From a new paper, NBER WP No. 32084myself and Laurent Ferraracame out today.

Abstract: In recent years, there has been a renewed interest in the moment in the yield curve (or spread as it is called) as a predictor of future economic activity (defined as recession or growth in industrial production). In this article, we revisit the evidence on this predictor for the United States, other high-income countries, and selected emerging market economies (Brazil, India, China, South Africa, and South Korea) from 1995 to 2023. Dot. We examine the sensitivity of the results to the addition of financial variables measuring other dimensions of domestic and international financial conditions. Specifically, we consider financial position indices (Arrigoni et al., 2022), debt service ratios (Borio et al., 2020), and foreign term spreads (Ahmed and Chinn, 2023). We find that in many cases foreign term spreads and debt service ratios yield better predictive power in terms of in-sample fits using the proportion of variance explained. Overall, the predictive power of the yield curve and other financial variables varies across countries, with emerging market economies in particular having very little explanatory power.

For the United States, assuming no recession occurs by February 2023, we obtain the following results: In the parsimonious regression of the term spread only or the short-term spread, the coefficients have the expected signs. There are also significant and expected signs of the financial condition index when this specification is added. However, the addition of debt service ratio (DSR) and foreign term spread eliminates the importance of term spread and FCI.

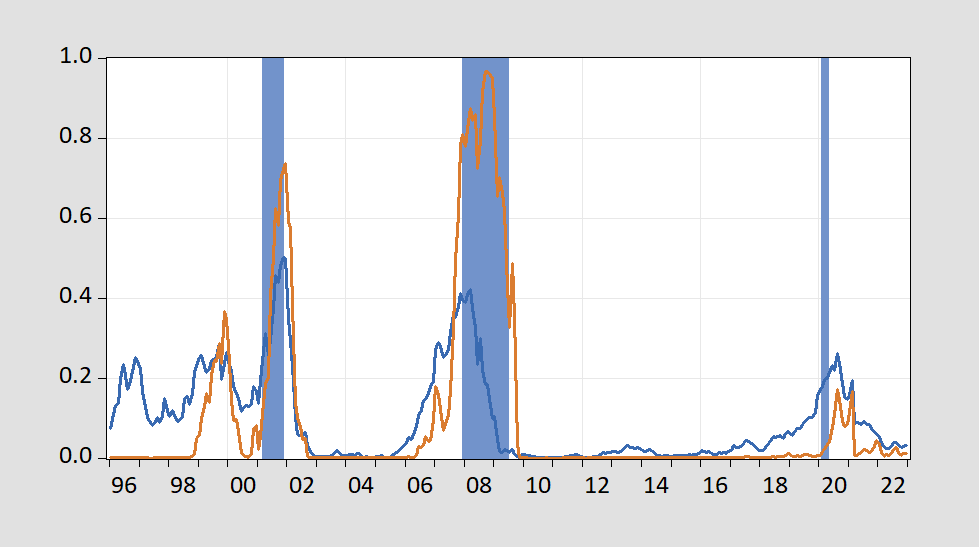

In-sample predictions were made using only the distribution terms and all variables in Figure 1.

figure 1: Recession probability estimated based only on term spreads (blue), term spreads, short rates, FCI, DSR, foreign term spreads (tan), and NBER recession peak-to-trough dates in blue. Source: Figure 2 from Chinn and Ferrara (2024).

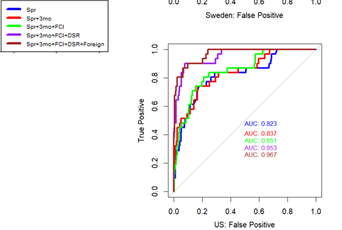

The AUROCs of various models are shown in Figure 2 .

figure 2: AUROC is for US specifications. Source: Figure 3b taken from Chinn and Ferrara (2024).

Note that the AUROC is quite high for the simple term spread specification. However, adding the debt service ratio increases the forecast significantly.Interestingly, the spread of foreign terms (e.g. Ahmed and Chin (2023)) can enhance predictions even after adding DSR.

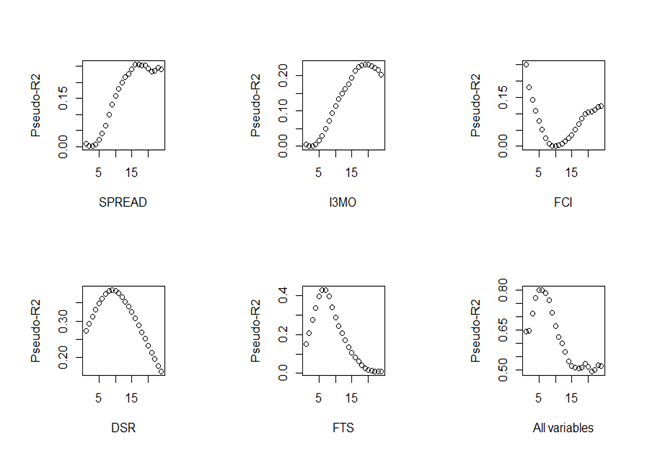

We assessed the predictive power of individual variables at different ranges.

image 3: American pseudo-R2. Source: Figure 4 from Chinn and Ferrara (2024).

Evidence from spreads and short-term rates suggests a peak is predicted to be around a year and a half. In contrast, foreign term spreads peak around six months. The maximum forecast time for DSR is approximately one year. Peak predictions for all five variables occur at approximately 6 months, with a pseudo-R2 of 0.8 (compared to 0.6 at 12 months).

Ungated version Chin and Ferrara (2024).

{kind=link}

{kind=link}