Olivier Blanchard and Larry Summers have an interesting exchange On interest rates and secular stagnation, and target inflation today, in PIIE. Blanchard mentioned the evolution of r and g as a key issue in thinking about secular stagnation, which prompted me to look at the data.

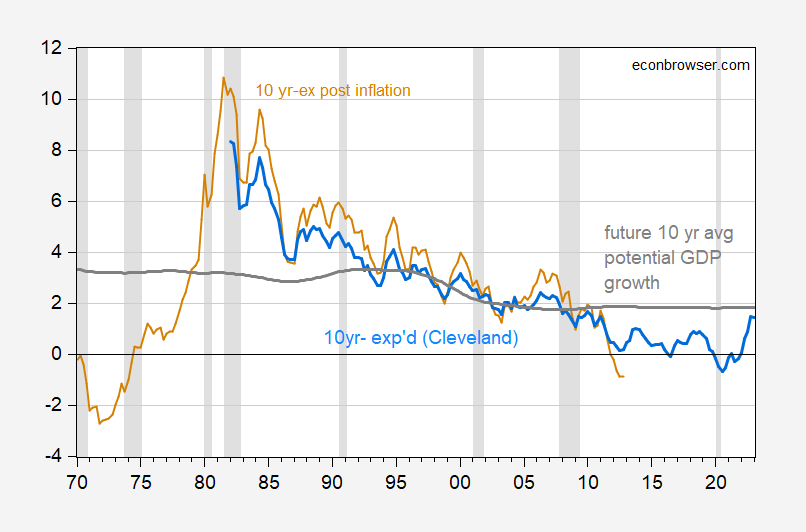

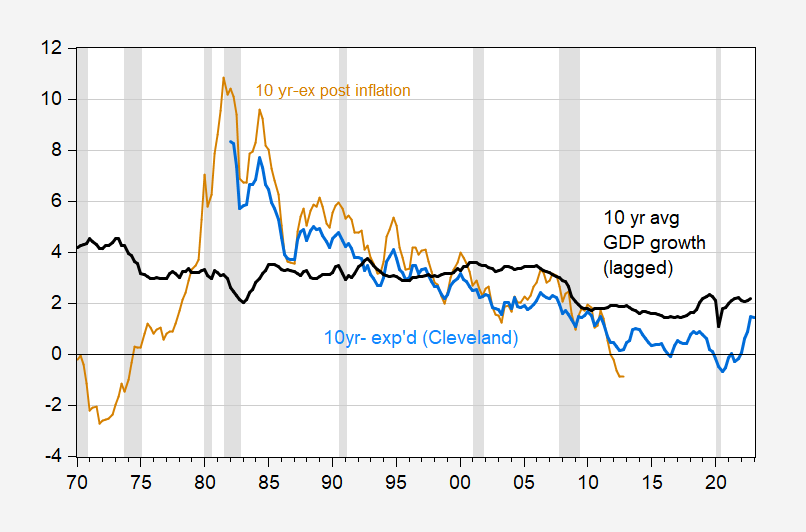

First, the real 10-year Treasury rate adjusted for expected inflation compared to the 10-year growth rate over the past decade.

figure 1: Ex-post inflation-adjusted 10-year Treasury yield (tan), Cleveland Fed inflation forecast (blue), and average GDP growth over the past decade (black). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Source: Treasury Department via FRED, Cleveland Fed, BEA, NBER, and author’s calculations.

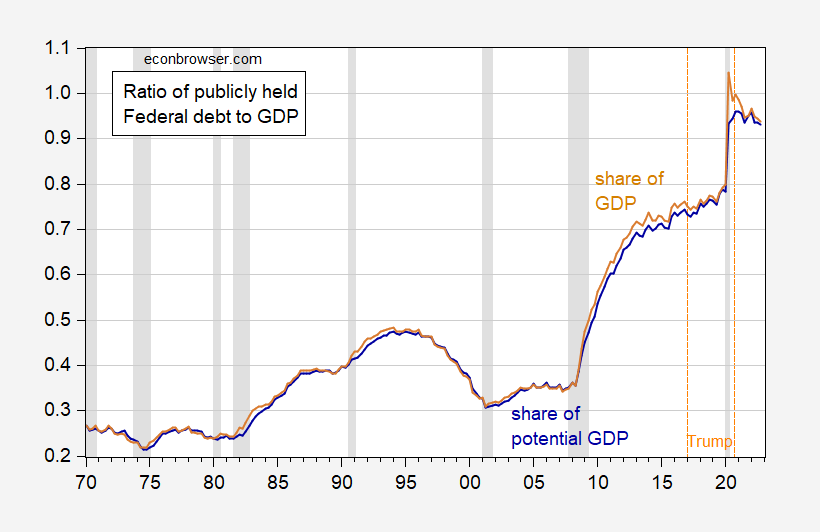

In fact, it might be better to consider real interest rates and growth rates for the relevant period. We could calculate and use the ex-post growth rate of GDP (ending with observations in Q4 2012), but I use the CBO’s estimate of potential growth.

figure 2: Ex-post inflation-adjusted 10-year Treasury yield (tan), Cleveland Fed inflation forecast (blue), and average potential GDP growth over the next decade (gray). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Source: Treasury via FRED, Cleveland Fed, CBO, NBER, and author’s calculations.

G > r Over the past ten years, including 2020-21. Now the two have converged, but given the recent evolution of these two rates, we can see why the debt-to-GDP ratio has not exploded, postal– Trump, despite huge deficits (in dollar terms).

image 3: Federal debt held by the public as a share of GDP (tan) and as a share of potential GDP (dark blue). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: Treasury, BEA via FRED, CBO, NBER, and author’s calculations.

To recap, this expression describes the dynamic relationship between debt and GDP.

(1) dTon-dt-1 = [(rt-gt)/(1+gt)]× dt-1 –pTon

Where d is the debt-to-GDP ratio, r is the real (inflation-adjusted) interest rate, G is the growth rate of real GDP, and p is the ratio of primary (non-interest) surplus to GDP. In other words, when the gap between real interest rates and growth is large enough or the primary deficit is large enough, the debt-to-GDP ratio rises.

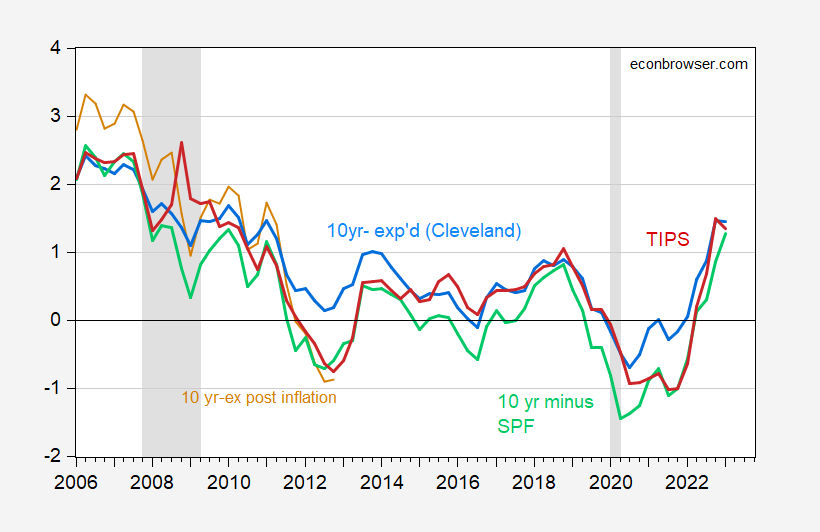

Note that for the first two months of the first quarter of 2023, the different measure of expected inflation is similar to the measure of the real 10-year rate.

Figure 4: Ten-year Treasury yield based on ex-post inflation for the following decade (tan), Cleveland Fed projected ten-year inflation (blue), SPF projected ten-year median inflation (green), and TIPS ten-year yield (red) Adjustment. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. 2023Q1 observation is the first two months. Source: Treasury Department via FRED, Cleveland Fed, BEA, NBER, and author’s calculations.

Clearly, if real interest rates rise further, or the growth outlook weakens, then the debt dynamics will not work in our favor.

{kind=link}

{kind=link}