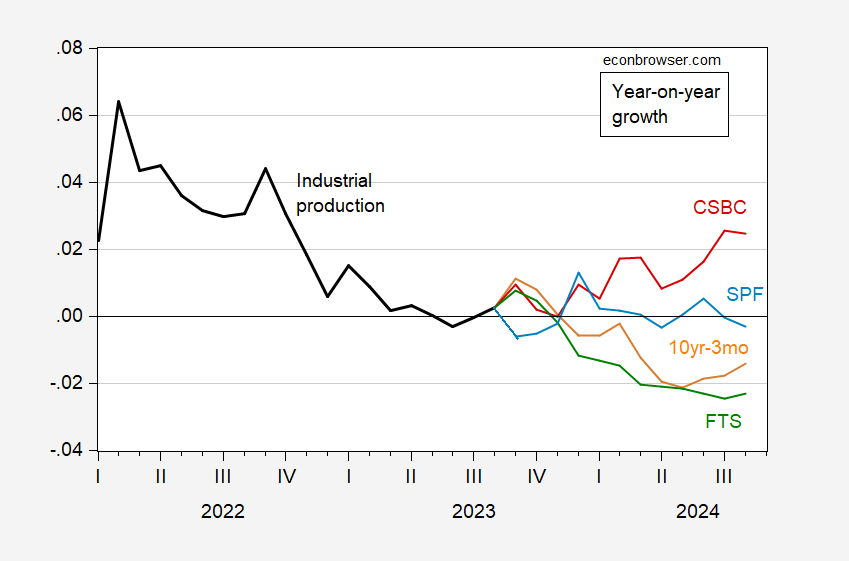

Recession forecasts vary by indicator (term spread, foreign term spread, debt service ratio). Forecasts of economic activity, as measured by industrial production, also vary depending on the forecast factors.

I compared forecasts for 10yr-3mo spreads and foreign term spreads (Ahmed/Chin), and stock market factors determined by Chatelet/Starla-Boudillon/Chin (I thank Arthur Starrer-Bourdillon for updating stock market factors).

figure 1: Annual growth of industrial production (black), 1-year forecast of 10yr-3mo term spreads (orange), foreign 10yr-3mo term spreads (green), Chatelais/Stalla-Bourdillon/Chinn stock market factors (red) and from August forecast (light blue) from a survey of professional forecasters. The foreign term spread is the GDP-weighted long-term interest rate minus the short-term policy rate. SPF industrial production is secondarily interpolated to months. Forecasts are based on a three-year sample to August 2023 (not from a rolling window). Data sources: Federal Reserve, Treasury through FRED, Stalla-Bourdillon calculations, Philadelphia Fed, Federal Reserve Bank of DallasDGEIand the author’s calculations.

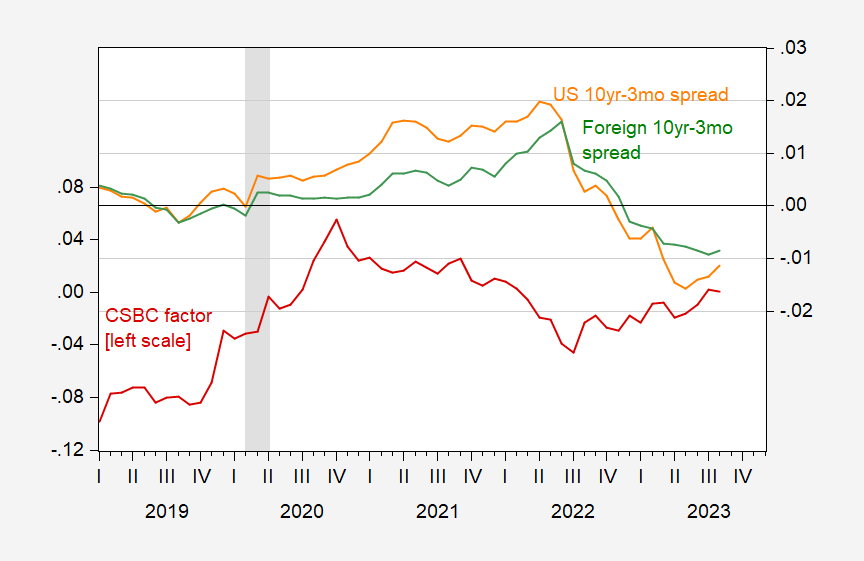

warn: I use the Dallas Fed DGEI spread instead of the Ahmed-Chinn version. The former is GDP weighted for all developed countries, while the latter uses only Canada, the Eurozone, the UK and Japan. The actions of the two are very similar. adjective-R2 The regression value of the Ahmed-Chinn measure used here is 0.8 (in level, the first difference is 0.45).

The outlook for interest rate spreads (domestic and foreign) is pessimistic. These indicators also paint a picture of a coming recession. Stock market factors, which include information on leading industries such as housing, predict a return to economic growth.

figure 2: 10yr-3mo term spread (orange), foreign 10yr-3mo term spread (green), Chatelais/Stalla-Bourdillon/Chinn stock market factors (red). The foreign term spread is the GDP-weighted long-term interest rate minus the short-term policy rate. Source: Ministry of Finance through FRED, Stalla-Bourdillon calculations, Federal Reserve Bank of DallasDGEIand the author’s calculations.

It is important to consider these results versus the results of the recession. Recessions are analyzed using binary variables consistent with the NBER chronology. Industrial production growth is a continuous variable, Just one of several key variables followed by the NBER Business Cycle Dating Committee (Non-agricultural employment population and personal income before transfer payments rank higher) b.

{kind=link}

{kind=link}