The IMF conducts regular “visits” to member countries, in which a group of highly paid economists trot to some capital city, hole up in a luxury hotel, hold a few meetings with Treasury officials and the like, and then head off as soon as the meeting is over. Make a short visit to where they came from and submit a report. On October 31, 2023, the International Monetary Fund released— Australia: Staff summary statement on Title IV tasks for 2023 ——This has attracted widespread attention from Australia’s mainstream media. This article summarizes the information the public has received – IMF says Australia needs higher interest rates. This article does not make any qualifications or reflections on the methodology. Journalists with high profile in the country’s mainstream media endorsed the IMF’s conclusions without question. Such is the information need of our time. This is truly an attack on our collective intelligence.

The above news article begins with a sensational headline and then immediately segues into subplot:

The International Monetary Fund has urged central banks to raise official interest rates further, while warning that rates could go even higher if governments don’t abandon or delay some billions of dollars in infrastructure projects.

This is the narrative.

Interest rates rising – why?

Answer: Excessive fiscal deficit – the government must abandon some of its major programs to help transition to a more sustainable economy.

The lack of rigorous scrutiny of these journalists is astounding and, in my opinion, makes them mere lackeys of the IMF rather than investigative independent news organizations.

If you read the IMF report (cited in the introduction), you will find more than journalists are willing to write.

Essentially, media coverage failed to even piece the pieces together.

The International Monetary Fund states that in the case of Australia:

Unemployment remains low, output is above potential, and house prices have recovered after adjusting for 2022…Overall inflation has peaked…but staff assesses that more will be needed to bring inflation back to target and sustain inflation Expectations are stable.

On inflation, they write:

…despite the recent slowdown, services inflation remains high and broad-based, driven by strong demand, labor costs (reflecting historically tight labor markets and weak productivity outcomes) and non-labor costs (e.g. driven by input cost pressures from rent and electricity). ,

I must be living in a parallel universe where labor costs are not rising significantly and real wages are still being slashed.

Furthermore, real wages have lagged “weak” productivity growth, meaning real unit labor costs are falling as more national income is reallocated into profits.

And, in terms of the so-called non-labor costs they refer to, electricity prices are high because privatized companies have been raking in profits and have failed to invest in the necessary infrastructure to integrate growing solar supplies.

The sources of CPI inflation will not be sensitive to rising interest rates.

What is needed is tighter regulation and a reversal of utility privatization.

And, because the Reserve Bank of Australia has been raising interest rates, rent prices are rising rapidly – a classic example of monetary policy supposedly fighting inflation actually causing it.

To be clear, I think it’s insulting that the IMF uses American spelling when discussing Australia, but the IMF believes their approach is one size fits all, which is why they make serious mistakes in many cases.

This is the modern form of imperial colonialism!

Furthermore, as I reported last week in my blog post on Australia’s latest inflation data – Australia’s inflation rate rises slightly due to unreasonable further interest rate hikes (October 25, 2023) – Australia has not seen any major upward changes in inflation expectations.

Two of the main time series were within the RBA target range, with the other time series approaching the upper limit on the way down.

Based on the data we have on inflation expectations, there is no reason to raise interest rates further.

The International Monetary Fund also stated:

Production is expected to be about 1% above potential…

That’s really the core of it.

According to the plan, if the “output gap” is above positive – that is, output is expected to be above potential – then the appropriate response is to tighten fiscal and monetary policy.

Why?

Because this means that overall spending exceeds the economy’s supply capacity to absorb it, and the trigger for the adjustment will be rising prices.

The RBA and IMF have clearly claimed that the current inflation is driven by demand factors, whereas I think it is clear that supply factors have triggered this event and will weaken over time without the need for interest rate adjustments.

But even so, using the output gap to guide policy remains controversial.

International Monetary Fund’s “Finance and Development” series of articles— Output Gap: Departure from Potential – will help you understand what the IMF means when it talks about the output gap and its relationship to policy.

The problem is, these measures are notoriously inaccurate and biased in support of the IMF’s ideological agenda of opposing government intervention.

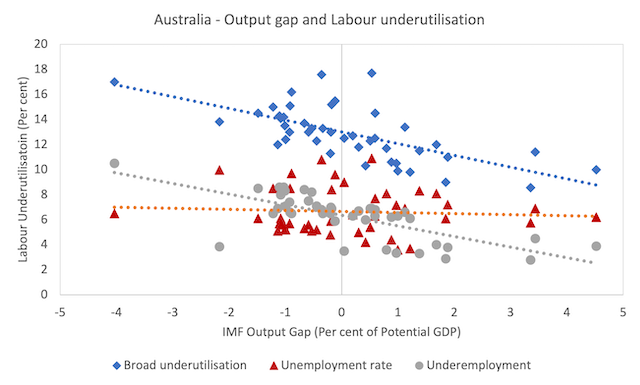

The chart below shows the IMF’s output gap indicator (as a percentage of potential GDP) on the horizontal axis and various labor underutilization indicators (as a percentage of the labor force) on the vertical axis.

The three measures of labor underutilization are:

1. Official unemployment rate.

2. Underemployment (part-time workers who want more hours but can’t find a job).

3. Extensive underutilization (sum of 1 and 2).

The dashed lines associated with each labor underutilization indicator are linear trends.

The diagram is actually quite interesting, as I’m sure you’ll see.

In fact, increases and decreases in the IMF’s output gap indicator are Changeless Changes in the official unemployment rate, which certainly casts doubt on your confidence in the IMF’s measures.

According to the International Monetary Fund, when the unemployment rate is around 6%, Australia could have an output gap (an overall measure of overcapacity) of 4%.

But again, they claim the output gap is likely to be positive 4%, which would mean GDP is 104% of potential GDP – which the IMF classifies as overly full employment at exactly the same rate as the official unemployment rate.

If you believe that, then send me an email and I can sell you the Sydney Harbor Bridge for cheap and throw the Sydney Opera House to you, just for fun.

The problem lies in the way they estimate potential GDP and the underlying NAIRU indicator they use to describe the total capacity of the labor market.

NAIRU is the non-accelerating unemployment rate and is estimated indirectly (because it is unobservable) from an econometric equation, which itself is highly imprecise.

So you get the standard error of the NAIRU point estimate, which is wide, meaning that when the point estimate is 5%, we can be equally confident that the NAIRU is somewhere between 2% and 8%.

In other words, it is so imprecise that even if you believe the underlying theoretical framework, this imprecision makes it useless for policy purposes.

However, organizations such as the International Monetary Fund insist on using it for this purpose because they know that this imprecision systematically biases the conclusion that the current level of fiscal expansion is excessive.

In other words, their measures of potential GDP are always biased downwards because their estimates of the full-employment unemployment rate are always biased upwards.

This bias therefore suits their ideological agenda of smaller government involvement in the economy.

It’s certainly a loaded game.

And in reports that the media loves to publish with sensational headlines, the details are never reported, so all the public gets is ideological bias wrapped in statements like “interest rates must rise further.”

I doubt the reporters who wrote these reports themselves knew the details.

They are merely pawns in the ideological battle between elites and ordinary workers, which over the past few decades has led to low labor utilization, suppressed wage growth, and a massive redistribution of national income toward profits.

The result is rising income and wealth inequality and a decline in the quality and scope of public service delivery.

This shift has benefited some at the expense of many.

Test the proposition

I want to put this to the test by announcing that the federal government will abandon its shitty income support system for unemployment and instead provide a job guarantee with a socially inclusive living wage (which will become the minimum wage) to any worker who wishes to access social benefits This proposal. Working but unable to find a job, any worker who is currently seeking more hours but cannot find a job due to demand constraints.

What do you think will happen?

Socially and environmentally useful output will increase.

The well-being of currently unemployed and underemployed people who accept job offers will improve.

Poverty rates will fall among the unemployed and those affected by the gig economy.

Inflation simply won’t respond.

This shows that the output gap measure for which the IMF makes policy recommendations is simply wrong.

I don’t think it’s possible that about 10% of the available and willing labor force is not working one way or another (unemployed or underemployed) and the economy is judged to be overcapacity.

in conclusion

Unfortunately, the local media does not offer any insight into the garbage the IMF continues to create.

How many times does the IMF have to be smeared (think of the Greek bailout, decades of failed SAP, etc.) before local media can at least be critical of a report the IMF publishes?

That’s enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}

{kind=link}