look here.

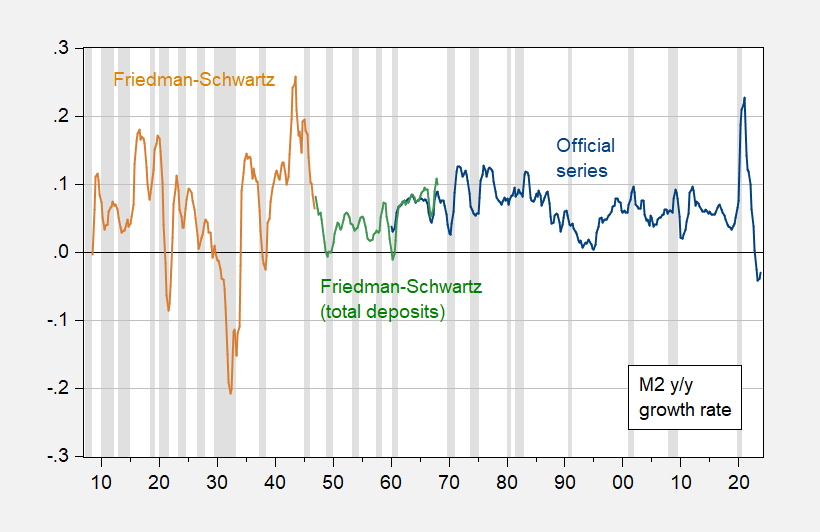

The US money supply (M2) has contracted 4.2% since March 22, and all signs point to a recession later this year. Since the Federal Reserve was established in 1913, there have only been four tightenings in the money supply. Because of the lag, they all lead to recessions.

This is real:

figure 1: Friedman-Schwartz's M2 (tan), total commercial bank deposits (green) and FRB's M2 (blue), year-on-year changes. The first quarter of 2024 is based on the average of the previous two months. NBER-defined recession peak-to-trough dates appear gray. Source: NBER MacroHistory database (m14144a, m14145a), FRB via FRED, NBER, and author's calculations.

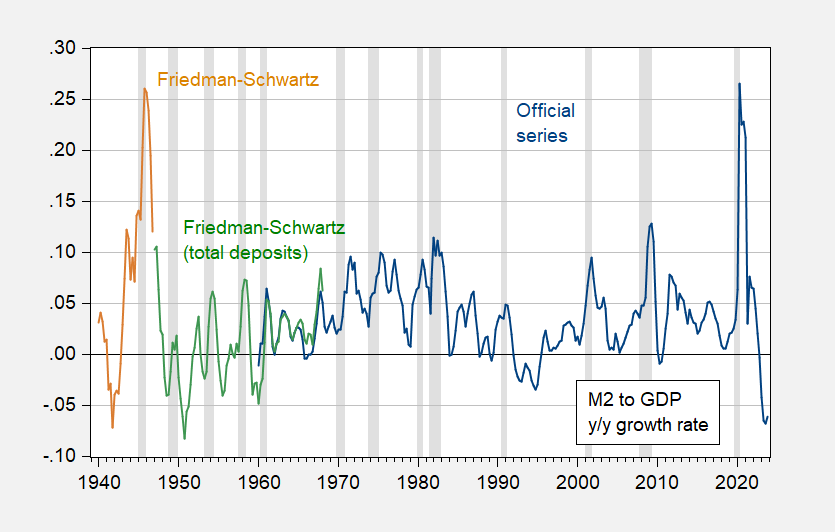

On the other hand, one might think that the relationship of M2 to economic activity (a determinant of supply relative to demand) might be more appropriate.

figure 1: Friedman-Schwartz's M2 (tan), total commercial bank deposits (green) and FRB's M2 (blue), all divided by GDP, year-on-year changes. 2024Q1 M2 is based on the first two months, GDPNow as of 4/5. NBER-defined recession peak-to-trough dates appear gray. Source: NBER MacroHistory database (m14144a, m14145a), FRB via FRED, BEA via FRED, Ramey, Federal Reserve Bank of Atlanta, NBER, and author's calculations.

Not sure of the relevance in this case. There were many negative growth rates before 1960, the mid-1990s, and 2010, but no recessions.

{kind=link}

{kind=link}