Data released yesterday (chronic fatigue syndrome, SPGMI) until August.

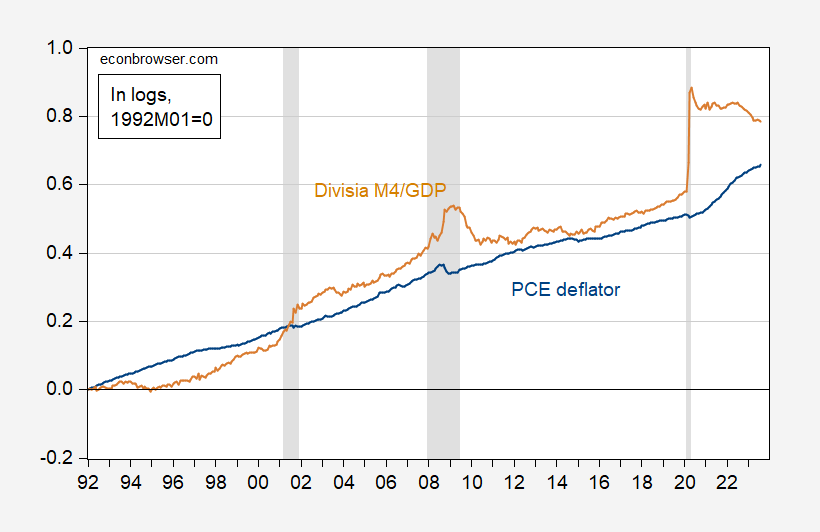

figure 1: PCE deflator (blue), Divisia M4M divided by real GDP (tan), both logarithmic 1992M01=0. NBER-defined recession peak-to-trough dates appear gray. Source: BEA, via FRED, center for financial stability, SPGMINBER, and author’s calculations.

This plot is motivated by quantity theory (the broadest divergence index is used here, as requested by a reader).

MV=PQ

Where medium size It’s money, V is the speed, phosphorus is the price level, ask is an economic activity.

think V’ is a constant; then:

MV’ = PQ

Get the log (where lowercase letters represent the log value).

p = m + v’ – q

During the period 1992-2019 (pre-pandemic), the multivariable cointegration test (constant cointegration vector in VAR, but no deterministic trend in the cointegration vector, 4 lags in the first difference) failed to reject the no cointegration null value .

Instead of assuming a long-run trend speed (which is consistent with a stable long-run money demand equation), we can assume a long-run relationship between speed and interest rates.

p = m + v(i) – q

where i is the interest rate. Coupled with own interest rates calculated by the Center for Financial Stability, the same norm fails.

If 2020-2023M08 data is added, cointegration is found at 5% msl of the trend stationary speed specification. If interest rate is included, it is 10% MSL. Unfortunately for this version of quantity theory, the sign of the interest rate is wrong (as long as one believes the money demand equation).

If you are forced to make forecasts based on (interest-free) quantity theory models, you run into a small problem: in addition to not being able to find cointegration, the money-to-GDP ratio seems to recover error corrections—not the PCE deflator.

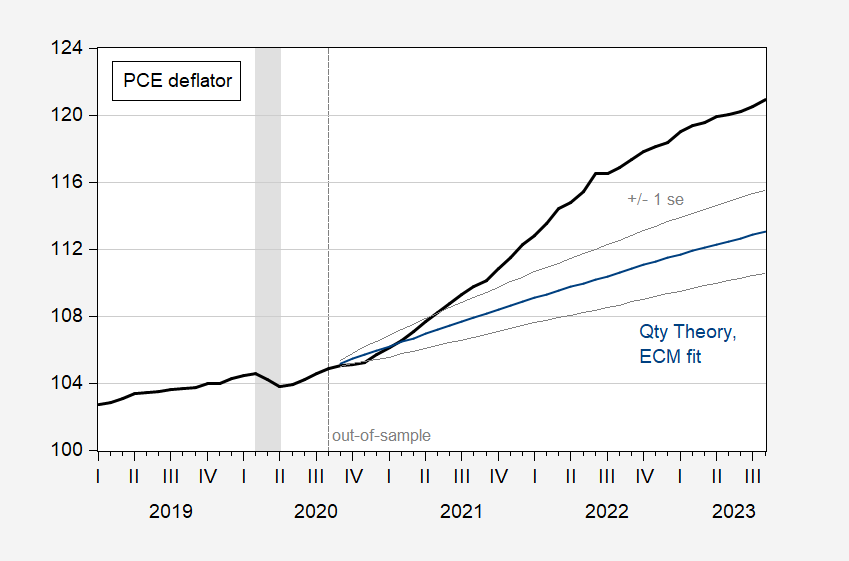

I estimate a single-equation error correction model from 1992 to 2020.08 (which includes the large jump in Divisia M4) and perform dynamic forecasts out-of-sample. This is what I got.

figure 2: PCE deflator (black) and dynamic out-of-sample forecast (blue), +/- 1 standard error (grey line). NBER-defined recession peak-to-trough dates appear gray. Source: BEA and author’s calculations.

While one can find other parameter estimates that are equally reasonable, my point here is that literal quantity theory does not necessarily fit the data well.

{kind=link}

{kind=link}