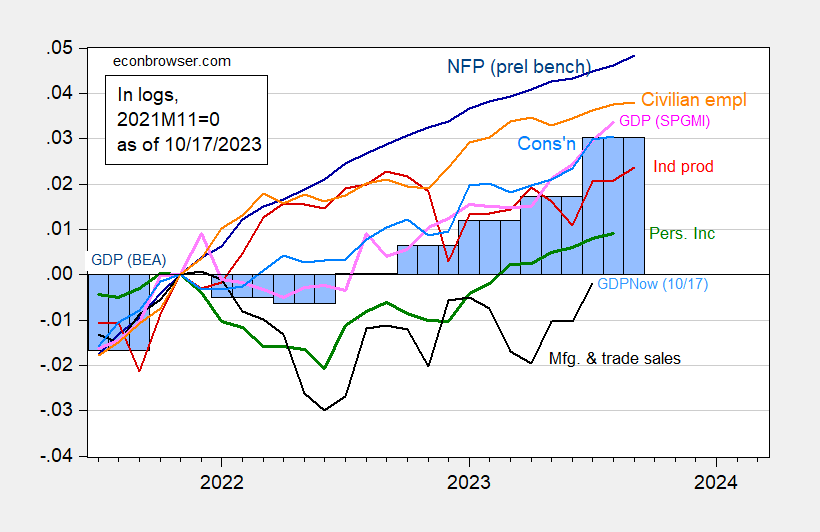

Industrial and manufacturing production unexpectedly rose (month-on-month growth of 0.3%, the market expected a growth of 0.1%, the market expected a growth of 0.4%, the market forecast a growth of 0.1%), of which August growth was revised upward. Below are the key indicators the NBER BCDC follows along with a picture of monthly GDP (SPGMI) and GDPNow (5.4% QoQ YY as of today).

figure 1: Nonfarm employment employment includes preliminary baseline (dark blue), civilian employment (orange), industrial production (red), 2017 personal income excluding transfers (green), 2017 manufacturing and trade sales$ (black), Consumption of monthly GDP (pink) and GDP (blue bars) in Ch.2017$ (light blue), 2017, Ch.2017$ in 2017, all logarithms normalized to 2021M11=0. Source: BLS via FRED, U.S. Bureau of Labor Statistics preliminary benchmarksFederal Reserve, BEA 2023Q2 released for the third time, fully revised, S&P Global/IHS Markit (Nigerian macroeconomic consultant, IHS Markit) (10/2/2023 release), Federal Reserve Bank of Atlanta (released October 17, 2023), and author’s calculations.

It’s hard to imagine a recession coming in September (let alone beyond October). Although there is a general caveat – all series will be revised, as will GDP.

As of today, there are more live broadcasts here.

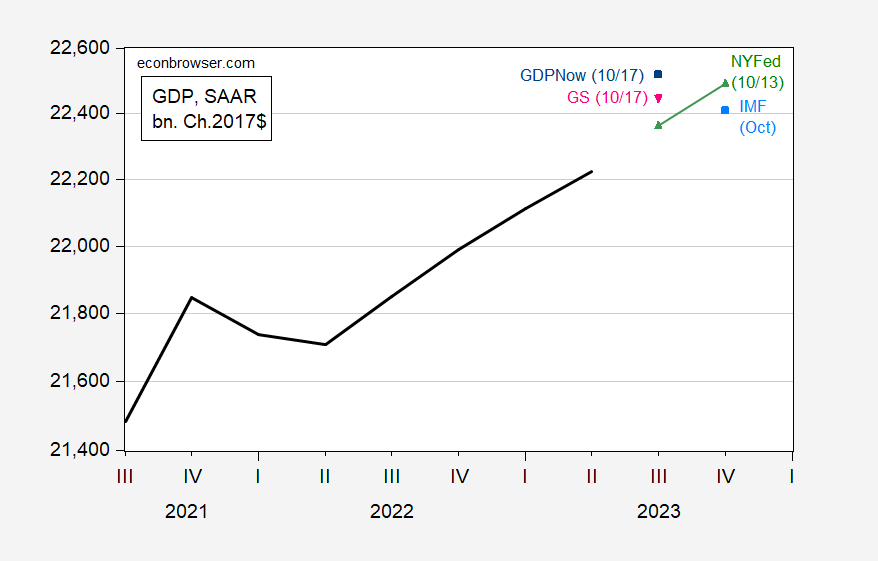

figure 1: Reported GDP (bold black), GDPNow on 10/17 (blue square), NY Fed Live Forecast on 10/13 (green triangle), Goldman Sachs Tracking as of 10/17 (pink inverted triangle), International IMF October World Economic Outlook (sky blue square), all in billions Ch. 2017$, SAAR. Sources: BEA Integrated Revision, Federal Reserve Bank of Atlanta, Federal Reserve Bank of New York, Goldman Sachs, International Monetary Fund World Economic Outlook, and author’s calculations.

Based on these immediate predictions, there’s no slowdown in the third quarter.

{kind=link}

{kind=link}