from milwaukee sentinel today (Title not mine):

Try as some may, we cannot blame any single institution or political party—there are too many factors that contribute to inflation. $4 trillion in federal spending during the Trump administration allowed individuals and businesses to continue buying goods and services, supporting prices. At the same time, the Federal Reserve’s commitment to low interest rates and emergency loans has kept the economy afloat amid a potentially catastrophic fall in prices.

The US$1.9 trillion American Rescue Plan passed during the Biden administration has increased upward pressure on prices. The main reason for the acceleration in inflation from 2020 to mid-2021 is fiscal policy. However, from mid-2021, supply chain disruptions and labor market tightness more related to the pandemic will become more important. The rise in oil prices following Russia’s invasion of Ukraine will be particularly important in mid-2022.

This is the picture from the article.

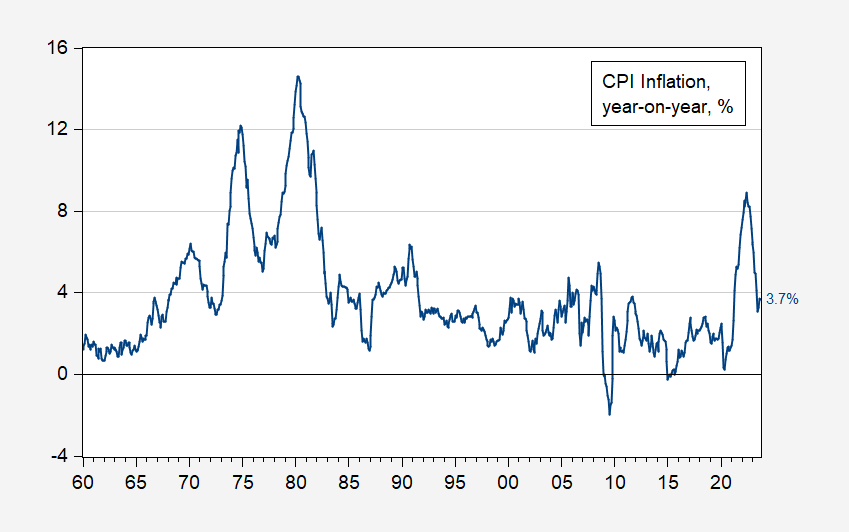

figure 1: Year-on-year CPI inflation rate, % (blue). Source: BLS, author’s calculations.

Looking at inflation series over the long term highlights the fact that, ultimately, inflation is transitory. However, it was not as short-lived and high as many expected.

I think, based on recent analyzes (e.g. here), a combination of supply, cost push and demand (fiscal) shocks has driven inflation in recent years. This is a detail.

figure 2: Year-on-year CPI inflation (blue), instantaneous Eikehout (T=12, a=4) Annual CPI inflation rate (tan) and core CPI (red), %. NBER-defined recession peak-to-trough dates appear gray. Source: BLS, NBER, and author’s calculations.

Note that inflation did rise after the ARP. But numbers have also risen in European countries. Of course, as Russia expands its invasion of Ukraine, inflation rates rise in Europe. Needless to say, this occurred despite less expansionary fiscal policy in the region.

Looking ahead, inflation appears to be down, but not over, as evidenced by the persistence of core inflation (remember, housing costs will have a negative impact next year).

{kind=link}

{kind=link}