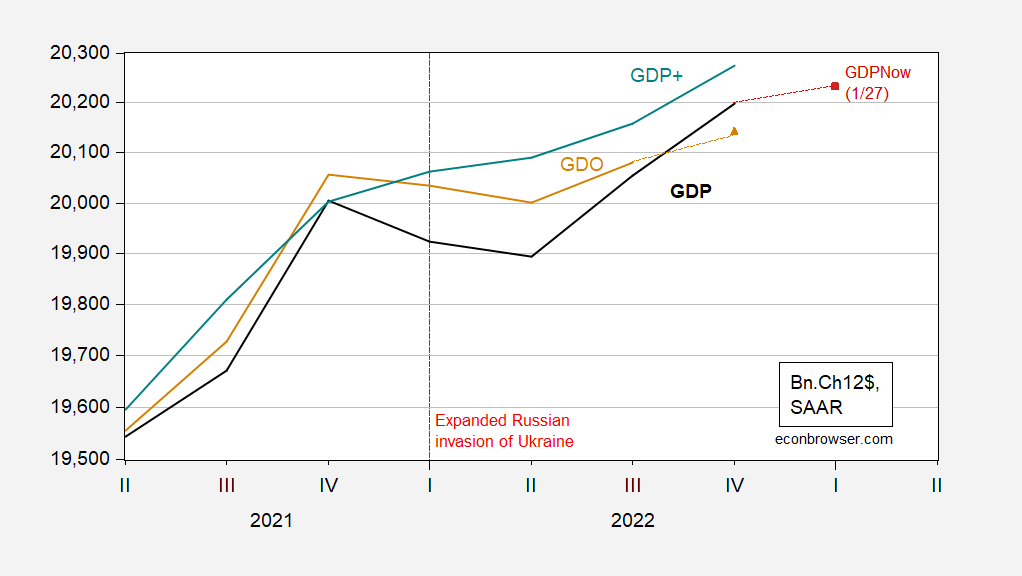

According to some composite measures, the economy will slow down in the first half of 2022, but GDP+ does not indicate that.

figure 1: GDP (black), 1/27th of GDPNow (red squares), GDO (tan), GDO estimate for Q4 (tan triangles), GDP+ (teal), all in billions Ch.2012$ SAAR. 4Q2022 GDO is based on GDI with net operating surplus set equal to 2021Q3 value. The GDP+ level calculated by iteratively calculating the growth rate of real GDP in the fourth quarter of 2019. Source: BEA, 2022Q4 advance, Federal Reserve Bank of Atlanta, Federal Reserve Bank of Philadelphiaand the authors’ calculations.

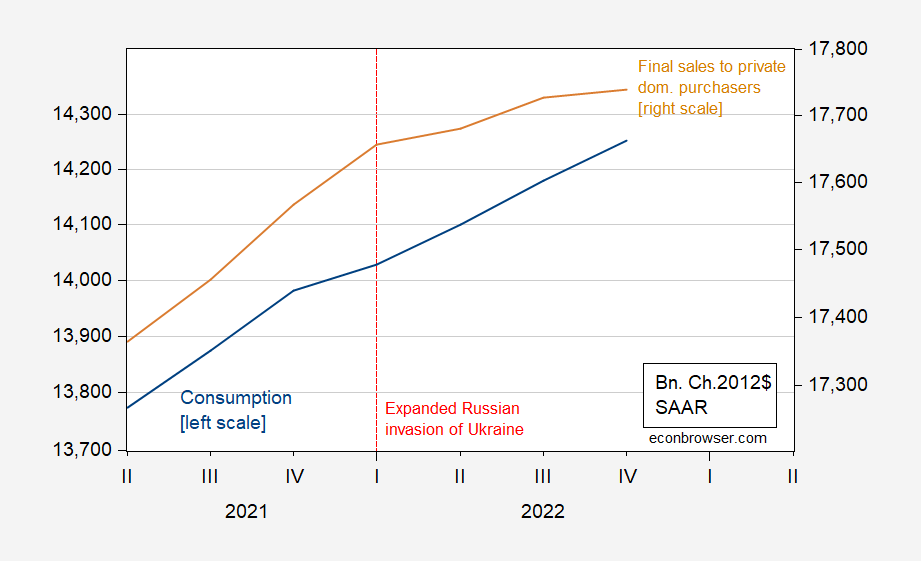

Although GDP and GDO fell in the first half, it is interesting to note that neither final sales nor consumption to domestic private buyers fell.

figure 2: Consumption (blue, left scale) and final sales to domestic private buyers (tan, right scale), both in billions. 2012 $SAAR. Source: BEA 2022Q4 advance release.

In every recession (as defined by the NBER) since 1967, final sales have always fallen. The same is true for consumption, except for the recession of 2001 ( wall street journal Median Response to January Survey Indicates that the recession will begin in the first quarter of 2023, GDPNow as of 1/27). In other words, a recession does not appear to be on the horizon; given what has happened before, 2022H1 does not appear to be in sight either, employment trendsand the Sahm rule (against Kopits).

{kind=link}

{kind=link}