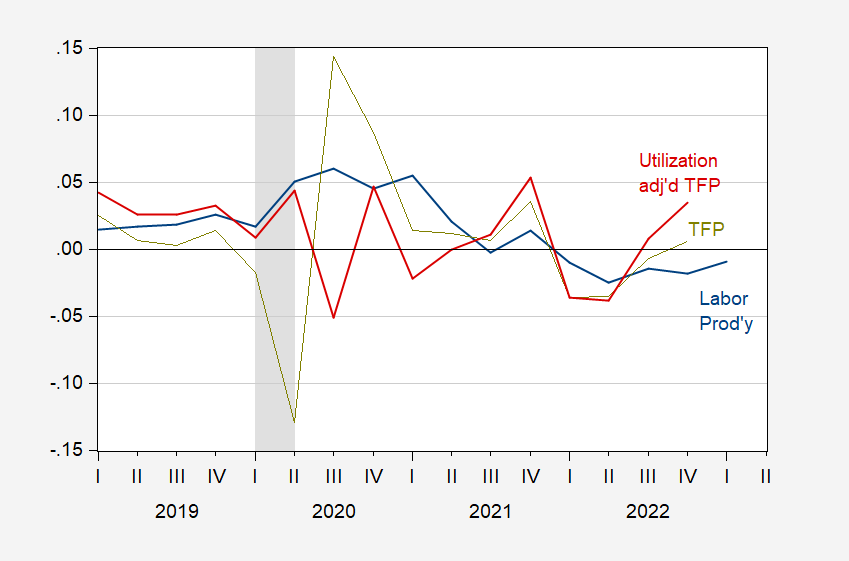

Final note: We rely on labor productivity because we believe our estimates of it are more accurate than total factor productivity. In fact, the calculation of total factor productivity (TFP) is also affected by changes in capacity utilization (hence capital “hoarding” and labor hoarding).Below I show year-over-year growth in labor productivity (from Figure 1) compared to year-over-year growth in TFP and utilization-adjusted TFP, estimated John Fernard.

image 3: Year-over-year growth rates of output per hour (blue), total factor productivity (yellow-green), and utilization-adjusted total factor productivity (red), all calculated using log differences. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Source: BLS via FRED, Fernald/San Francisco FedNBER, and author’s calculations.

{kind=link}

{kind=link}