Two big things happened yesterday (March 7, 2023). First of all, my birthday present was a lovely bouquet of sunflowers. This is the trump card. Second, the RBA board ousted its governor to announce the 10th consecutive rate hike, even though inflation has been falling for several months. The RBA is getting ridiculous now, and the government should absolutely terminate the governor’s term in September when his term expires. In the meantime, it should clean up the RBA board, or introduce legislation requiring every member, including the governor, to deduct a percentage of their own wages towards the actual discretionary losses they impose on workers. Further deductions (amount to be determined) will be made for each percentage point increase in the unemployment rate. It might give them pause for thought. After watching The Haze below, the music section is sure to lift your spirits.

Huge loss of average real household disposable income – deliberately engineered by the RBA

I will quickly return to yesterday’s RBA decision.

As part of the publications suite following the monthly board meeting, the RBA has published – March 2023 Australian Economy and Financial Markets Chart Pack (Published March 8, 2023).

The package contains various information about the economy that the RBA claims is used to justify the interest rate decision released the previous day.

This graph (taken from the data pack) shows the collapse in consumer confidence since the rate hike 11 months ago.

The global financial crisis and pandemic are bad enough, but the RBA engineered something shocking.

Keep this in mind when I analyze decisions.

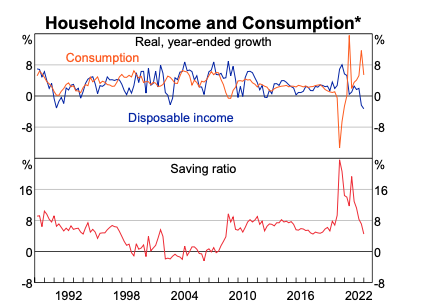

The figure below shows the impact of the decision on household consumption expenditure, household disposable income, and the household saving rate.

The only reason consumer spending is holding up is because households now have much less disposable income to save.

Remember, this is a general description of the situation.

For many low-income households with zero savings stocks and low income saving capacity, they will now sink into the abyss, swallowing what little wealth they may have or going bankrupt.

At the other end of the wealth scale, those at the top will be banking on rising interest rates and income growth from the massive redistribution of income and wealth engineered by the RBA.

The graph also shows that disposable income is now generally declining.

The RBA conveniently shows nominal disposable income, failing to adjust for population growth.

Even on these fronts, things are bad and getting worse.

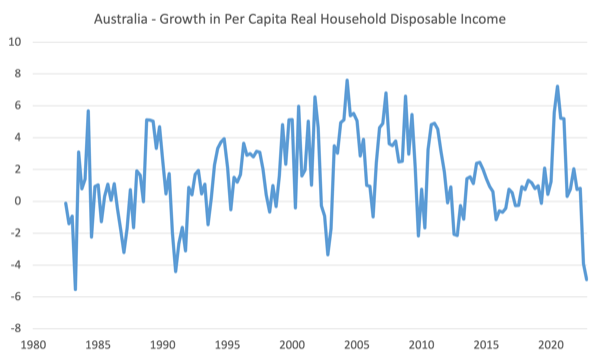

But I adjusted for changes in consumer prices using deflat0r, the implied price of household final consumption expenditures from the December 2022 quarterly national accounts published last week.

I also corrected for population growth to get a real measure of household disposable income per capita, the next chart I constructed shows the annual change in this measure, so it can be compared to the RBA’s RBA in the previous chart benchmarks for comparison.

In the 12 months ending December 2022, real per capita household disposable income fell 4.9%, a catastrophic decline on par with the worst recession in recent history.

The graph covers the 1982 recession – real household disposable income per capita fell by 5.53% (June 1982 to June 1983); the 1991 recession (worst since the Great Depression) – falling 4.39% (March 1990 to March 1991); Global Financial Crisis – down 2.17% (December 2008 to December 2009); and Pandemic – no decline due to financial support for households.

As a result, the current period has seen the largest reduction in real per capita disposable income of households except 1982, and the situation will decline further in the coming months.

Also keep in mind that this aggregate figure masks the distributional effects of income size.

The cuts to low-income households with mortgages would go well beyond that.

The RBA is wreaking havoc on families in this country.

They are irresponsible, unelected and the government should intervene to stop the rate rise and fire the governor and his board.

RBA decision and rationale

As I was stretching after my run this morning, the RBA governor was on the TV screen trying to justify the unreasonable.

He smugly told us that inflation was the worst problem we could have and that while he didn’t want unemployment to rise, the RBA would push unemployment as high as necessary to bring inflation back to 2% to 3%.

He talked a lot about the ills of inflation, but said almost nothing about the devastating effects of unemployment on society.

In any case, unemployment is the worst of the double disaster.

Losing your job, then your house, then all your savings, then, in many cases, your family, and your physical and mental health – all are part of the unemployment story, not to mention the destruction of self-esteem and confidence — Worse than being squeezed by some price hikes.

Especially when the current inflation is weakening anyway, because the factors that caused the pressure are being cleaned up.

This reduction has nothing to do with rising interest rates.

inside – Governor Philip Lowe’s Statement: Monetary Policy Decision (Published 7 March 2023) – The RBA was unaware of the damage it intentionally caused.

First, it also raised the “Foreign Exchange Settlement Balance Rate” while raising the cash rate target again.

For those who don’t know, ES balances are what Americans call bank reserves.

They are accounts that commercial banks must open with the RBA to facilitate the development of the payments system.

Currently, there are excess accounts due to the RBA’s government bond buying spree during the pandemic.

So not only does the RBA penalize mortgage holders by raising interest rates, the support rates they pay banks also provide an income fortune to bank shareholders, who are often high-income and high-wealth citizens.

This redistribution from poor to rich is in addition to the basic redistribution brought about by the effect of interest rates on wealth holdings.

The RBA acknowledged:

Monthly CPI indicators suggest that inflation in Australia has peaked.

It’s been down for months.

They also admit:

Medium-term inflation expectations remain firm…

The RBA’s argument is that everyone knows that inflation is supply-driven right now, and those drivers are coming down, so is inflation.

Why do citizens instinctively believe that inflation is temporary, while policymakers keep bashing it as a possible wage-price spiral and must be hammered on the head with the biggest sledgehammer they can afford?

The RBA acknowledged:

Australia’s economic growth slowed, with GDP rising 0.5% in the December quarter and 2.7% for the year. Growth in the coming years is expected to be below trend.

Read: well below trend.

GDP growth will be well below 2% through the March quarter and falling.

The trend growth rate is about 3.2% to 3.5%.

If this level is not reached, unemployment will rise rapidly.

RBA abuse history:

The labor market remains very tight, although conditions have eased. Unemployment remains near a 50-year low.

Yes it does.

But the reference period is flawed.

The 50-year period mentioned is actually the neoliberal period, when unemployment was kept deliberately high by flawed monetary and fiscal policies.

So it’s not a good thing to say we’re back where this ugly period of history began.

Why not 60 years?

That would take us back to a period of true full employment, when the unemployment rate was below 2%, rather than the current 3.7%.

Furthermore, during periods of full employment, there is almost no underemployment.

Currently, the underemployment rate is 6.1%, and on average, the underemployed need to work about 14 extra hours a week.

As a result, the broad labor underutilization rate (unemployed and underemployed) is 9.8% – meaning Australia’s labor market is not very tight at all, with many working hours not at full employment.

The RBA Governor made the bold claim on TV this morning that we are at full employment.

I almost pulled a muscle when he said that.

The RBA maintains the “fear” of a distributional struggle, which they now refer to as a price-wage spiral.

Apparently, the private data they interviewed with companies still showed something that all the official data didn’t – dangerous wage pressures.

They should release this data and let experts like me interrogate its basis.

I bet the companies are making up a story because the managers are somehow benefiting from rising rates.

None of the public figures released by the Australian Bureau of Statistics show a sharp cut in real wages and low pressure on nominal wages.

Finally, the RBA acknowledged:

…monetary policy is running with a lag, and the full impact of the cumulative rise in interest rates has yet to be reflected in mortgage payments. There is uncertainty about the timing and extent of the slowdown in household spending.

In fact, like all central banks, the RBA does not know when these changes will have an impact, how they will affect and who will benefit the most and who will be hurt the most.

In fact, they are only pushing for rate hikes when there are so many indicators that: (a) inflation is temporary and falling; (b) low-income households are going bankrupt; Push up the unemployment rate, and that will make things worse — that’s untenable.

The RBA has been in this situation before – on both sides of the dynamic – with rates falling too late and rates rising too early, and too many times.

This means that monetary policy is not a good anti-stability tool.

So while the RBA is frantically imitating the Fed, thankfully we do have another approach.

The Bank of Japan is not raising interest rates and the Cabinet Office is using fiscal transfers to shield households from cost-of-living pressures.

Why would they do that? Because they understand that inflation is temporary, they don’t want to create other problems by driving up unemployment and forcing mortgage holders into bankruptcy.

In its most recent— Economic Activity and Price Outlook (January 2023) – The Bank of Japan states:

The year-over-year increase in the CPI … is likely to be relatively high in the short term due to the pass-through to consumer prices from higher costs due to higher import prices. Growth is projected to moderate by mid-FY2023 due to the waning of these effects, and the impact of government economic measures to depress energy prices…

However, growth is expected to slow to below 2% by mid-FY2023

They said monetary policy settings would not change.

We’ll see how it turns out.

Music – Nina Simone

Here’s what I’ve been listening to this morning at work.

I just wish someone could cast a spell on the RBA.

This is – nina simon – with her version of the classic song – I put a Spell on You – This is the title track from the 1965 album – I put a Spell on You.

This is one of my favorite albums and I play it a lot.

The author of this song is- screaming jay hawkins

Nina Simone’s guitarist is – Rudy Stevenson.

Anyway, if anyone can figure out how to put a spell on the RBA to stop their madness, please let me know!

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}