I see more and more speculation ([1] , [2]) We can avoid recessions by rolling recessions. Often, the argument is that the slowdown is affecting different industries, although one can also look at it geographically. Here I discuss industry and geographic differences.

First of all, from a general point of view, through the lens to achieve real value-added.

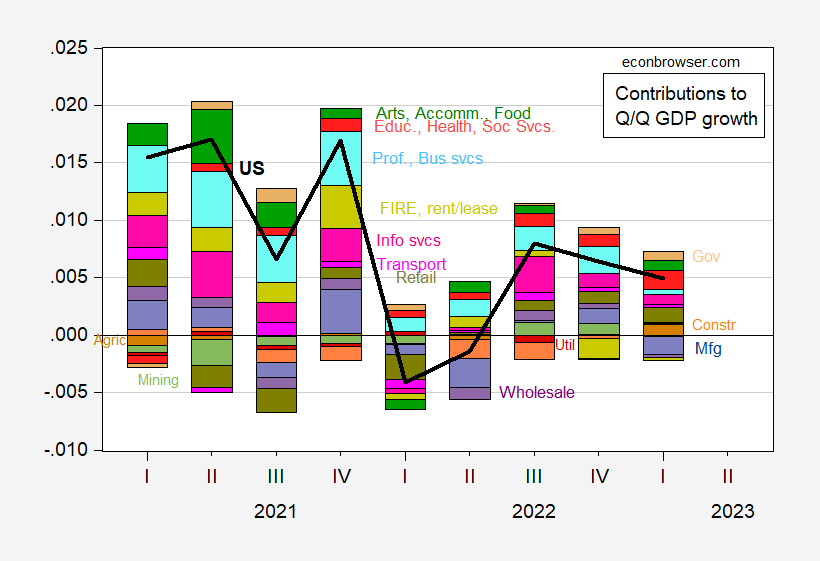

figure 1: Quarterly real GDP growth (thick black line), and contribution of industrial real value added to quarterly GDP growth (bars). Source: BEA and authors’ calculations.

Note that during the slowdown in the first half of 2022, no industry other than professional and business services (including computer systems design and management) has consistently contributed negatively or positively. Compare this to the 2007-09 recession.

figure 2: Quarterly real GDP growth (thick black line), and contribution of industrial real value added to quarterly GDP growth (bars). Recession peak-to-trough dates as defined by NBER are grayed out. Sources: BEA, NBER and authors’ calculations.

Finance, insurance, real estate (FIRE), and leasing and leasing largely led the downturn, with manufacturing not far behind.

Right now we don’t have disaggregated industry data for Q2 2023 (9/28 is the next release), so we don’t know the pattern of contributions right now.

geographical difference

BEA’s expansion across regions showed large growth differences.

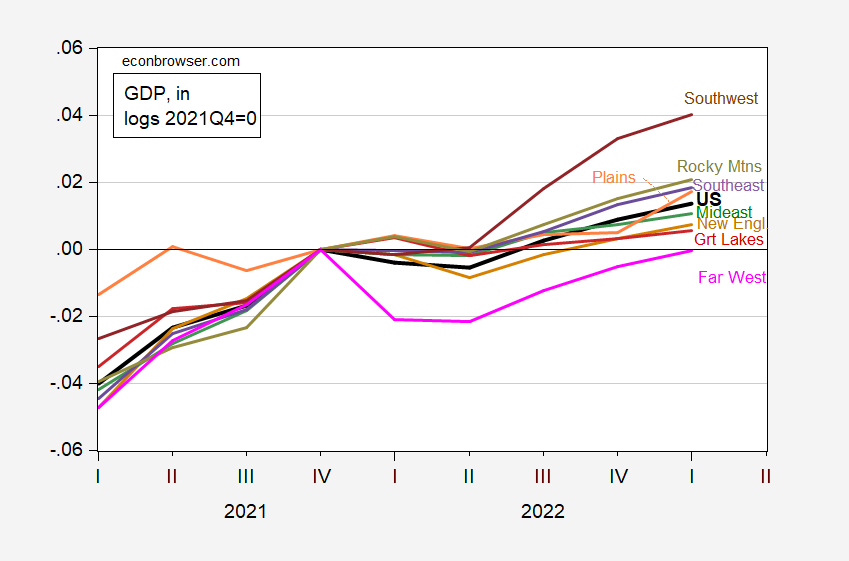

image 3: Log GDP for US (bold black) and BEA, both = 0 in 4Q21. Source: BEA and authors’ calculations.

Figure 3 shows that the slowdown in GDP in the first half of 2022 is concentrated in the Far West, followed by New England. The Southwest is growing much faster than the rest of the country.

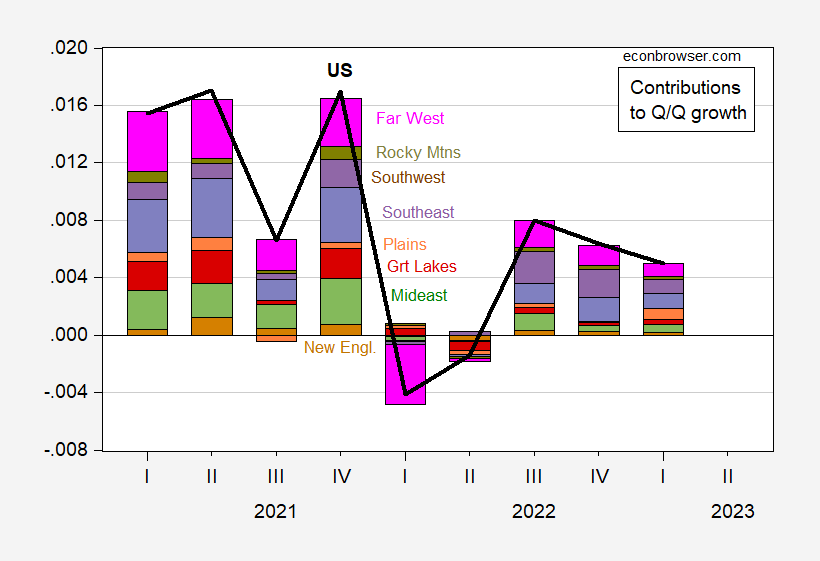

In terms of contribution to GDP growth, the Far West is the main component of the downturn in the first quarter of 2022 in an accounting sense.

Figure 4: Quarter-over-quarter growth rates for the US (thick black line) and BEA region (bars), not annualized. Source: BEA and authors’ calculations.

I tend to interpret the large decline in GDP in the Far West as being related to a large decline in the contribution of professional and business services (including computer systems design and management) and information services. In an accounting sense, the data support this interpretation. In the first quarter, the Far West’s GDP fell by 8.0% (seasonally adjusted rate) from the previous quarter, of which professional and business services and information services combined fell by 3.7 percentage points.

Note that the large effect on the contribution of the Far West to GDP is due to the large size of its economy (as shown in Figure 5), and In this case, variables (as shown in Figure 3).

Figure 5: U.S. GDP (thick black line) and BEA region (bars), in millions of 2012 USD seasonally adjusted. Source: Bank of East Asia.

So, as of Q1, the expansion appears to be broadly geographically based. This does not mean that shocks in one region (or industry) do not propagate strongly to other regions – saying yes or no to this question depends on the causal model.

{kind=link}

{kind=link}