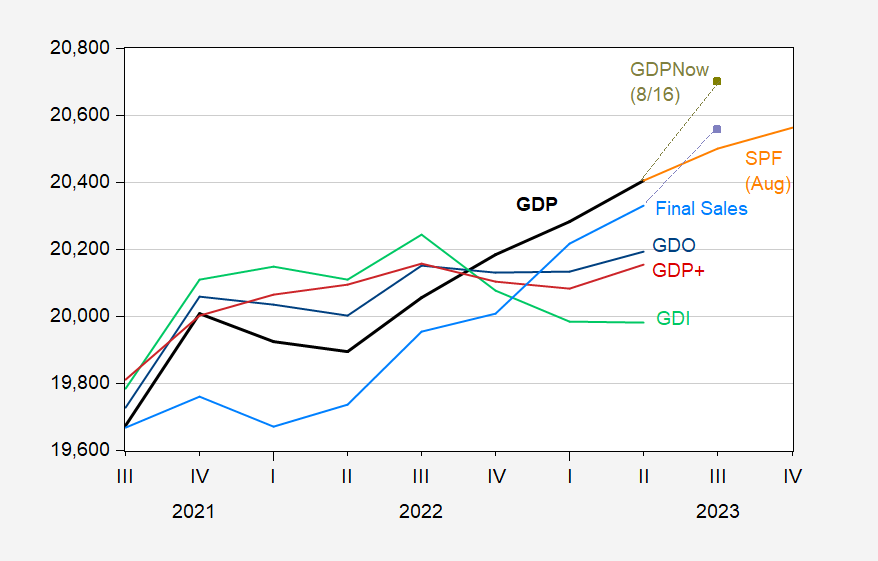

To see how far this bean counting method deviates from the consensus, consider the following graph:

figure 1: GDP (bold black), GDPNow as of 8/24 (yellow green square), GDI (light green) GDO (blue), GDP+ (red), final sales (light blue), GDPNow as of 8/24 Final Sales (lavender squares), Professional Forecasters Survey August Survey Median (orange), all in billions. Ch. 2012$ SAAR. GDO assumes a $100 billion decline in net operating income for the second quarter. The GDP+ level GDP+ growth rate is based on the Q4 2019 GDP iteration. Source: BEA Q2 2023 Advance, atlanta fed (8/24), philadelphia fed (7/28), philadelphia fedand the authors’ calculations.

GDI for Q2 2023 is not available, but all but one major component (net profit) is reported. Assuming a net profit decline of $100 billion (SAAR) in Q2, I estimate Q2 GDO in Figure 1.

Note that final sales are also expected to rise, so the exaggerated GDP forecast is not primarily due to inventory buildup. More than half of the growth was attributable to increased consumption.

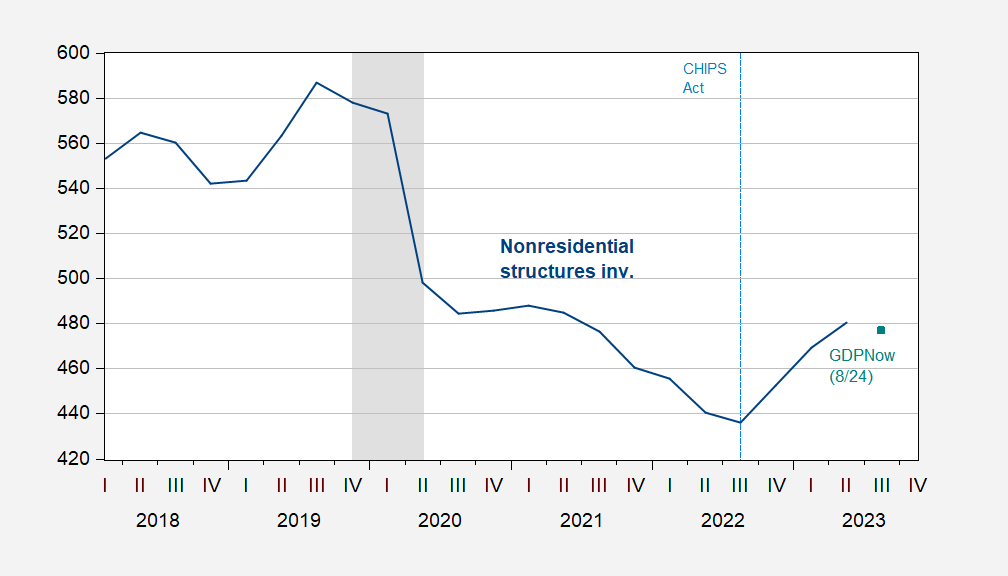

An interesting aspect of the results is the (expected) end of the non-residential investment boom.

figure 2: Structural nonresidential fixed investment (blue) and 8/24 immediate forecast GDPNow (teal boxes), all in billions. 2012 quarterly US dollars, seasonally adjusted earnings. Recession peak-to-trough dates as defined by NBER are grayed out. Sources: BEA, Atlanta Fed (8/26), NBER.

{kind=link}

{kind=link}